NeoVolta Stock Jumps 20% After Needham Initiates Buy Rating With $8 Target, Signaling 300% Upside

Key Points

NeoVolta stock surged ~20% after Needham issued a Buy rating with an $8 price target.

Strong revenue growth driven by rising demand in energy storage and U.S. manufacturing expansion The company remains unprofitable, with dilution and execution risks impacting investor sentiment.

Analysts show mixed views, with high volatility and a wide price target range for NEOV in 2026.

NeoVolta stock jumped about 20% in mid-June 2026 after Needham & Company initiated coverage with a Buy rating and an $8 price target. The move caught investors’ attention as energy storage demand continues to grow in the U.S. It also reflects renewed optimism around small-cap clean energy manufacturers. Shares remain volatile, but the bullish analyst call has shifted short-term sentiment. Investors are now watching whether the rally can hold through late June 2026.

NeoVolta Stock Surge Explained After Needham Rating

NeoVolta Inc. (NASDAQ: NEOV) gained strong attention after jumping nearly 20% in June 2026. The rally followed Needham & Company initiating coverage with a Buy rating and an $8 price target, suggesting significant upside from the ~$1.80–$2.60 trading range seen in mid-June 2026.

The move reflects renewed investor interest in small-cap energy storage companies. Trading volume also increased sharply after recent financing and project updates.

Key drivers behind the surge include:

- Improved sentiment in clean energy stocks

- Growing U.S. battery storage demand

- Speculation around NeoVolta’s Georgia manufacturing ramp

Despite the rally, volatility remains high, with the stock still down significantly year-to-date due to dilution pressure and weak profitability trends.

Why Is Needham Bullish on NeoVolta?

Energy Storage Demand Acceleration

Needham’s bullish stance is based on long-term energy storage growth. The U.S. grid modernization push and AI-driven power demand are increasing battery deployment needs. NeoVolta is targeting residential and utility-scale storage solutions.

Georgia Facility as a Growth Catalyst

NeoVolta’s Georgia manufacturing facility remains a key catalyst. According to recent operational updates, initial production is targeted for mid-2026 with 2 GWh capacity in phase one . This could significantly expand revenue scale if fully executed.

Revenue Growth Trend

Recent financials show strong top-line expansion:

- Revenue reached $4.65M in Q2 FY2026

- YoY growth exceeded 300% in earlier quarters

- Pipeline expansion through new supply agreements supports future growth

Needham views this as early-stage hyper-growth rather than stable maturity.

Financial Performance and Risks Investors Must Know

NeoVolta’s growth comes with clear financial pressure. The company remains unprofitable, reporting negative EPS and widening operating losses due to higher R&D and facility buildout costs.

Recent filings show:

- Net loss of roughly -$5M (TTM)

- Operating margin around -56%

Another major concern is dilution. The company recently raised capital through equity offerings, including a $25M stock sale to fund expansion and JV obligations.

Key Risks

- Heavy reliance on equity financing

- Execution risk in the Georgia facility ramp

- Revenue inconsistency across quarters

- High volatility in small-cap energy stocks

While growth is strong, profitability remains uncertain in the near term.

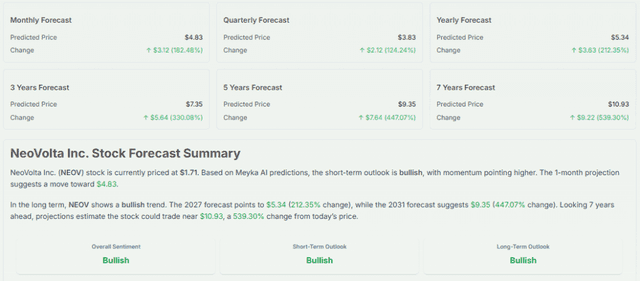

Analyst Forecast, Meyka View, and Technical Analysis

Wall Street sentiment remains mixed. Based on aggregated analyst data, NeoVolta carries a “Reduce” consensus rating with limited coverage and an average target in the $6 range in broader models.

Technical Analysis Summary

- Stock trades in a downtrend from 52-week highs near $7+

- Support zone forming around $1.70-2.00

- Resistance seen near $2.80-3.20

- High volatility with frequent gap moves driven by news

What Meyka AI Stock Tool Indicates?

Using insights from the Meyka AI stock analysis tool, NEOV is classified as a high-volatility speculative growth stock, with sentiment leaning “cautiously bullish” due to revenue acceleration but weak earnings stability.

Other Analyst Insights

- Needham: Buy, $8 target

- MarketBeat consensus: Hold/Reduce

- Independent models: wide range $4-10 depending on execution success

Industry Tailwinds Supporting NeoVolta

NeoVolta operates in the fast-growing energy storage sector. Demand is rising due to renewable integration, AI data center expansion, and grid instability concerns. Global battery storage capacity is expected to expand sharply through 2030. U.S. policy incentives are also supporting domestic manufacturing.

However, competition is intense. Larger players like Tesla Energy and Fluence dominate scale production. NeoVolta’s strategy focuses on niche positioning, faster deployment, and regional manufacturing advantages in the U.S. clean energy supply chain.

Conclusion

NeoVolta’s 20% surge reflects renewed optimism after Needham’s bullish $8 price target. The company shows strong revenue growth and expanding production capacity, but financial risks remain significant.

High dilution, ongoing losses, and execution challenges continue to weigh on long-term confidence. Investors are now focused on whether the Georgia facility ramp and energy storage demand can justify the aggressive valuation upside implied by analysts.

Disclaimer:

The content shared by Meyka AI PTY LTD is solely for research and informational purposes. Meyka is not a financial advisory service, and the information provided should not be considered investment or trading advice.

What brings you to Meyka?

Pick what interests you most and we will get you started.

I'm here to read news

Find more articles like this one

I'm here to research stocks

Ask Meyka Analyst about any stock

I'm here to track my Portfolio

Get daily updates and alerts (coming March 2026)