Key Points

NVIDIA reported $81.6 billion in revenue with 85% year-over-year growth in Q1 FY2027.

Adjusted EPS beat Wall Street estimates as AI demand stayed extremely strong.

Blackwell and Rubin AI platforms continue driving Nvidia’s long-term growth outlook.

Analysts remain bullish on NVDA stock despite valuation and competition concerns.

NVIDIA stock (NASDAQ: NVDA) stayed in the spotlight after the company reported another massive earnings beat in May 2026. The AI chip leader posted $81.6 billion in quarterly revenue, up 85% year over year, while adjusted EPS topped Wall Street estimates once again. Yet the stock reaction surprised many investors. Markets are now asking a bigger question: can Nvidia keep growing at this historic pace as AI spending explodes worldwide?

NVIDIA Q1 FY2027 Earnings Snapshot: Key Numbers

Revenue and EPS Beat Expectations

NVDA delivered another major earnings surprise in its Q1 FY2027 report released on May 20, 2026. The AI chip giant posted quarterly revenue of $81.6 billion, up 85% from the same quarter last year. Non-GAAP earnings per share reached $1.87, beating Wall Street estimates of around $1.75 to $1.78.

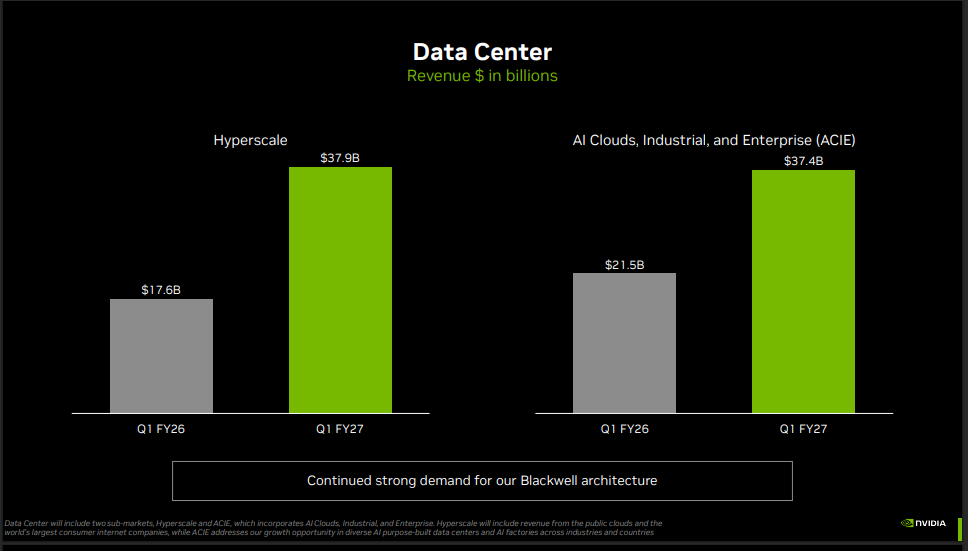

The company’s data center business remained the biggest growth driver. Revenue from that segment climbed to $75.2 billion, showing 92% year-over-year growth. Gross margins also stayed strong near 75%, which helped investors stay confident about Nvidia’s pricing power in the AI market.

NVIDIA also announced:

- An additional $80 billion stock buyback authorization

- A dividend increase from $0.01 to $0.25 per share

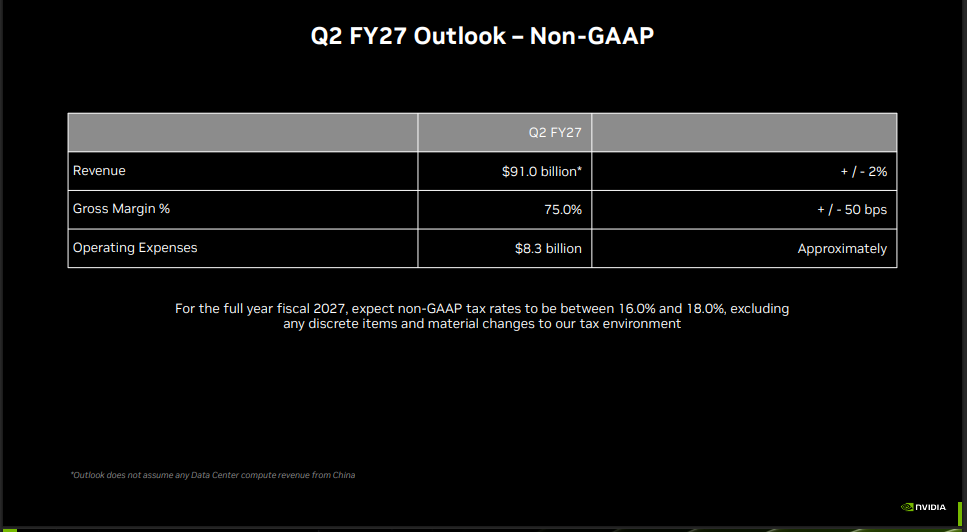

- Strong Q2 FY2027 guidance of about $91 billion in revenue

Why the 85% Revenue Growth Matters?

The 85% growth rate was important because Nvidia is already operating at a massive scale. Many large technology companies struggle to maintain strong growth once revenues cross tens of billions. NVIDIA is doing the opposite.

The latest results marked the company’s third straight quarter of accelerating year-over-year growth. Revenue growth was 62% two quarters ago, then 73%, and now 85%.

This shows that AI spending is still expanding rapidly. Cloud companies like Microsoft, Amazon, Alphabet, and Meta continue investing heavily in AI infrastructure. NVIDIA remains the biggest supplier of advanced AI accelerators, powering large language models and AI agents.

CEO Jensen Huang said the “buildout of AI factories” is accelerating globally. He also stated that agentic AI is now generating real business value across industries.

NVIDIA’s AI Business Is Growing Faster Than Wall Street Expected

- NVIDIA’s data center revenue jumped 92% year over year to $75.2 billion in Q1 FY2027.

- The segment now generates over 90% of Nvidia’s total revenue.

- Growth was driven by hyperscaler AI spending, Blackwell demand, and enterprise AI adoption.

- Networking revenue reached $14.8 billion with strong NVLink and InfiniBand demand.

- NVIDIA now focuses on reporting on the Data Center and Edge Computing markets.

- Jensen Huang said AI infrastructure demand has become “parabolic.”

- NVIDIA is expanding through Blackwell, Rubin architecture, AI networking, and enterprise AI software.

- Analysts increasingly view Nvidia as a core AI infrastructure rather than a traditional chipmaker.

Why NVDA Stock Didn’t Surge Despite a Massive Earnings Beat?

Wall Street Expectations Were Already Extremely High

Even though Nvidia crushed estimates again, the stock reaction stayed mixed after earnings. That happened because expectations had already become extremely high heading into the report.

Investors expected another strong quarter after several years of explosive AI-driven growth. A simple earnings beat was no longer enough to create a huge rally.

Wall Street focused more on:

- Future guidance

- Gross margins

- China-related risks

- Long-term AI demand sustainability

- Competitive threats from AMD and hyperscalers

Some traders also expected Nvidia to deliver an even larger upside surprise because the stock had already rallied strongly before earnings.

Profit-Taking and Valuation Concerns

Another reason for the muted stock move was valuation pressure. NVIDIA is now one of the world’s most valuable companies, with a market cap above $5 trillion.

At these levels, investors closely watch whether growth can remain this strong for several more years. Some portfolio managers locked in profits after the earnings release. Others questioned:

- Whether hyperscaler AI spending could slow later

- If competition will pressure margins

- How export restrictions could affect China’s revenue

Despite these concerns, many analysts still believe Nvidia has years of AI-driven expansion ahead.

NVIDIA’s Q2 Guidance Could Be the Bigger Story

Revenue Guidance Topped Consensus Again

NVIDIA’s Q2 FY2027 forecast became one of the strongest parts of the earnings report. The company guided for roughly $91 billion in quarterly revenue, well above Wall Street expectations.

The guidance also excluded any China data center compute revenue. That detail was important because it showed Nvidia could still grow aggressively despite export restrictions.

The company expects:

- Gross margin near 75%

- Operating expenses are around $8.5 billion

- Continued AI infrastructure expansion globally

Analysts are Watching Margins Closely

Margins became another key focus after earnings. NVIDIA maintained gross margins near 75%, which remains unusually high for a hardware company.

This matters because investors want proof that Nvidia can keep premium pricing power while expanding production.

Analysts are also tracking:

- Manufacturing costs

- Blackwell rollout expenses

- Networking integration costs

- Future Rubin platform investments

Several research firms said stable margins suggest Nvidia still has major pricing control in the AI accelerator market.

Blackwell, Rubin, and the Next Phase of Nvidia’s AI Expansion

The Blackwell Demand Remains a Major Catalyst

Blackwell Systems continues to drive investor excitement. NVIDIA said demand for Blackwell infrastructure remains extremely strong across hyperscalers and enterprises.

Many customers are scaling beyond AI training and moving into:

- AI inference

- autonomous AI agents

- enterprise copilots

- robotics

- industrial AI systems

Analysts expect Blackwell-related revenue to contribute tens of billions during FY2027.

Rubin Launch Expectations are Growing

NVIDIA also confirmed progress on its next-generation Rubin platform. Rubin is expected to become a major driver of AI computing in the coming years.

The company believes Rubin systems will support:

- Larger AI models

- Faster inference

- Agentic AI workloads

- Physical AI applications

According to Nvidia, Rubin demand is already building among hyperscalers and sovereign AI projects worldwide.

This is one reason many investors continue using advanced platforms like the AI stock analysis tool from Meyka to monitor Nvidia’s technical momentum and future AI growth trends.

NVDA Stock Forecast and Technical Analysis Summary

What Meyka Says About NVDA Stock?

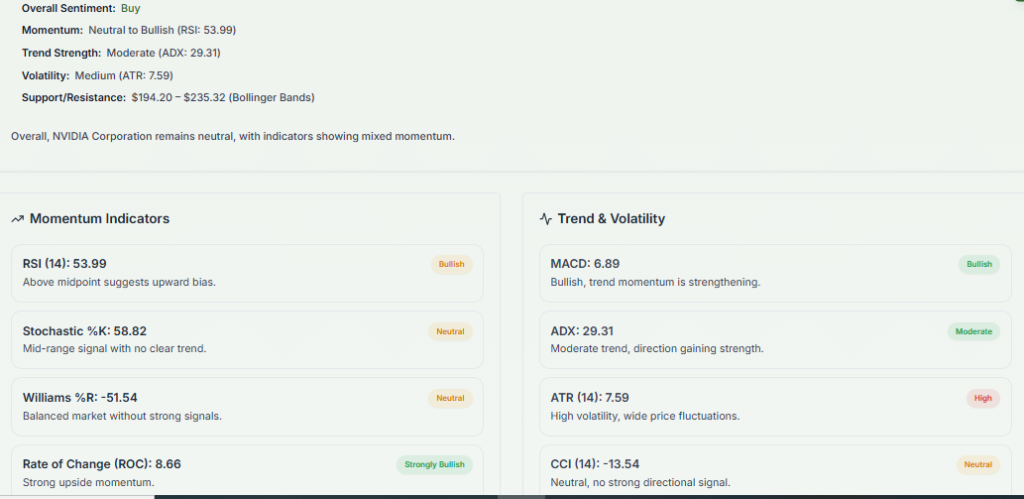

According to Meyka’s NVDA technical analysis page, Nvidia stock currently trades in a neutral range overall, although momentum indicators remain bullish.

Meyka’s latest technical summary showed:

- RSI near 67.77

- Bullish momentum signals

- Weak trend strength based on ADX

- Medium volatility levels

Meyka also previously projected around 33% upside potential for NVDA stock earlier in 2026 as AI demand continued strengthening.

Supporting Insights From Other Analysts

Other analysts also remain optimistic about Nvidia’s long-term direction. TIKR estimated a long-term valuation target of $486 based on future AI revenue expansion.

Some independent market researchers believe Nvidia could remain the dominant AI accelerator provider through the end of the decade because of:

- software ecosystem advantages

- CUDA dominance

- networking integration

- large enterprise adoption

However, analysts continue warning that volatility could remain high due to Nvidia’s premium valuation and fast-moving AI competition landscape.

What Nvidia Earnings Mean for AI Stocks and the Broader Market?

AI Infrastructure Spending Remains Strong

NVIDIA’s earnings report reinforced the broader AI investment narrative across financial markets. The company’s results showed that:

- AI infrastructure spending is still accelerating

- Hyperscalers remain aggressive buyers

- Enterprise AI adoption is expanding globally

- AI networking demand continues to rise

Many semiconductor stocks moved higher ahead of Nvidia earnings because investors viewed the report as a key test for overall AI demand.

Nvidia Remains the AI Market Bellwether

NVIDIA earnings now influence sentiment across the entire AI market.

Investors use Nvidia’s results to evaluate:

- cloud computing demand

- AI software growth

- semiconductor trends

- enterprise AI spending

As long as Nvidia continues posting strong revenue growth and maintaining high margins, many investors believe the broader AI boom still has room to expand.

Wrap Up

NVIDIA’s latest earnings once again proved its dominance in the AI industry. Strong revenue growth, rising AI demand, and bullish guidance kept Wall Street focused on NVDA stock. While valuation concerns and competition remain risks, Nvidia continues to lead the global AI infrastructure market through Blackwell, Rubin, and expanding enterprise adoption.

Disclaimer:

The content shared by Meyka AI PTY LTD is solely for research and informational purposes. Meyka is not a financial advisory service, and the information provided should not be considered investment or trading advice.

What brings you to Meyka?

Pick what interests you most and we will get you started.

I'm here to read news

Find more articles like this one

I'm here to research stocks

Ask Meyka Analyst about any stock

I'm here to track my Portfolio

Get daily updates and alerts (coming March 2026)