NSE: DMART Falls 4% Despite ₹860 Crore Q1 FY27 Profit Beat; Here’s Why Investors are Selling

Key Points

DMart reported Q1 FY27 net profit of ₹860.6 crore, up 11.3% year over year.

Despite the earnings beat, DMart shares fell nearly 4% on the NSE.

High valuations, margin pressure, and quick-commerce competition weighed on sentiment.

Analysts remain positive on long-term growth but expect near-term stock volatility.

On July 13, 2026, Avenue Supermarts, the company behind DMart, reported a stronger-than-expected Q1 FY27 performance with a net profit of ₹860.6 crore. Despite the earnings beat, the stock dropped nearly 4% on the NSE during the trading session. The reaction suggests investors were looking beyond the headline numbers. So, why did the market respond negatively? Here’s a closer look at the factors behind the sell-off.

DMart Q1 FY27 Results Overview

Key Financial Highlights

Avenue Supermarts posted healthy growth for the quarter ended June 30, 2026. Consolidated net profit rose 11.3% year over year to ₹860.6 crore, while revenue from operations increased 14.9% to ₹18,795 crore. The retailer also expanded its footprint by opening three new stores, taking its total store count to 503.

The company continued to grow despite higher operating costs and increased competition across India’s retail market.

Quick Numbers

| Metric | Q1 FY27 |

| Revenue | ₹18,795 crore |

| Net Profit | ₹860.6 crore |

| Profit Growth | 11.3% YoY |

| Revenue Growth | 14.9% YoY |

| Total Stores | 503 |

Even with results that came in slightly ahead of expectations, investors were hoping for stronger margin expansion and better growth from existing stores.

Why Did DMart Shares Fall Despite Better Earnings?

Why Was a Profit Beat Not Enough?

Investors paid more attention to what lies ahead than to the quarterly profit. DMart shares fell nearly 4% on July 13, 2026, as concerns grew over slowing momentum in some of the company’s larger markets.

High Valuation Left Little Room for Disappointment

DMart has traded at a premium valuation for years compared with most listed retail companies in India. That means expectations remain high every quarter. Even solid earnings can trigger selling if the market believes growth is slowing or margins are unlikely to improve.

Margin Pressure Has Not Eased

Operating costs stayed elevated during the quarter. Spending on employees, store expansion, and competitive pricing continued to weigh on profitability. Revenue increased at a faster pace than net profit, indicating that margins remain under pressure.

Quick Commerce Is Reshaping Consumer Spending

Performance varied across regions. Mature metro markets saw limited growth, while non-metro locations performed better. Analysts say quick-commerce platforms are taking a larger share of spending in major cities, making it harder for established DMart stores to maintain previous growth rates. Like-for-like sales growth also slowed to around 5.5%, adding to investor caution.

What are Analysts and Brokerages Saying?

Are Experts Still Positive on DMart?

Brokerage opinions remain mixed after the quarterly results.

Motilal Oswal retained its Buy rating and raised its target price slightly to ₹4,800. The brokerage believes DMart’s value-driven business model and expansion into Tier 2 and Tier 3 cities should continue to support long-term growth.

Citi took a more cautious view. It maintained its Sell rating and lowered its target price, pointing to weaker same-store sales growth, pressure on margins, and rising competition from quick-commerce companies.

According to Meyka’s AI stock analysis tool, DMART continues to have strong long-term fundamentals backed by its efficient retail operations and steady store expansion. Even so, the stock could remain volatile until margins improve and demand strengthens in metro markets. That view is broadly in line with several analysts who remain positive over the long term while staying cautious about the near-term outlook.

Should Investors Worry About DMart Stock?

DMart continues to expand its store network while increasing both revenue and profits. Its long-term business model remains intact. Even so, investors should keep an eye on margin trends, same-store sales growth, and competition from quick-commerce platforms. With the stock trading at a premium valuation, future earnings will need to stay strong to support higher prices.

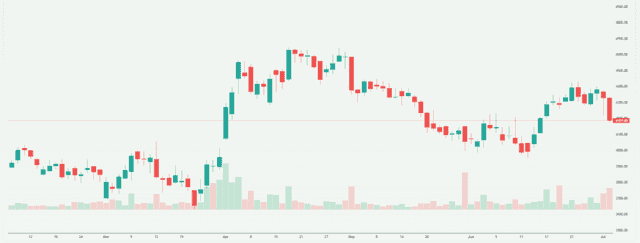

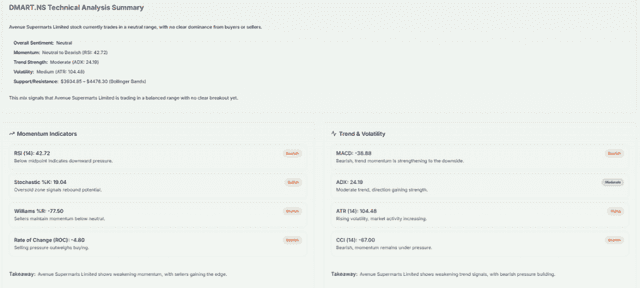

Technical Analysis Summary: DMart has weakened in the short term after slipping below the ₹4,000 support level. The next resistance is around ₹4,100. A sustained recovery may depend on stronger execution and improved operating performance over the coming quarters.

Conclusion

DMart delivered another quarter of revenue and profit growth, but that was not enough to satisfy the market. Investors focused on slower growth at mature stores, pressure on margins, and the stock’s premium valuation. Those concerns outweighed the earnings beat and pushed the shares lower. While short-term volatility may continue, the company remains one of India’s strongest retail businesses with a disciplined expansion strategy and a solid financial position.

Disclaimer:

The content shared by Meyka AI PTY LTD is solely for research and informational purposes. Meyka is not a financial advisory service, and the information provided should not be considered investment or trading advice.

What brings you to Meyka?

Pick what interests you most and we will get you started.

I'm here to read news

Find more articles like this one

I'm here to research stocks

Ask Meyka Analyst about any stock

I'm here to track my Portfolio

Get daily updates and alerts (coming March 2026)