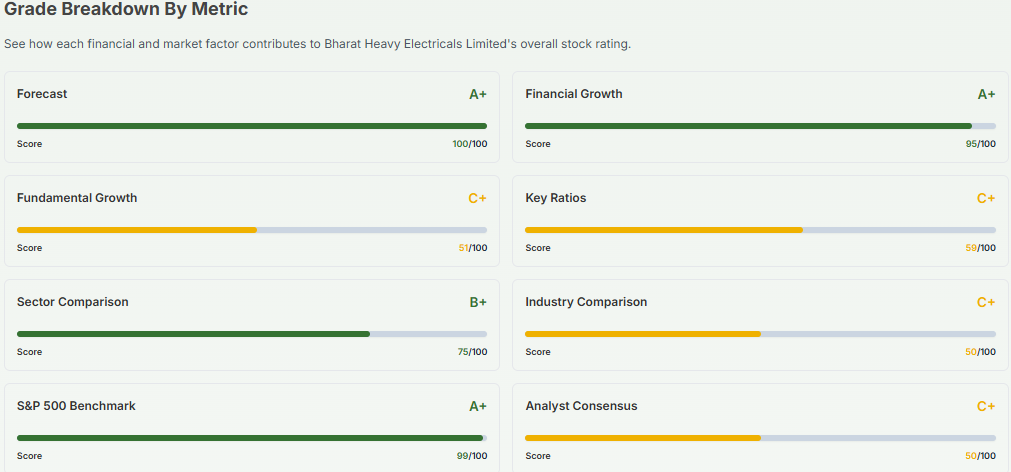

Key Points

BHEL FY26 shows strong recovery with ~18% YoY growth and ₹75,000 crore+ order inflow

Power segment remains dominant, contributing nearly 75-80% of total orders

The industrial segment is rising fast, improving margins, and diversifying

Strong ₹2.4 lakh crore order book ensures long-term revenue visibility

BHEL share has stayed in the spotlight in 2026 due to its strong business recovery. In FY26, the company reported a solid jump in performance with order inflows crossing ₹75,000 crore, reflecting steady demand in India’s power and infrastructure sectors.

As of April 2026, Bharat Heavy Electricals Limited continues to benefit from rising government spending on energy and industrial projects. The company’s order book has also strengthened, giving better visibility for future growth.

This momentum has directly influenced the BHEL share price, which investors are tracking closely for signs of a long-term turnaround.

FY26 Business Update Snapshot: What Changed for BHEL in 2026?

BHEL reported a strong improvement in FY26 performance, supported by higher execution in power projects and fresh industrial orders. As of FY26 results updates released in early 2026, the company showed stable recovery across key segments.

Key financial and operational highlights include:

- Total turnover around ₹32,000+ crore, showing nearly 18% YoY growth

- Order inflow close to ₹75,000 crore in FY26

- Strong order book near ₹2.4 lakh crore, giving multi-year visibility

- Power project execution of nearly 8-9 GW capacity

This improvement reflects rising government capital spending in energy and infrastructure. According to reports from sources like Business Standard and Economic Times Energy, demand for thermal and hybrid power equipment has supported new contracts in FY26.

Why is BHEL gaining more power sector orders in FY26?

The power segment remains the backbone of BHEL’s business. It contributes the majority of the company’s revenue and order inflows.

Key drivers behind power order growth:

- Expansion of coal-based and hybrid energy capacity in India

- Large EPC contracts from NTPC and state utilities

- Replacement demand from aging power plants

- The government’s focus on energy security in the 2025-2026 policy cycle

In FY26, power orders formed nearly 75-80% of total inflows. This shows that while diversification is happening, power still drives core growth.

However, margins in this segment remain moderate due to competition and long execution cycles. Analysts note that execution speed will decide future earnings growth more than order wins.

How is the industrial segment changing BHEL’s growth story?

The industrial business is becoming a key long-term growth driver for BHEL. In FY26, this segment showed stronger momentum compared to earlier years.

Key highlights:

- Industrial orders around ₹15,000-16,000 crore in FY26

- Strong growth in railways, defence, and process industries

- Higher profitability compared to the power segment

Industrial EBIT margins are estimated to be significantly higher than power EPC projects. This improves the overall profitability mix.

Why this matters:

- Reduces dependency on cyclical power demand

- Improves long-term earnings stability

- Supports valuation re-rating potential

Experts believe this diversification is one of the most important structural shifts for BHEL in the last decade.

Is BHEL’s order book strong enough for long-term growth?

Yes, the order book remains one of BHEL’s biggest strengths in FY26.

Order book snapshot:

- Total order book: ~₹2.4 lakh crore

- Strong pipeline from both central and state projects

- Book-to-bill ratio above 6x-7x levels

This large backlog ensures revenue visibility for the next 3-5 years. However, investors must track conversion efficiency. A strong order book is useful only if execution remains consistent. Delays in EPC projects can impact cash flow and margins.

BHEL share price trend: What is the technical setup saying?

BHEL’s share price has shown strong momentum since mid-2025 and continued into 2026, driven by order inflow optimism.

Technical analysis summary:

- Stock is trading above key moving averages in the 2026 trend cycles

- Strong support is seen in previous breakout zones

- Momentum indicators suggest bullish-to-neutral consolidation phases

- Volume spikes indicate institutional interest during order announcements

Overall, the trend is positive but not fully one-sided. The stock often moves in sharp cycles based on order news and execution updates.

AI-based stock analysis insight:

An AI stock analysis tool used for pattern tracking suggests that BHEL is in a “structural recovery phase,” where earnings visibility is improving but volatility remains due to project-based revenue recognition cycles.

What does Meyka say about BHEL share outlook?

According to insights from Meyka.com, an AI-driven market analysis platform, BHEL shows a mixed but improving outlook.

Meyka-style summary:

- Trend: Medium-term bullish recovery

- Key trigger: Execution of large EPC orders in FY26-FY27

- Risk factor: Margin pressure in competitive bids

- Sentiment: Positive but cautious

Meyka’s model highlights that BHEL’s valuation is currently more driven by “future order conversion expectations” rather than current earnings strength.

The platform also flags that industrial diversification could be the biggest long-term re-rating factor if sustained.

Outlook for FY26-FY27: What should investors expect?

The outlook for BHEL depends on three major factors:

- Execution strength: Timely completion of large power projects is critical. Delays can hurt margins.

- Industrial growth expansion: A higher share of railways and defence orders can improve the profitability mix.

- Government capex cycle: Energy and infrastructure spending will directly impact order inflows.

Key risks:

- Competitive pricing pressure in EPC bids

- Working capital stress

- Cyclical nature of power demand

Key positives:

- Strong order visibility

- Diversification beyond power

- Improving operational efficiency

Final Words

BHEL is entering a key transition phase in FY26. The company is no longer just an order-driven PSU, but a recovery story supported by execution and diversification. Strong order inflows and a solid backlog give stability, while industrial growth adds a new earnings angle.

However, the real test lies in execution over the next two years. If delivery improves, BHEL’s share price could see a stronger long-term re-rating phase.

Disclaimer:

The content shared by Meyka AI PTY LTD is solely for research and informational purposes. Meyka is not a financial advisory service, and the information provided should not be considered investment or trading advice.

What brings you to Meyka?

Pick what interests you most and we will get you started.

I'm here to read news

Find more articles like this one

I'm here to research stocks

Ask Meyka Analyst about any stock

I'm here to track my Portfolio

Get daily updates and alerts (coming March 2026)