Key Points

Wall Street expects NVIDIA revenue to reach $78.75B with EPS at $1.76 in Q1 FY2027.

Blackwell AI chips remain the biggest growth driver for NVDA stock in 2026.

Options traders expect a major 6%–7% stock move after earnings results.

Investors are closely watching guidance, margins, and the AI demand outlook for 2027.

On May 20, 2026, investors across Wall Street are closely watching NVIDIA as the AI chip giant prepares to release its latest earnings report. Analysts expect quarterly revenue to reach nearly $78.75 billion, while earnings per share could jump to $1.76 amid booming demand for AI infrastructure. The results may not only move NVDA stock but also shape sentiment across the global tech sector. Traders are now waiting to see whether NVIDIA can once again beat expectations and extend its dominance in the fast-growing AI market.

Why NVIDIA Earnings Matter More Than Ever in 2026?

Why is Wall Street closely watching NVIDIA earnings?

NVIDIA has become the biggest symbol of the global AI boom. The company now sits at the center of the artificial intelligence infrastructure market. Its GPUs power large AI models, cloud computing systems, and enterprise AI platforms used by companies worldwide.

NVIDIA is scheduled to report fiscal Q1 FY2027 earnings after the market closes on May 20, 2026. Analysts expect another record quarter as AI spending remains strong across the technology sector. Reuters reported that investors expect nearly 79% year-over-year revenue growth this quarter.

The company’s earnings now influence:

- Semiconductor stocks

- AI infrastructure companies

- Cloud computing firms

- Nasdaq market sentiment

- AI-focused ETFs

Many traders see NVIDIA earnings as a health check for the entire AI industry.

How much market impact could NVIDIA have?

The options market expects NVIDIA shares to move about 6.5% after earnings. That equals nearly a $355 billion swing in market value. Reuters noted that this would be larger than the entire market capitalization of most S&P 500 companies.

This shows how important NVIDIA has become for global markets. Even strong earnings may not guarantee a stock rally because investor expectations remain extremely high.

NVIDIA Q1 FY2027 Expectations: Revenue, EPS, and Growth Forecasts

What revenue and EPS does Wall Street expect?

Analysts expect NVIDIA to deliver another historic quarter. Consensus estimates project currently:

- Revenue: about $78.4 billion to $78.75 billion

- EPS: around $1.75 to $1.76

- Revenue growth: nearly 79% year-over-year

- Profit growth: more than 80% year-over-year

Several earnings tracking platforms confirmed these expectations ahead of the report.

The expected growth comes mainly from AI data center demand. Hyperscalers continue spending aggressively on advanced AI infrastructure.

Which business segment matters most?

The data center division remains NVIDIA’s biggest earnings engine. According to investor discussions and recent filings, this segment contributed over 90% of total quarterly revenue in recent periods.

Investors will closely watch:

- Data center revenue growth

- Blackwell GPU shipments

- Gross margins

- AI cloud partnerships

- China sales outlook

- FY2027 guidance

Strong guidance may matter more than headline earnings numbers.

Can NVIDIA keep beating expectations?

NVIDIA has built a strong history of outperforming Wall Street estimates. EarningsSpike data shows the company beat analyst EPS estimates in 19 of the last 24 quarters. Revenue also exceeded expectations in 22 of the previous 24 quarters. That consistency is one reason investors remain bullish despite high valuations.

Blackwell GPUs Could Be the Biggest Earnings Driver

Why are Blackwell chips so important?

The Blackwell platform is now the biggest growth catalyst for NVIDIA. The company launched Blackwell as its next-generation AI computing architecture designed for large AI training and inference workloads.

Demand appears extremely strong. Several analyst reports and investor discussions suggest Blackwell orders may already stretch deep into 2026. Large cloud providers continue expanding AI infrastructure at a rapid pace.

Which companies are driving AI demand?

Major technology companies remain NVIDIA’s largest customers. These include:

These companies continue investing billions into AI infrastructure and data centers. Reuters reported that AI infrastructure spending could approach $700 billion this year.

Why do margins matter this quarter?

Investors are becoming more focused on profitability. Rising memory prices and advanced packaging costs could pressure margins going forward.

Investopedia recently highlighted memory shortages as one of the biggest concerns heading into earnings.

If margins weaken, the stock could become volatile even if revenue beats estimates.

Risks and Concerns Heading Into Earnings

Is competition becoming a real threat?

NVIDIA still dominates AI chips, but competition is rising quickly. Key rivals now include:

- AMD

- Intel

- Amazon with Trainium chips

- Alphabet with TPU systems

Reuters reported that investors are paying closer attention to AI inference workloads, where competition is growing faster.

Could valuation pressure hurt NVDA stock?

NVIDIA stock has already gained strongly in 2026. According to Reuters, shares are up about 19% year-to-date. The company now trades at premium valuation levels:

- Forward P/E above 23x

- Market cap above $5 trillion

- Strong Buy analyst consensus

High expectations create pressure. Investors may demand exceptional guidance to push shares higher.

What about China and geopolitical risks?

China remains a major concern for investors. The U.S. government continues to tighten AI chip export restrictions. Analysts want updates on:

- China revenue exposure

- Export approvals

- Supply chain risks

- Future licensing rules

These issues could affect long-term growth projections.

What Analysts and Traders Expect After the Report?

Could NVIDIA stock make a massive move?

Options traders expect heavy volatility after earnings. Reuters reported that the market expects a 6.5% move in either direction after the results.

Historically, NVIDIA shares often move sharply after earnings announcements. Interestingly, the stock declined after several recent earnings reports despite strong numbers because expectations were already elevated.

What are analysts saying about NVDA stock?

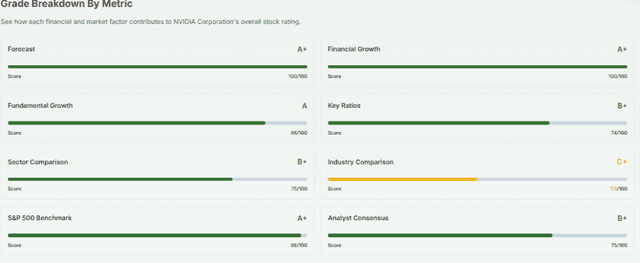

Wall Street sentiment remains highly bullish. According to StockAnalysis, analysts currently maintain a Strong Buy consensus with an average price target near $272.

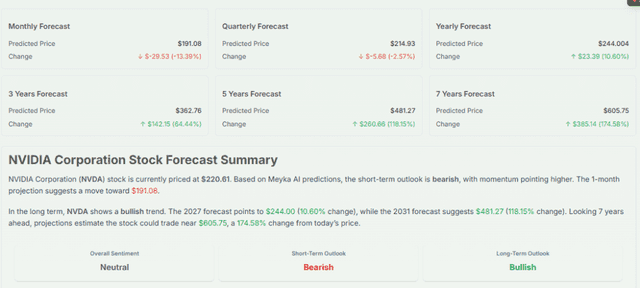

Meyka’s earlier NVDA analysis projected a yearly target of around $246 based on its AI stock analysis tool, though the platform also warned about downside risks if momentum slows.

Technical Analysis Summary

Current technical indicators suggest:

- Strong long-term uptrend remains intact

- AI demand continues to support momentum

- Support zones remain near previous breakout levels

- Earnings volatility may create sharp short-term swings

Traders are closely watching guidance for confirmation of continued AI spending growth.

What Meyka Says?

Meyka NVDA Analysis highlighted that NVIDIA’s valuation already reflects strong AI optimism. The report noted that future upside will likely depend on:

- Blackwell shipment growth

- Stable margins

- Strong FY2027 guidance

- Continued hyperscaler AI spending

Meyka also warned that slowing AI capex or weaker guidance could increase volatility.

Key Questions Jensen Huang Must Answer on the Earnings Call

What will investors focus on most?

CEO Jensen Huang will face several major questions during the earnings call. Investors want updates on:

- Blackwell production capacity

- AI inference opportunities

- Rubin chip roadmap

- Gross margin outlook

- China strategy

- Long-term AI demand trends

Why does guidance matter more than results?

Strong quarterly numbers alone may not satisfy investors anymore. Markets now care more about:

- Q2 revenue guidance

- 2027 growth outlook

- AI spending sustainability

- Future profit margins

A weaker-than-expected forecast could pressure shares even if earnings beat estimates.

Final Words

NVIDIA’s earnings report could become one of the most important market events of 2026. Investors expect another quarter of explosive AI-driven growth, with revenue projected near $79 billion and EPS around $1.76. Still, the focus now goes beyond headline numbers.

Markets want proof that Blackwell demand, margins, and hyperscaler spending can stay strong through 2027. The results and guidance may shape sentiment across AI, semiconductor, and technology stocks for the rest of the year.

Disclaimer:

The content shared by Meyka AI PTY LTD is solely for research and informational purposes. Meyka is not a financial advisory service, and the information provided should not be considered investment or trading advice.

What brings you to Meyka?

Pick what interests you most and we will get you started.

I'm here to read news

Find more articles like this one

I'm here to research stocks

Ask Meyka Analyst about any stock

I'm here to track my Portfolio

Get daily updates and alerts (coming March 2026)