Key Points

On May 8, 2026, Biocon Ltd shares rose nearly 4% in early trade after its Q4 FY26 results for the quarter ended March 2026 surprised the market. The company reported a 57% fall in net profit, mainly due to one-time costs. However, revenue remained steady, keeping investor confidence strong. The stock reaction highlights optimism about its long-term biosimilar growth story. Investors focused on future earnings outlook rather than short-term profit pressure.

On May 8, 2026, Biocon Ltd shares rose nearly 4% in early trade after its Q4 FY26 results for the quarter ended March 2026 surprised the market. The company reported a 57% fall in net profit, mainly due to one-time costs. However, revenue remained steady, keeping investor confidence strong. The stock reaction highlights optimism about its long-term biosimilar growth story. Investors focused on future earnings outlook rather than short-term profit pressure.

Biocon Q4 FY26 Earnings Snapshot

Biocon Ltd delivered a mixed performance in Q4 FY26, but revenue stability helped balance weak earnings. The results were announced for the quarter ending March 2026.

Key Financial Highlights

- Net Profit: ₹198.6 crore (down ~57% YoY)

- Revenue: ₹4,516–₹4,517 crore (stable growth)

- One-time exceptional cost: ~₹80 crore impact

- Core business performance: steady across major segments

The company’s top line remained stable, showing that demand for biosimilars and generics is still intact. However, higher expenses and one-off adjustments pulled net profit lower.

Why Did Biocon’s Net Profit Fall 57% in Q4 FY26?

Was the profit drop due to weak business performance?

No. The decline was not mainly due to sales weakness. The fall came from a mix of cost pressures and accounting adjustments:

- One-time exceptional expenses impacted earnings

- Higher operating and compliance costs

- Strong base effect from last year’s higher profit

- Continued heavy investment in R&D

These factors reduced reported profit, even though core revenue stayed steady. The key takeaway is simple. This was a quality issue, not a demand issue.

Revenue & Segment Performance: What Stayed Strong?

Did Biocon lose business momentum?

No. Revenue performance remained stable, which supported investor confidence.

Segment-wise overview

- Biosimilars: Continued global demand, especially in regulated markets

- Generics: Stable contribution from domestic and export markets

- CRAMS/API: Consistent performance but margin-sensitive

The biosimilars division remains the key long-term growth driver. Analysts still see it as Biocon’s strongest global opportunity.

Why Did Biocon Shares Rise 4% Despite Weak Profit?

What did the market focus on instead of profit?

Investors focused on future growth, not short-term earnings. Even after a 57% drop in net profit, Biocon shares rose nearly 4% because:

- Revenue stayed stable

- Losses were seen as one-time in nature

- Biosimilar pipeline remains strong

- Long-term global expansion outlook is positive

Markets often react to future earnings visibility, especially in pharma stocks, where quarterly profits can fluctuate.

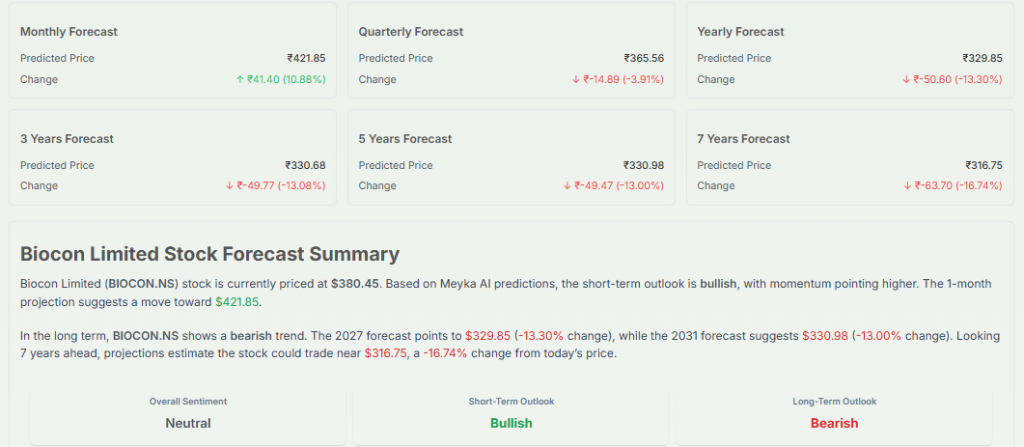

Stock Forecast & Technical Analysis Including AI-Based Insights

What is the short-term outlook for Biocon stock?

Short-term sentiment remains cautiously positive. Stability in revenue and expectations of margin recovery support the stock.

Technical analysis summary

- Stock shows support near the recent consolidation zone after the results

- Resistance likely near previous short-term highs

- Momentum is moderate, not strongly overbought or oversold

- Volume spike after earnings indicates renewed investor interest

What does Meyka AI’s stock analysis tool indicate?

According to a general AI-driven stock analysis view similar to tools like Meyka AI stock analysis platforms, Biocon is currently positioned in a neutral-to-positive zone. The outlook is supported by:

- Stable revenue trend

- Strong biosimilar growth potential

- Short-term volatility due to earnings noise

What do other analysts suggest?

- Some brokerages expect a gradual margin improvement in FY27

- Biosimilars expansion in the US/EU markets is a key trigger

- Cost normalization could improve profitability in the cycle ahead

Overall sentiment is balanced, with a long-term bullish bias but short-term caution.

Analyst Outlook: What Comes Next for Biocon?

Will Biocon improve margins in FY27?

Most analysts believe yes, but gradually. Key expectations include:

- Better EBITDA margins as one-off costs fade

- Strong biosimilars growth in global markets

- Controlled R&D spending growth

- More stable earnings pattern from FY27 onward

The long-term story still depends heavily on global biosimilar approvals and launches.

Wrap Up

Biocon’s Q4 FY26 results show a clear gap between profit and performance. While net profit dropped sharply due to one-time costs, revenue stability and strong biosimilar demand kept investor confidence intact. The 4% stock rise reflects optimism about future growth rather than current earnings. Going ahead, margin recovery and global expansion will decide whether Biocon can convert stability into stronger profitability.

Disclaimer:

The content shared by Meyka AI PTY LTD is solely for research and informational purposes. Meyka is not a financial advisory service, and the information provided should not be considered investment or trading advice.

What brings you to Meyka?

Pick what interests you most and we will get you started.

I'm here to read news

Find more articles like this one

I'm here to research stocks

Ask Meyka Analyst about any stock

I'm here to track my Portfolio

Get daily updates and alerts (coming March 2026)