Key Points

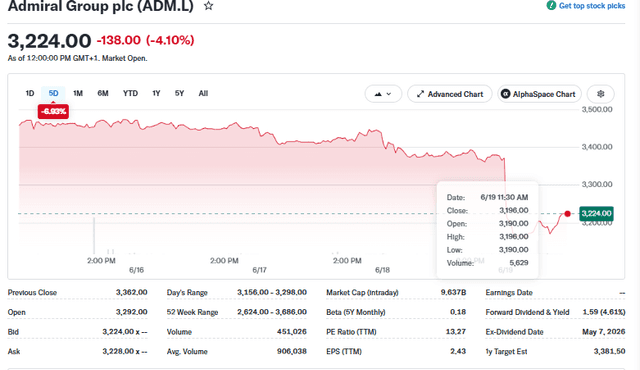

Admiral shares fell 4% after RBC downgraded the stock and cut its price target.

RBC lowered earnings forecasts and flagged weaker dividend outlook concerns.

UK motor insurance competition is pressuring margins and growth.

Other analysts also show cautious sentiment on Admiral’s near-term outlook.

Admiral Group shares came under pressure after RBC Capital Markets downgraded the stock and reduced its price target to 3,450p, triggering a sharp 4% decline in trading. The move reflects growing concerns about future earnings growth, dividend prospects, and challenges in the UK motor insurance market.

As investors reassess the insurer’s outlook in June 2026, the downgrade raises important questions about whether Admiral can maintain its strong performance or faces a tougher road ahead.

What Triggered the 4% Drop in Admiral Shares?

RBC Downgrades Admiral’s Rating

Admiral Group shares came under pressure after RBC Capital Markets downgraded the stock from “Outperform” to “Sector Perform.” The downgrade reflected a more cautious view on future earnings growth and shareholder returns. RBC argued that stronger evidence of a recovery in earnings would be needed before the stock could outperform again. This shift in analyst sentiment quickly caught investors’ attention and weighed on the share price.

Price Target Reduction Signals Limited Upside

RBC also reduced its price target. The bank cut its valuation from 3,600p to 3,100p after lowering its earnings expectations and dividend forecasts. Analysts use price targets to estimate a stock’s fair value over the next 12 months. A lower target often signals reduced confidence in near-term growth prospects.

RBC also lowered its valuation multiple from 15x earnings to 13x earnings. That is well below Admiral’s long-term average valuation of around 17x earnings.

Immediate Market Reaction

The downgrade triggered a sharp sell-off. Investors reacted to concerns about slower profit growth and weaker special dividends. The decline also reflected broader caution toward UK insurance stocks facing competitive pricing pressure.

Market participants closely follow broker recommendations because they can influence institutional investment decisions and market sentiment.

RBC’s Key Concerns About Admiral Group

Why Is the Dividend Outlook Under Pressure?

One of RBC’s biggest concerns involves Admiral’s dividend policy. The insurer plans to buy shares from the market to fund employee share schemes rather than issuing new shares. While this may benefit existing shareholders in some ways, it reduces excess capital that could have been used for special dividends.

As a result, RBC lowered its dividend forecasts. The bank expects lower shareholder payouts over the next several years compared with previous estimates.

Earnings Forecast Cuts Raise Questions

RBC reduced its earnings-per-share forecasts by around 1% for FY2025 and 4% for FY2026 and FY2027. The bank cited a tougher competitive environment and slower premium growth in the UK motor insurance market.

Lower earnings estimates matter because they directly affect valuation models. When analysts cut profit forecasts, they often reduce target prices as well.

For investors using an AI stock analysis tool, earnings revisions remain one of the most important indicators to monitor because they often signal changing business conditions before financial results are released.

Competitive UK Motor Insurance Market

The UK motor insurance sector remains highly competitive. Premium growth has slowed after a period of strong pricing increases. Insurers are now competing harder to attract customers while managing claims inflation and regulatory pressures.

RBC believes this environment could limit margin expansion and make it harder for Admiral to deliver strong earnings growth in the near term.

How Does This Compare With Other Analyst Views?

Growing Analyst Caution Around Admiral

RBC is not alone. Several major investment banks have recently become more cautious on Admiral. Goldman Sachs downgraded the stock from Buy to Sell and reduced its target price. UBS also adopted a more neutral stance due to concerns about UK insurance pricing trends.

These moves suggest that analysts are increasingly focused on industry challenges rather than past performance.

Market Consensus vs RBC Outlook

RBC’s forecasts are more conservative than many market estimates. The bank expects slower earnings growth and lower dividend distributions than broader consensus projections.

However, not all analysts share the same concerns. Some believe improving underwriting performance and disciplined pricing could support a recovery over the medium term.

Investor Sentiment Trends

Investor sentiment remains mixed. While some traders view the pullback as a warning sign, others see value in Admiral’s strong market position and long-term track record.

Recent market discussions have focused on dividend sustainability, earnings momentum, and the outlook for UK motor insurance pricing.

What Investors Should Watch Next?

Upcoming Earnings and Dividend Announcements

Future earnings reports will be critical. Investors will look for updates on premium growth, claims costs, and dividend guidance. Any improvement in these areas could help rebuild confidence.

UK Motor Insurance Pricing Trends

Pricing trends remain the biggest driver of profitability. If premium rates stabilize and claims inflation eases, Admiral could see stronger margins and earnings growth.

Potential Catalysts for Recovery

Several factors could support the stock:

- Faster earnings growth than expected

- Strong underwriting results

- Improved dividend visibility

- Better pricing conditions in UK motor insurance

Admiral Stock Forecast and Technical Analysis Summary

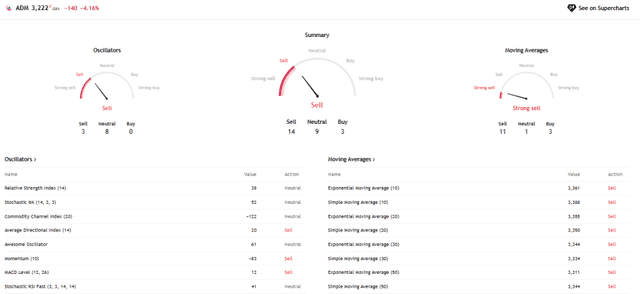

Admiral remains one of the UK’s leading insurance companies. Current analyst views are mixed, with targets ranging from bearish estimates near 3,000p to more optimistic forecasts above 3,500p. Recent technical indicators suggest investors are waiting for clearer earnings momentum before driving a sustained upward trend.

What Meyka Says?

Meyka’s stock-analysis approach generally focuses on earnings trends, analyst revisions, valuation metrics, and market sentiment. Recent analyst downgrades and reduced dividend expectations point to caution in the near term.

However, Admiral’s strong brand, established customer base, and long-term profitability remain important strengths that investors should not ignore.

Conclusion

Admiral’s share-price decline highlights growing concerns about earnings growth, dividend sustainability, and competitive pressure in the UK motor insurance market. RBC’s downgrade added to a broader wave of analyst caution, making future earnings updates especially important.

While short-term challenges remain, Admiral still benefits from a strong market position and a proven operating model. Investors should closely monitor earnings revisions, dividend guidance, and industry pricing trends to determine whether the recent weakness represents a warning sign or a long-term opportunity.

Disclaimer:

The content shared by Meyka AI PTY LTD is solely for research and informational purposes. Meyka is not a financial advisory service, and the information provided should not be considered investment or trading advice.

What brings you to Meyka?

Pick what interests you most and we will get you started.

I'm here to read news

Find more articles like this one

I'm here to research stocks

Ask Meyka Analyst about any stock

I'm here to track my Portfolio

Get daily updates and alerts (coming March 2026)