Key Points

AMD stock has surged 12,941% since 2016, becoming a major AI growth story.

Data center revenue jumped 57% year-over-year in Q1 2026, driven by AI demand.

AMD's valuation remains stretched, with the stock trading near a 200x P/E ratio.

Analysts stay bullish on long-term growth, but competition and high expectations remain key risks.

Advanced Micro Devices (AMD) has been one of the stock market’s biggest success stories, delivering a staggering 12,941% gain since 2016. The chipmaker transformed itself from a struggling semiconductor company into a major player in artificial intelligence and data centers.

As of June 2026, investors remain bullish on AMD’s growth potential, but its lofty valuation has sparked debate across Wall Street. Can strong AI-driven earnings justify the premium price, or is the stock becoming too expensive to ignore?

How AMD Delivered a 12,941% Gain Since 2016?

From Turnaround Story to AI Powerhouse

AMD stock has become one of the biggest success stories in the semiconductor industry. In 2016, the company traded at just a few dollars per share and faced intense competition from Intel and NVIDIA. Since then, CEO Lisa Su has led a remarkable turnaround through product innovation and disciplined execution.

The launch of Ryzen processors helped AMD regain market share in PCs. Later, EPYC server chips strengthened its position in data centers. These products allowed AMD to compete effectively in high-margin markets and improve profitability significantly.

The AI Boom Accelerated the Rally

The rise of artificial intelligence created another growth engine for AMD. Demand for AI accelerators and data-center infrastructure surged throughout 2025 and 2026.

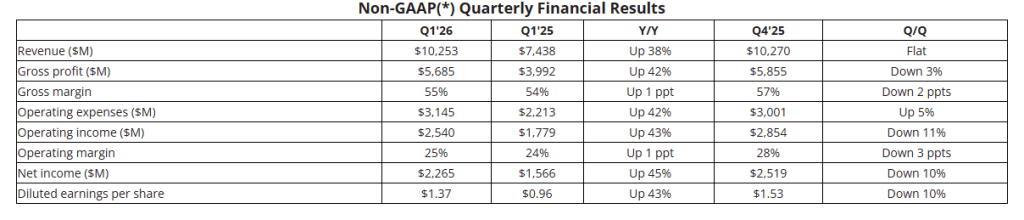

AMD reported first-quarter 2026 revenue of $10.25 billion, up 38% year over year. Data-center revenue climbed 57% to $5.8 billion, highlighting the company’s growing role in AI infrastructure. Q2 revenue guidance of approximately $11.2 billion also exceeded analyst expectations. Sources: CNBC earnings data via investor discussions and earnings coverage.

Why are Investors Paying Attention to AMD’s Valuation?

The P/E Ratio Has Reached Extreme Levels

AMD’s growth has pushed its valuation to unusually high levels. According to CompaniesMarketCap, AMD’s trailing P/E ratio stood near 196 in June 2026. Other financial databases show similarly elevated readings depending on calculation methods.

For comparison, many mature semiconductor companies trade at far lower earnings multiples. Such a premium suggests investors expect years of strong earnings expansion from AMD’s AI and data-center businesses.

What a 204x P/E Ratio Really Means?

A valuation above 200 times earnings signals that investors are paying heavily for future growth. While this can be justified during periods of rapid expansion, it also increases downside risk.

If AI demand slows or revenue growth misses expectations, valuation compression could pressure the stock. High-multiple stocks often experience larger swings because expectations are already very high.

The Bull Case: Why AMD Could Still Have Room to Run

AI Demand Remains Strong

The AI infrastructure market continues to expand rapidly. Enterprises, cloud providers, and technology giants are investing billions into AI computing capacity. Industry spending on AI hardware remains a major tailwind for semiconductor companies.

AMD’s MI-series accelerators and EPYC processors position the company to benefit from this trend. Several analysts believe the AI market is large enough to support multiple winners alongside NVIDIA.

Earnings Growth Is Accelerating

AMD’s financial performance supports much of the bullish narrative. Revenue reached $37.45 billion on a trailing twelve-month basis, while net income rose nearly 125% year over year. Analysts continue to maintain a Strong Buy consensus on the stock.

According to Meyka’s AI stock analysis tool, AMD currently shows a bullish technical trend with strong momentum and buying pressure. The platform rates the stock as a “Buy with caution” because momentum indicators suggest overbought conditions despite strong trend strength.

The Bear Case: Risks That Could Pressure AMD Stock

Expectations May Be Too High

AMD’s biggest risk may be investor expectations. The company must continue delivering strong AI-related growth to justify its premium valuation. Even solid results could disappoint if they fail to exceed Wall Street forecasts.

Competition Is Intensifying

Competition remains fierce across the semiconductor industry. NVIDIA continues dominating AI GPUs, while Intel is working to regain market share. NVIDIA’s recent expansion into AI-focused PC chips also adds new competitive pressure.

What Wall Street and Investors are Saying?

Analysts Remain Optimistic

Many analysts continue to view AMD as a leading AI beneficiary. Strong earnings growth, expanding margins, and data-center momentum support the bullish outlook. Market consensus remains positive despite valuation concerns.

Investor Sentiment Is Divided

Some investors believe AMD’s AI opportunity justifies its premium valuation. Others argue the stock has moved ahead of fundamentals and may face volatility if growth slows. This debate has intensified as AMD approaches new all-time highs.

AMD Stock Outlook for 2026 and Beyond

Key Metrics Investors Should Watch

Investors should focus on:

- Data-center revenue growth

- AI accelerator adoption

- Earnings-per-share expansion

- Gross margin trends

- Competitive positioning against NVIDIA and Intel

Meyka’s technical analysis currently shows strong momentum, but also warns that overbought conditions could trigger short-term pullbacks.

Conclusion

AMD has transformed from a turnaround story into a major AI infrastructure player. Strong earnings growth and rising data-center demand support the bullish case. However, a valuation near 200 times earnings leaves little room for mistakes. Investors should watch AI revenue growth, profitability, and competitive developments closely. If AMD continues executing well, it may justify its premium valuation. If growth slows, volatility could quickly return.

Disclaimer:

The content shared by Meyka AI PTY LTD is solely for research and informational purposes. Meyka is not a financial advisory service, and the information provided should not be considered investment or trading advice.

What brings you to Meyka?

Pick what interests you most and we will get you started.

I'm here to read news

Find more articles like this one

I'm here to research stocks

Ask Meyka Analyst about any stock

I'm here to track my Portfolio

Get daily updates and alerts (coming March 2026)