Key Points

CMPDI Q4 FY26 net profit fell 32% YoY to ₹187 crore despite revenue growth

Shares dropped nearly 4% after results due to margin pressure and rising costs

Company announced ₹1.06 per share final dividend, supporting investor sentiment

Outlook remains mixed with stable demand but weak profitability and cost concerns.

On April 21-22, 2026, CMPDI shares fell nearly 4% in early trade after the company reported its Q4 FY26 results. Net profit dropped 32% year-on-year to ₹187 crore, even as revenue showed steady growth. Investors reacted quickly to the weak earnings trend and rising cost pressure.

However, the company also announced a final dividend of ₹1.06 per share, which offered some support to sentiment. CMPDI, a key PSU mining consultancy firm linked with Coal India, is now in focus as markets assess its mixed performance. The latest results raise important questions about margins, costs, and future earnings stability. The stock remains under close watch by investors today.

CMPDI Q4 FY26 Results Snapshot – Profit vs Revenue Divergence

CMPDI reported its Q4 FY26 results on April 21, 2026. The numbers showed a clear gap between revenue growth and profit performance. Net profit stood at ₹187 crore, down 32% year-on-year. Revenue, however, increased to around ₹827-853 crore, showing steady demand for mining consultancy and engineering services.

The key takeaway is margin pressure.

- Profit fell sharply despite higher sales

- Revenue grew around 10–11% YoY

- Expenses rose significantly in the same period

- EPS declined compared to last year

This mix signals that operational costs are rising faster than income generation. Investors are now closely watching whether this is a one-time spike or a long-term efficiency issue.

What caused CMPDI’s profit to drop by 32%?

The main reason behind the profit decline is cost inflation. CMPDI’s operating expenses rose sharply during the quarter.

Key pressure points:

Employee-related expenses increased significantly. Project execution costs also went higher due to ongoing consultancy work. Administrative overheads added further pressure.

Another factor is fixed cost rigidity. CMPDI operates in long-cycle infrastructure and mining planning projects. These do not adjust quickly to cost changes.

This created a situation where:

- Revenue grew steadily

- But expenses grew faster

- Profit margins shrank

The result is a 32% drop in net profit despite strong top-line performance.

Revenue growth story: Why the business is still expanding

Even with profit pressure, CMPDI’s core business remains stable. Demand for mining planning and consultancy services continues across PSU mining projects.

Growth drivers include:

- Ongoing Coal India-linked exploration work

- Increased focus on mine modernization

- Environmental and engineering consultancy demand

- Long-term government-backed infrastructure planning

Revenue growth of nearly 10–11% shows that core operations are intact. The concern is not demand. The concern is efficiency.

This is why analysts say CMPDI is in a “growth with margin compression” phase.

Dividend announcement: What does it mean for investors?

CMPDI declared a final dividend of ₹1.06 per share for FY26, subject to approval. This is important for investor sentiment because:

- It signals stable cash flow

- It rewards shareholders despite weak profits

- It supports PSU dividend expectations

Dividend stocks in the PSU space often attract long-term investors. Even during profit dips, payouts help stabilize sentiment.

However, investors should note that dividend sustainability depends on future profit recovery.

Why did CMPDI shares fall after results?

CMPDI shares declined nearly 4% in early trade after the Q4 announcement on April 22, 2026. The market reaction was driven by:

- Sharp 32% profit decline

- Rising cost concerns

- Weak margin outlook

- Lack of strong forward guidance

Short-term traders booked profits quickly. Long-term investors stayed cautious but did not exit aggressively due to dividend support. The stock is now in a wait-and-watch zone.

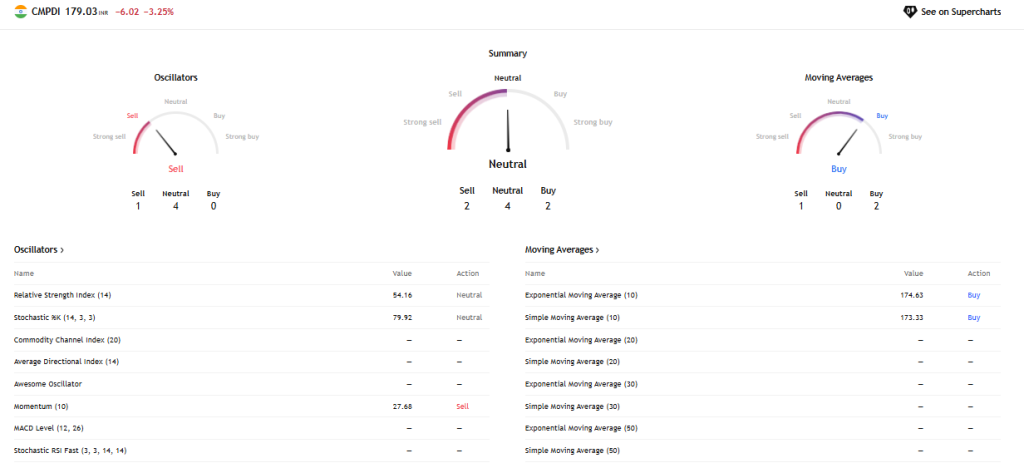

Technical analysis and Meyka AI stock insight

From a technical perspective, CMPDI shows short-term weakness after the earnings release. Price action indicates:

- Resistance near recent post-results highs

- Support forming at lower trading bands after the 4% drop

- Volume spike during sell-off, indicating profit booking

However, PSU-linked AI screening models similar to the AI stock analysis tool approach used in Meyka-style systems suggest:

- Neutral short-term outlook

- Stable long-term fundamentals due to government-linked projects

- Earnings recovery depends on cost control, not revenue expansion

Other market analysts from PSU tracking reports (such as exchange commentary and brokerage notes) highlight the same pattern: strong demand visibility but weak margin efficiency in FY26.

Investor sentiment and future outlook

The outlook for CMPDI depends on two key factors.

- Cost control recovery: If employee and operational costs stabilize, margins can recover quickly.

- Project pipeline strength: Coal India-linked consultancy demand remains strong, which supports revenue stability.

Short-term expectations:

- Volatility likely to continue

- Stock may remain range-bound

- Earnings reactions will dominate sentiment

Long-term expectations:

- Stable PSU-backed business model

- Moderate but consistent dividend flow

- Gradual margin improvement if efficiency improves

CMPDI is currently not a high-growth story. It is a steady PSU income play with cyclical earnings pressure.

Final Words

CMPDI’s Q4 FY26 results highlight a clear mismatch between revenue growth and profitability. While income rose steadily, rising costs pulled net profit down by 32%. The 4% share decline reflects short-term market caution.

However, the dividend announcement and stable project pipeline offer some balance. Going ahead, CMPDI’s performance will depend mainly on cost control and margin recovery rather than demand growth.

Disclaimer:

The content shared by Meyka AI PTY LTD is solely for research and informational purposes. Meyka is not a financial advisory service, and the information provided should not be considered investment or trading advice.

What brings you to Meyka?

Pick what interests you most and we will get you started.

I'm here to read news

Find more articles like this one

I'm here to research stocks

Ask Meyka Analyst about any stock

I'm here to track my Portfolio

Get daily updates and alerts (coming March 2026)