Key Points

SBI FY26 profit hits record ₹80,032 crore, up ~13% YoY despite Q4 weakness.

Q4 FY26 profit rises but misses expectations due to lower NII and treasury income.

Net Interest Margin slips near ~2.9%, raising concerns about future earnings stability.

Stock falls 0.13% as investors focus on margins and the operating profit slowdown over annual growth.

State Bank of India surprised investors after reporting a record annual profit of ₹80,032 crore for FY26, yet its stock slipped 0.13% following the Q4 results announcement. The earnings, released in May 2026, showed pressure on profit margins and weaker treasury income despite strong loan growth. This unusual market reaction has raised fresh questions about SBI’s future growth outlook, profitability, and the broader direction of India’s banking sector in a changing interest-rate environment.

SBI Reports Record FY26 Profit, But Q4 Weakness Pressures Stock

FY26 Profit Hits All-Time High

State Bank of India delivered its highest-ever annual profit in FY26. The country’s largest public sector bank reported a standalone net profit of ₹80,032 crore for the financial year ended March 31, 2026. The figure was nearly 13% higher than the FY25 profit of ₹70,901 crore.

SBI also maintained strong loan growth across retail, agriculture, and MSME segments. Its RAM portfolio crossed ₹27 trillion during the year. Strong credit demand and lower bad loans supported overall earnings growth.

The bank also announced a dividend of ₹17.35 per share for FY26. The record date was fixed as May 16, 2026.

Why Did Q4 Earnings Disappoint Investors?

Despite strong annual numbers, investors focused on weaker quarterly performance. SBI reported Q4 FY26 net profit of ₹19,684 crore, up only 5.6% year-on-year. However, profit declined sequentially from ₹21,028 crore reported in Q3 FY26. Total income also fell to ₹1.40 lakh crore during the March quarter.

The market reacted negatively because operating profit and treasury income weakened sharply. SBI shares slipped after the earnings release as investors worried about slower earnings momentum going into FY27.

The Real Reason SBI Shares Fell After Earnings

NIM Compression Became the Biggest Concern

Net Interest Margin, or NIM, became the biggest pressure point in SBI’s Q4 results. Domestic NIM declined to 2.93% in Q4 FY26 from 3.14% a year earlier. Every quarter, margins also dropped from 3.11%.

The decline reflected rising deposit costs and lower lending spreads. RBI policy changes and competitive deposit pricing also affected profitability. Investors usually track NIM closely because it measures how efficiently banks generate earnings from loans.

According to Reuters, SBI management maintained FY27 guidance of around 3% NIM despite global economic uncertainty and oil market risks linked to Middle East tensions.

Treasury Income and Operating Profit Weakened

Another major issue was weak treasury performance. Rising bond yields reduced treasury gains during the quarter. Reuters reported that forex arbitrage curbs and bond market volatility also hurt treasury income.

Operating profit fell more than 11% year-on-year to ₹27,704 crore in Q4 FY26. Sequentially, it declined nearly 16%. This slowdown overshadowed the bank’s record annual earnings.

Meyka’s AI stock analysis tool highlights that SBI remains fundamentally strong due to stable credit growth and improving asset quality, but short-term technical pressure may continue if margins stay below investor expectations.

Strong Areas Investors Should Not Ignore

Asset Quality Continued Improving

SBI still showed strong improvement in asset quality. Gross NPA ratio declined to 1.49% in Q4 FY26, compared to higher levels in previous years. Lower stressed assets helped reduce provisioning pressure and strengthened investor confidence over the long term.

The bank also maintained strong capital levels and healthy balance-sheet growth. Many analysts believe SBI remains one of the strongest PSU banking plays despite short-term margin pressure.

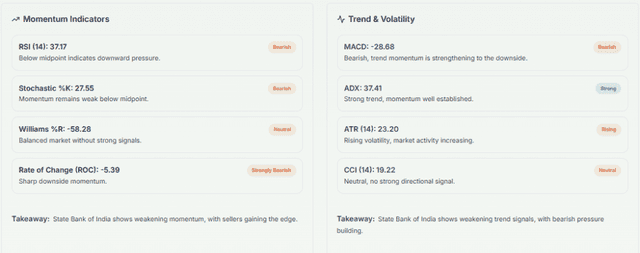

What Analysts and Technical Charts Suggest?

Technical analysts say SBI stock is currently facing resistance near the ₹1,050-1,070 range after the post-results decline. Support is seen around the ₹1,000 levels. Market experts believe the stock may remain volatile until investors gain clarity on FY27 margin trends.

Several brokerage firms still remain positive because:

- Loan growth guidance stays at 13-15%

- Asset quality continues improving

- PSU banks are reporting record sector profits in FY26

Conclusion

State Bank of India delivered a historic FY26 performance with record annual profit and improving asset quality. However, shrinking margins, weaker treasury income, and softer Q4 operating profit triggered investor concerns.

Markets are now watching whether SBI can protect profitability and maintain loan growth in FY27. If margins stabilize and credit demand stays strong, the bank could regain investor confidence despite recent stock weakness.

Disclaimer:

The content shared by Meyka AI PTY LTD is solely for research and informational purposes. Meyka is not a financial advisory service, and the information provided should not be considered investment or trading advice.

What brings you to Meyka?

Pick what interests you most and we will get you started.

I'm here to read news

Find more articles like this one

I'm here to research stocks

Ask Meyka Analyst about any stock

I'm here to track my Portfolio

Get daily updates and alerts (coming March 2026)