Key Points

Maruti Suzuki leads in revenue scale, while Hyundai shows stronger SUV-driven positioning.

Both companies faced mild profit pressure in Q4 FY25 due to rising costs.

Hyundai relies more on premium SUVs, and Maruti dominates mass-market segments.

Exports and SUV demand remain key growth drivers for both automakers.

India’s auto industry is seeing strong competition between Hyundai Motor India and Maruti Suzuki. In Q4 FY25 (January-March 2025), both companies released their earnings with mixed results. Maruti Suzuki continued to lead in scale and revenue, while Hyundai showed steady growth driven by SUV demand. Profit trends were uneven due to cost pressures and market shifts. This quarter highlights how both automakers are adapting to changing consumer preferences in a fast-evolving Indian car market.

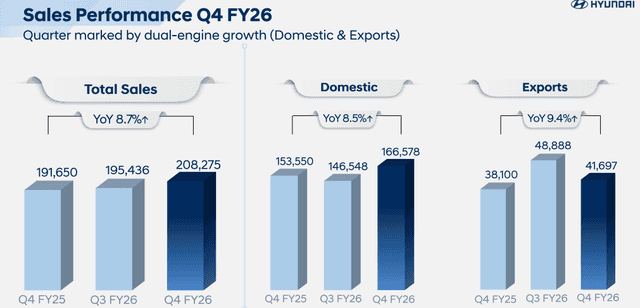

Hyndai & Maruti Q4 FY25 Snapshot: How Did Both Automakers Perform?

India’s auto sector remained strong in Q4 FY25 (Jan-Mar 2025), but growth patterns were uneven. Both Hyundai Motor India and Maruti Suzuki India reported stable revenues with mild profit pressure due to cost inflation and shifting demand trends.

Key numbers (Q4 FY25):

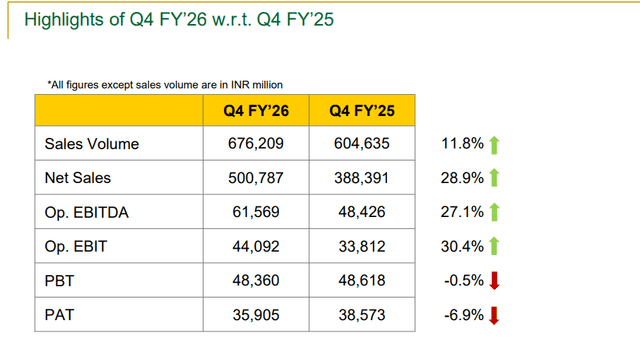

Hyundai Motor India

- Revenue: ~₹17,562 crore (~2.5% YoY)

- Net profit: ~₹1,583-1,614 crore (~4% YoY)

- EBITDA margin: ~14.1%

Maruti Suzuki India

- Revenue: ~₹40,920 crore (~6.4% YoY)

- Net profit: ~₹3,911 crore (~1% YoY)

Maruti clearly leads in scale. Hyundai shows tighter margin control.

Why Did Maruti Suzuki Grow Revenue but See Flat Profits?

Is rising cost pressure hurting Maruti Suzuki?

Yes. Even with strong sales, profit growth remained weak.

- Higher raw material costs reduced margins

- New plant-related expenses increased overhead

- SUV shift improved mix, but not enough to offset costs

Maruti still sold strong volumes in both domestic and export markets. However, operating costs reduced profitability efficiency.

What helped revenue growth?

- Higher SUV contribution

- Strong export demand

- Better pricing in the compact SUV segment

Despite pressure, Maruti continues to dominate India’s mass-market car space.

Why Is Hyundai Motor India Losing Profit Despite SUV Strength?

Can SUVs alone protect Hyundai’s earnings?

Not fully. Hyundai’s SUV-driven portfolio (Creta, Venue, Alcazar) contributed nearly 68% of domestic sales, but profits still dipped.

Key reasons:

- Weak entry-level car demand

- Higher input costs

- Competitive pricing pressure in the compact SUV space

What is supporting Hyundai’s performance?

- Strong export contribution

- Premium SUV demand stability

- EV transition (Creta EV launch strategy)

Hyundai is shifting toward premiumization rather than volume expansion.

Market Strategy Comparison: Volume vs Premium Focus

How are both companies positioning themselves?

Maruti Suzuki India

- Focus: Mass-market dominance

- Strength: Small and compact cars

- Weakness: Lower SUV penetration compared to rivals

Hyundai Motor India

- Focus: SUV + premium segment

- Strength: Feature-rich SUV lineup

- Weakness: Smaller scale in the entry-level segment

Key insight: Maruti wins on scale. Hyundai wins on product mix quality.

Sales Trends: Who Is Winning the SUV Race?

SUV demand remains the biggest growth driver in FY25.

- Hyundai: SUV share ~68% of domestic sales

- Maruti: Rapid SUV expansion but still balancing entry-level dominance

Industry trend shows:

- SUVs are now the fastest-growing segment in India

- Entry-level hatchbacks are declining

- Mid-size SUVs are becoming highly competitive

Export Performance: A Silent Growth Driver

Why are exports becoming more important?

Both companies are relying more on exports to stabilize earnings.

- Hyundai: Strong exports across emerging markets

- Maruti: Record vehicle shipments via global networks

Export growth helps:

- Reduce domestic demand risk

- Improve capacity utilization

- Stabilize revenue cycles

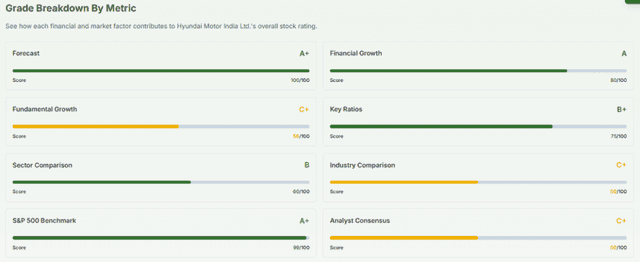

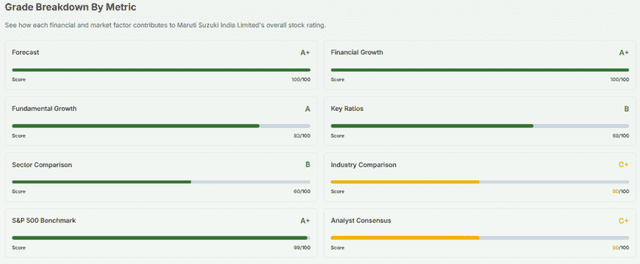

AI Stock Analysis Insight – Market View

Using an AI stock analysis approach similar to modern tools like AI-driven stock intelligence platforms, both companies show different risk profiles:

- Hyundai: Lower scale, higher stability in margins

- Maruti: Higher scale, but more exposed to cost cycles

Meyka market insight:

- Hyundai: “Neutral to positive outlook driven by SUV mix, but margin pressure remains a concern.”

- Maruti: “Stable long-term leadership, but earnings sensitivity to cost inflation persists.”

External analyst consensus aligns with this split view:

- Hyundai = growth in the premium segment

- Maruti = defensive market leadership

What Does the Future Look Like for FY26?

- EV launches will reshape competition

- SUV competition will intensify further

- Input cost volatility may continue

- Export markets will become more important

Both companies are expected to remain market leaders, but their growth paths will diverge.

Closing Note

Q4 FY25 clearly shows two different strategies in India’s auto market. Maruti Suzuki continues to lead in scale and revenue strength, while Hyundai Motor India focuses on SUVs and premium positioning. Both face cost pressure and changing demand trends. The coming quarters will be shaped by EV launches, SUV competition, and export growth, making FY26 a crucial year for both automakers.

Disclaimer:

The content shared by Meyka AI PTY LTD is solely for research and informational purposes. Meyka is not a financial advisory service, and the information provided should not be considered investment or trading advice.

What brings you to Meyka?

Pick what interests you most and we will get you started.

I'm here to read news

Find more articles like this one

I'm here to research stocks

Ask Meyka Analyst about any stock

I'm here to track my Portfolio

Get daily updates and alerts (coming March 2026)