Key Points

IndiGo reported a Q4 FY26 net loss of ₹2,537 crore, versus a ₹3,067 crore profit a year earlier.

Despite the loss, IndiGo shares surged more than 5% as investors focused on future growth.

Revenue from operations rose to ₹22,438 crore, showing resilient travel demand.

Analysts remain positive on IndiGo due to its market leadership, fleet expansion, and long-term aviation growth outlook.

IndiGo surprised investors on May 29, 2026, when its shares climbed more than 5% despite reporting a quarterly loss of ₹2,537 crore for the March quarter. While the headline numbers looked weak, the market focused on factors beyond the earnings miss.

Strong revenue performance, growth prospects, and positive analyst views helped boost confidence in the airline’s future. So why did investors cheer a company that posted a bigger loss? The answer reveals an important story about market expectations and long-term growth.

IndiGo Q4 FY26 Results Overview

Key Financial Highlights

InterGlobe Aviation, the parent company of IndiGo, reported a consolidated net loss of ₹2,536.9 crore for the March quarter (Q4 FY26). This was a sharp reversal from the ₹3,067.5 crore profit recorded in the same quarter last year. The results were announced on May 29, 2026.

Revenue from operations still increased 1.3% year-over-year to ₹22,438.4 crore, showing that demand remained resilient despite several challenges. Total income rose to ₹23,830.7 crore during the quarter.

What Hurt Earnings?

The biggest factor behind the loss was a large foreign exchange hit. IndiGo reported a forex loss of about ₹4,823 crore as the Indian rupee weakened against the US dollar. Operational disruptions linked to Middle East airspace issues also increased costs.

In addition, exceptional expenses related to labor code implementation affected profitability. Excluding forex and exceptional items, the airline would have reported a profit of about ₹1,921 crore, highlighting that the core business remained profitable.

Why Did IndiGo Stock Jump More Than 5%?

Investors Looked Beyond the Quarterly Loss

Markets often focus on future earnings rather than past results. That is exactly what happened with IndiGo. Despite the headline loss, investors saw strong signs of business stability. Revenue continued to grow, capacity increased 3.4%, and management remained confident about long-term demand.

The stock climbed more than 5% and touched around ₹4,634 on June 1, 2026. Analysts also noted that most of the loss came from temporary factors such as forex volatility rather than weak passenger demand.

Brokerages Remain Positive

Several leading brokerages maintained bullish views after the earnings release. Goldman Sachs reiterated its “Buy” rating and set a target price of ₹5,200, implying meaningful upside from current levels. Jefferies and other analysts highlighted IndiGo’s dominant position in India’s aviation market, strong balance sheet, and expansion plans.

Analysts believe that improving aircraft availability, international route growth, and better pricing could support earnings recovery in the coming quarters.

Strong Market Confidence

Investors appear to believe that IndiGo’s long-term growth story remains intact. India’s aviation sector continues to be one of the fastest-growing in the world. Domestic air travel demand remains strong, and international traffic is recovering steadily. These trends helped offset concerns about the quarterly loss.

What Management and Investors are Watching Next?

Currency and Fuel Costs Remain Critical

Foreign exchange movements will remain a major factor for IndiGo because a large portion of its aircraft lease obligations are denominated in US dollars. Fuel prices are another key variable. Any sharp rise in aviation turbine fuel costs could pressure margins.

Management has indicated that cost control and operational efficiency will remain major priorities throughout FY27.

Passenger Growth and Capacity Expansion

IndiGo carried 31.6 million passengers during the quarter despite operational challenges. The airline continues to expand its fleet and network. Capacity increased to 43.6 billion available seat kilometers (ASKs), demonstrating management’s confidence in future demand.

The company’s international expansion strategy remains an important growth driver for the coming years.

FY27 Profit Recovery Potential

Many analysts expect FY27 earnings to improve if forex pressures ease. Lower exceptional costs, stronger international operations, and continued passenger growth could help margins recover. The outlook remains favorable despite short-term volatility.

What does this mean for IndiGo Investors?

Bull vs Bear Case

Bull Case

- Market leader in Indian aviation.

- Strong revenue growth despite challenges.

- Positive analyst recommendations.

- Expanding international network.

- Rising long-term travel demand.

Bear Case

- Currency fluctuations remain a risk.

- Fuel prices can hurt profitability.

- Geopolitical disruptions may affect routes.

- Earnings can remain volatile in the short term.

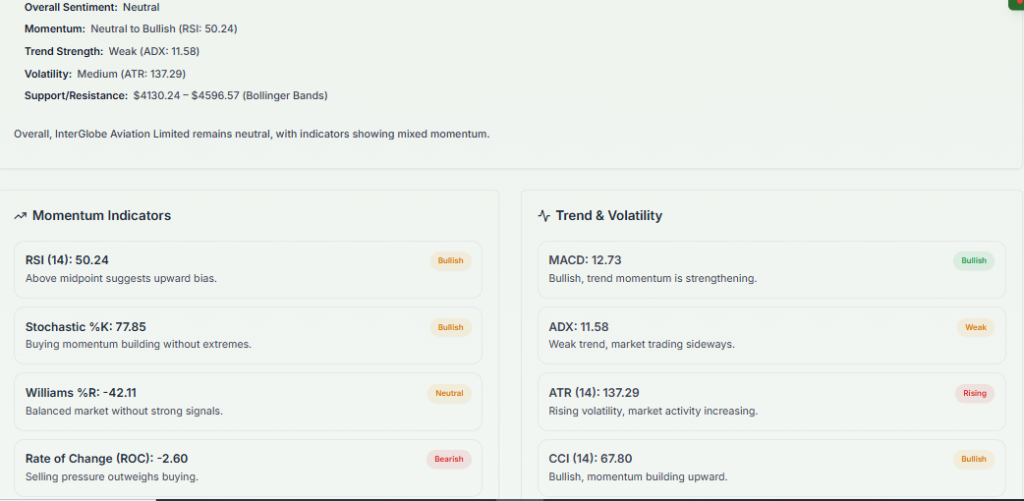

IndiGo Stock Details, Technical Analysis, and Forecast

According to market data on June 1, 2026, IndiGo shares traded near ₹4,634 after the post-results rally. Technical indicators suggest the stock remains in a broader uptrend, supported by strong institutional interest. Momentum has improved after the earnings reaction, though investors should monitor resistance levels near recent highs.

Meyka’s AI stock analysis tool highlights that IndiGo’s long-term outlook remains supported by strong industry demand, fleet expansion, and market leadership. Other analysts broadly agree that temporary forex-related losses do not change the company’s long-term growth potential.

What Meyka Says?

Meyka’s view remains constructive on IndiGo because the latest loss was largely driven by external factors rather than weakness in the airline’s core operations. Continued growth in passenger demand and capacity expansion could support earnings recovery over the next few quarters.

Final Words

IndiGo’s March-quarter loss grabbed headlines, but investors focused on the airline’s strong underlying business and future growth potential. With rising passenger demand, ongoing fleet expansion, and positive analyst sentiment, the market remains optimistic about FY27.

If forex pressures ease and operating conditions improve, IndiGo could be well positioned for a profitability rebound in the coming quarters.

Disclaimer:

The content shared by Meyka AI PTY LTD is solely for research and informational purposes. Meyka is not a financial advisory service, and the information provided should not be considered investment or trading advice.

What brings you to Meyka?

Pick what interests you most and we will get you started.

I'm here to read news

Find more articles like this one

I'm here to research stocks

Ask Meyka Analyst about any stock

I'm here to track my Portfolio

Get daily updates and alerts (coming March 2026)