Key Points

Hindalco Q4 net profit fell 51% YoY to ₹2,597 crore despite record revenue.

Novelis fire-related losses and weak US shipments hurt overall earnings.

India aluminium and copper businesses delivered strong operational performance.

Hindalco announced a ₹5 dividend while shares slipped nearly 2% after results.

Hindalco Industries surprised investors after reporting a sharp 51% drop in Q4 FY26 net profit on May 22, 2026. The company posted earnings of ₹2,597 crore, sending its shares down nearly 2% in early trade.

The decline came despite record revenue and strong operational performance in its aluminium and copper businesses. Rising global uncertainty and disruption at Novelis raised fresh concerns about future margins. Investors are now watching closely to see whether Hindalco can regain momentum in the coming quarters.

Hindalco Q4 FY26 Results at a Glance

Key Numbers Investors Need to Know

Hindalco Industries reported a mixed set of Q4 FY26 earnings on May 22, 2026. The company posted a sharp fall in profit even though revenue and EBITDA reached record highs.

Here are the major numbers from the March quarter:

- Consolidated net profit: ₹2,597 crore, down 51% YoY

- Revenue from operations: ₹78,133 crore, up 20%

- EBITDA: ₹11,197 crore, up 9%

- Earnings per share (EPS): ₹11.69 compared to ₹23.80 last year

- Recommended dividend: ₹5 per equity share

The company also reported full-year FY26 revenue of ₹2.74 lakh crore. That marked a 15% rise from FY25.

Why the Results Shocked Dalal Street?

Investors expected strong growth after Hindalco’s India business delivered record aluminium and copper earnings. Instead, the profit decline surprised the market.

The biggest concern came from exceptional losses linked to Novelis operations in the United States. Weak shipment volumes and disruption caused by the Oswego plant fire reduced overall profitability.

Following the results, Hindalco shares fell nearly 2% during early trading on the BSE.

Why Did Hindalco Profit Crash 51% Despite Revenue Growth?

Novelis Fire Disruption Became the Biggest Earnings Drag

The biggest reason behind the sharp earnings decline was the fire-related disruption at Novelis’ Oswego facility in New York.

Novelis, Hindalco’s US-based aluminium rolling subsidiary, faced two major fire incidents during FY26. These incidents severely affected production and shipment volumes. The company revised the expected cash flow impact from $650 million to nearly $1.7 billion.

Novelis reported a quarterly net loss of $84 million due to these disruptions. Hindalco said the Oswego hot mill is expected to restart within the next few weeks.

Rising Costs and Tariff Headwinds Hurt Margins

Global aluminium markets remained volatile throughout FY26. US tariff concerns and slowing industrial demand affected margins across metal companies.

Novelis also faced lower shipment volumes during the quarter. Higher operational expenses added pressure on consolidated profitability.

At the same time, global scrap prices and logistics costs remained unstable. This reduced the benefit of stronger aluminium prices.

One-Time Charges Distorted Overall Profitability

A key point investors should note is that Hindalco’s core business remained strong. Profit before exceptional items actually rose 10% YoY to ₹5,796 crore. However, after accounting for one-time losses tied to the Oswego disruption, reported PAT dropped sharply. This explains why EBITDA hit a record high while net profit collapsed.

Segment-Wise Performance: What Worked and What Failed?

Copper Business Emerged as the Bright Spot

Hindalco’s copper division delivered one of its strongest quarters ever. Copper EBITDA jumped 48% YoY to ₹907 crore. Better sulphuric acid realization and strong domestic demand supported growth.

The company is also expanding its copper production capacity to meet rising industrial and EV demand in India.

Aluminium Upstream Delivered Record EBITDA

The India aluminium upstream business remained highly profitable. Key highlights included:

- Revenue rose 11% YoY to ₹11,418 crore

- EBITDA climbed 13% to ₹5,448 crore

- EBITDA per tonne reached a record $1,756

- Operating margin stayed strong at 48%

Strong aluminium prices and lower production costs supported earnings growth.

Novelis Continued to Pressure Consolidated Earnings

Novelis remained the weak link in Hindalco’s quarterly performance. Shipments dropped from 957 KT to 844 KT during Q4 FY26. Adjusted EBITDA declined 3% due to lower volumes and operational disruptions.

Still, the company improved EBITDA per tonne to $544 through cost-cutting efforts and lower scrap costs.

Hindalco Share Price Reaction and Market Sentiment

- Hindalco shares fell nearly 2% after Q4 FY26 earnings announcement.

- Investors worried about Novelis losses, US tariff risks, and margin pressure.

- The stock traded around ₹1,087 after results.

- Nuvama and Motilal Oswal remain positive on long-term growth prospects.

- Analysts expect Oswego plant recovery to improve sentiment in FY27.

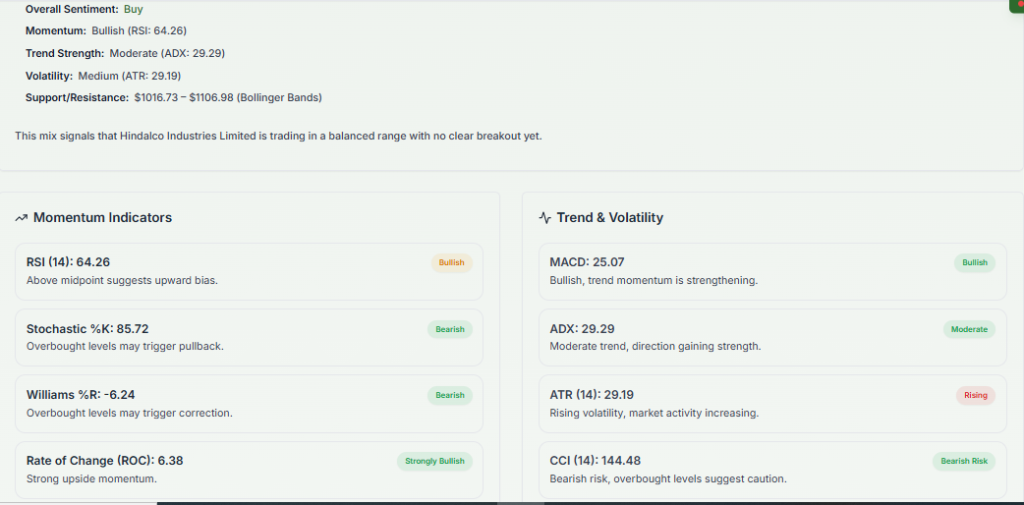

Hindalco Stock Forecast and Technical Analysis

Short-Term Technical Analysis Summary

Based on recent market trends, Hindalco stock continues to trade in a broader bullish structure despite short-term weakness.

Technical indicators currently suggest:

- Immediate support near ₹1,040-1,050

- Resistance around ₹1,130-1,150

- Long-term trend remains positive above 200-day moving average

- Volatility may remain high until Novelis recovery improves visibility

Several traders also noted increased accumulation volume near recent highs.

What Meyka Says About Hindalco Stock?

According to Meyka analysis, Hindalco’s long-term outlook remains tied to aluminium demand growth, India infrastructure spending, and Novelis recovery execution.

Meyka’s AI stock analysis tool highlights:

- Strong domestic business momentum

- Healthy aluminium margins

- Positive long-term EV demand exposure

- Near-term risks from US operations and global metal volatility

The platform also suggests investors monitor Oswego recovery timelines closely before expecting strong upside momentum.

Supporting Insights From Other Analysts

Other analysts remain cautiously optimistic.

ICICI Direct said Hindalco’s India business delivered “record operational performance” despite exceptional losses. Analysts believe cost optimization at Novelis may support future margin recovery.

What the ₹5 Dividend Means for Investors?

Dividend Despite Weak Profit Signals Management Confidence

Hindalco recommended a dividend of ₹5 per share for FY26 even after the sharp profit decline. This move signals that management remains confident about long-term cash flows and business stability.

Dividend-paying metal companies often attract long-term investors because they provide some protection during commodity cycles. Hindalco’s strong India operations likely gave management confidence to maintain shareholder returns despite Novelis-related pressure.

Global Aluminium Market Trends Affecting Hindalco in 2026

Aluminium Prices Remain Volatile

Global aluminium prices stayed volatile during FY26 due to trade tensions, slowing industrial demand, and uncertainty around US tariffs. Metal companies worldwide faced pressure from fluctuating raw material costs and weaker manufacturing activity.

EV and Renewable Energy Demand Still a Long-Term Tailwind

Despite short-term uncertainty, aluminium demand remains strong in fast-growing sectors.

These include:

- Electric vehicles

- Solar infrastructure

- Battery manufacturing

- Lightweight transportation systems

India’s infrastructure push also continues to support domestic aluminium consumption growth.

US Manufacturing Weakness Is Hurting Novelis

North American demand slowed during the quarter. That affected shipment volumes at Novelis. The Oswego disruption worsened the pressure. However, management expects gradual recovery once production normalizes later in 2026.

What Investors Should Watch in Hindalco Going Forward?

Recovery Timeline for Novelis Operations

The biggest trigger for Hindalco shares will be the restart of the Oswego plant. A faster recovery could improve profitability and investor confidence during FY27.

Copper and Domestic Aluminium Demand Growth

India’s infrastructure spending continues to rise. Demand from construction, renewable energy, and EV manufacturing may support Hindalco’s domestic business. The company is also expanding copper and downstream aluminium capacity.

Margin Recovery and Global Metal Prices

Future profitability will depend heavily on:

- Global aluminium prices

- Operational cost control

- US tariff developments

- Novelis shipment recovery

Investors should closely track quarterly margin trends over the next few quarters.

Final Words

Hindalco’s Q4 FY26 results showed strong operational growth but weak bottom-line performance due to Novelis-related losses and one-time charges. While the India aluminium and copper businesses remain strong, investors are closely watching the recovery of US operations.

Long-term demand from EVs, infrastructure, and renewable energy still supports Hindalco’s growth outlook, but near-term volatility may continue to pressure the stock.

Disclaimer:

The content shared by Meyka AI PTY LTD is solely for research and informational purposes. Meyka is not a financial advisory service, and the information provided should not be considered investment or trading advice.

What brings you to Meyka?

Pick what interests you most and we will get you started.

I'm here to read news

Find more articles like this one

I'm here to research stocks

Ask Meyka Analyst about any stock

I'm here to track my Portfolio

Get daily updates and alerts (coming March 2026)