Key Points

Tesla Q1 2026 earnings focus shifts from EV sales to AI, robotaxis, and autonomy growth.

Vehicle deliveries remain steady but face pricing pressure and rising competition.

Heavy AI and robotics spending is increasing short-term cost and cash flow pressure.

Analysts revise forecasts as markets weigh execution risks against long-term AI potential.

Tesla is set to report its Q1 2026 earnings in late April 2026, and investor attention is unusually intense this quarter. The company is no longer viewed only as an electric vehicle maker. It is now being closely tracked as an AI and autonomous technology leader. Expectations are high, but so are concerns. Recent data shows uneven vehicle demand, rising competition, and heavy spending on artificial intelligence and automation projects.

At the same time, Tesla’s long-term vision around robotaxis and self-driving software continues to drive market excitement. Analysts have also started revising forecasts as they weigh short-term pressure against long-term growth potential. With capital spending increasing and profitability under review, this earnings report could shape Tesla’s stock direction for months. Investors are now asking a key question: Can Tesla’s AI future justify its current performance gap?

Tesla Q1 2026 Earnings Overview

Tesla’s Q1 2026 earnings arrive with mixed expectations from Wall Street. As of April 2026, consensus estimates point to moderate revenue growth driven by steady EV demand and expanding energy storage sales. Analysts expect earnings per share to remain under pressure due to higher operating costs and heavy investment in artificial intelligence and autonomy programs.

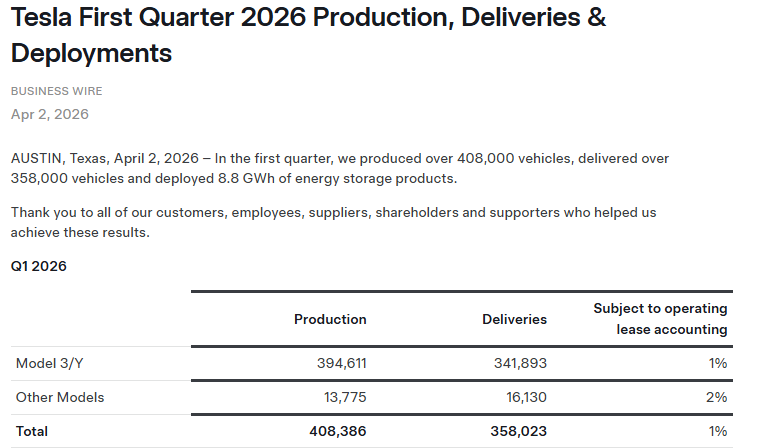

Vehicle deliveries for the quarter are estimated at around the mid-350,000 range. This reflects stable output but weaker-than-expected demand in some regions due to pricing competition. Inventory levels are also slightly higher compared to the previous quarter.

Revenue is projected in the range of roughly $21B-$23B based on aggregated analyst forecasts. Investors are now focusing less on short-term vehicle numbers and more on Tesla’s AI and robotics roadmap.

Robotaxis and Autonomous Driving Progress

How important is the robotaxi strategy for Tesla right now?

Robotaxis are now a core part of Tesla’s long-term valuation story. The company continues to test and expand its Full Self-Driving (FSD) system in select U.S. cities. However, full-scale commercial rollout is still limited.

Recent updates suggest a gradual expansion in test zones such as Texas and California. Tesla is focusing on improving safety performance, regulatory approvals, and real-world driving data collection.

Key focus areas include:

- FSD adoption rates among existing Tesla owners

- Safety validation across diverse road conditions

- Regulatory discussions in multiple U.S. states

- Fleet readiness for future ride-hailing integration

Despite progress, no large-scale robotaxi revenue model has been officially launched yet.

AI Spending Surge and Capital Investment Pressure

Tesla’s AI strategy is driving a sharp rise in capital expenditure in 2026. The company is investing heavily in custom AI chips, data infrastructure, and robotics systems like Optimus.

Why is Tesla increasing AI spending so aggressively?

The goal is to build a fully integrated autonomy ecosystem. This includes self-driving cars, AI-powered manufacturing, and humanoid robotics.

Key spending areas:

- AI training clusters and compute infrastructure

- Custom silicon for autonomous driving

- Optimus humanoid robot development

- Expansion of energy storage systems

This has created short-term pressure on free cash flow. Analysts expect continued heavy investment through 2026 as Tesla scales its AI capabilities.

An AI stock analysis tool used by institutional investors highlights Tesla as a “high-volatility, high-growth AI transition stock,” mainly driven by future earnings potential rather than current margins.

Tesla Earnings: Vehicle Deliveries, Pricing, and Margin Trends

Tesla continues to face competitive pressure in global EV markets. Chinese manufacturers and legacy automakers are intensifying pricing competition, which has impacted Tesla’s pricing strategy.

What is happening to Tesla’s margins?

Gross margins are expected to remain in the mid-to-high teens. This is slightly lower than peak levels seen in earlier growth cycles.

Key trends:

- Price cuts in key models to maintain demand

- Rising production efficiency offsetting some cost pressure

- Higher logistics and AI-related operating expenses

- Stronger contribution from the energy storage segment

Inventory buildup remains a concern, especially in North America and Europe, where demand growth has slowed compared to earlier years.

Energy Business and Diversification Growth

Tesla’s energy division continues to show strong momentum. The Megapack and Powerwall products are driving steady revenue growth.

Why is the energy segment becoming more important?

Energy storage provides a stable cash flow compared to the cyclical automotive business. It also supports global grid modernization trends.

Key highlights:

- Increasing Megapack deployments for utility-scale projects

- Rising demand for renewable energy storage

- Expansion in international energy contracts

- Estimated double-digit revenue growth in the segment

This division is now seen as a key stabilizer for Tesla’s overall financial performance.

Analyst Forecast Revisions and Market Sentiment for Tesla

Wall Street analysts have recently adjusted Tesla’s price targets and earnings expectations ahead of Q1 2026 results.

Why are analysts changing their forecasts?

Forecast revisions are mainly driven by:

- Slower near-term EV demand

- Higher-than-expected AI spending

- Uncertainty around robotaxi monetization timelines

- Strong long-term growth potential in autonomy

Some analysts remain bullish on Tesla’s long-term AI positioning. Others warn that valuation already reflects aggressive future assumptions.

What is the market expecting now?

- Moderate EPS growth in the short term

- High volatility after the earnings announcement

- Strong focus on management commentary rather than numbers

Key Catalysts to Watch in Earnings Calls

Investors will closely watch Tesla’s management commentary during the Q1 2026 earnings call. Important questions include:

- When will robotaxis become commercially scalable?

- How fast is FSD adoption growing?

- What is the updated AI roadmap timeline?

- How will Tesla balance capex and profitability?

- What are the expectations for Q2 2026 deliveries?

Market reaction will likely depend more on forward guidance than actual earnings results.

Meyka Stock Insight and Market View

Meyka’s AI model currently classifies Tesla (TSLA) as a high-growth, high-volatility AI transition stock. The score reflects strong long-term potential but mixed short-term fundamentals. Technical signals show a neutral trend, with no clear bullish or bearish control in the near term.

Overall, the outlook is driven more by future AI and robotaxi growth expectations than current earnings strength. Short-term pressure comes from high valuations, rising AI spending, and margin concerns, while long-term sentiment stays focused on autonomy and robotics upside.

Bottom Line

Tesla’s Q1 2026 earnings go beyond financial results. They highlight Tesla’s shift from an EV maker to an AI and mobility company. Short-term pressure from costs and competition remains. But long-term focus stays on robotaxis, autonomy, and robotics. The earnings call will be key for investor sentiment. Markets now want clear proof that Tesla’s AI plans can scale and generate real profits.

Disclaimer:

The content shared by Meyka AI PTY LTD is solely for research and informational purposes. Meyka is not a financial advisory service, and the information provided should not be considered investment or trading advice.

What brings you to Meyka?

Pick what interests you most and we will get you started.

I'm here to read news

Find more articles like this one

I'm here to research stocks

Ask Meyka Analyst about any stock

I'm here to track my Portfolio

Get daily updates and alerts (coming March 2026)