Shares of Chinese AI developer Zhipu AI climbed sharply on April 1, 2026, after the company reported that its 2025 revenue more than doubled, marking a major milestone for one of China’s most watched artificial intelligence firms.

Investors responded with enthusiasm as the stock hit record highs, propelled by strong demand for Zhipu’s AI models and services across enterprise and developer markets. The surge reflects broader interest in AI stocks and highlights how rapid adoption of large language models is reshaping the tech landscape.

Advertisement

With revenue jumping over 130% in 2025, this performance has sparked fresh excitement and debate about how emerging AI leaders are turning cutting‑edge research into commercial growth.

What Drove Zhipu AI’s Share Price Rally After 2025 Results?

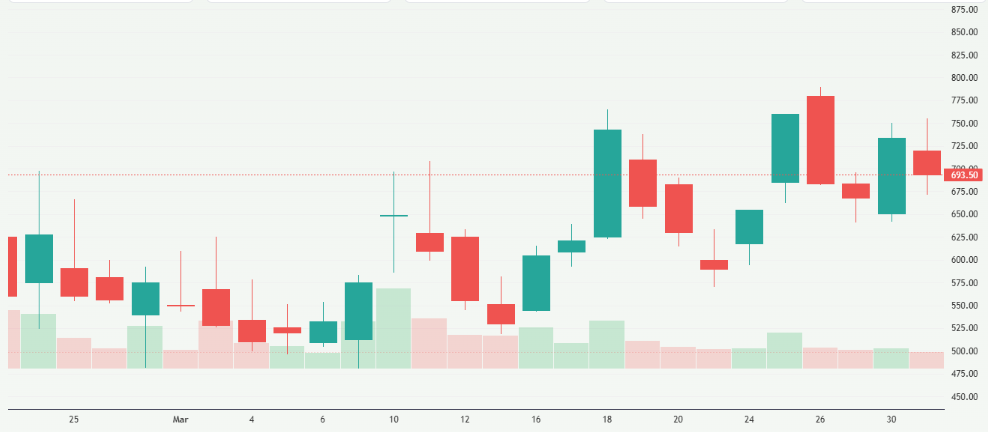

Shares of Zhipu AI (listed as Knowledge Atlas Technology on the Hong Kong Stock Exchange, HK: 2513) surged as much as 35% on April 1, 2026 after the company released its 2025 financial results. Stock gains pushed prices to around HK$938, marking a record high and reflecting strong investor confidence in its business trajectory. This rise also came amid a broader surge in Chinese technology stocks, with the Hang Seng Index climbing alongside Zhipu’s gains.

Why Revenue Growth Mattered?

The biggest driver of the share price jump was Zhipu’s revenue doubling in 2025, with total sales jumping 131.9% year‑over‑year to about ¥724.3 million (≈$105 million). The growth was strongest in its core on‑premise AI deployments, which accounted for roughly 74% of total revenue, and cloud‑based API services, which climbed nearly 300% year‑over‑year.

What Investors are Watching?

Investors cheered the rapid adoption of Zhipu’s GLM models, strong ecosystem integrations with domestic tech firms, and expansion in cloud API usage, a sign of sticky revenue demand. Despite widening net losses, the sales momentum suggested potential future profitability if costs and margins improve.

How Zhipu’s 2025 Financials Actually Look?

Strong Revenue Growth But Losses Remain

Zhipu’s 2025 results, its first full year of reporting post‑IPO, showed convincing top‑line momentum. Full‑year revenue climbed 131.9%, driven by expanding deployment of its AI technology and cloud services. On‑premise revenue grew to roughly ¥533.9 million (~$77.3 million), while cloud API revenue jumped to about ¥190.4 million (~$27.6 million).

However, the company posted a net loss of ¥4.72 billion, significantly wider than the ¥2.96 billion loss in 2024. Its adjusted net loss came in at ¥3.18 billion, reflecting heavy investment in research, model development, and market expansion.

Where Profitability Fits In?

Zhipu says it expects operating improvements and continued revenue expansion to move it toward profitability, though it has not provided a firm timeline. The widening losses underscore the high cost of scaling AI businesses, especially when competing on performance and API demand.

Breakdown of Growth Drivers

- On‑premise deployments remain the largest revenue stream, reflecting strong enterprise uptake.

- Cloud API growth is explosive, indicating broader developer and third‑party integration.

- Pricing adjustments in API services have helped lift usage and overall revenue.

What Strategic Moves are Boosting Zhipu’s Prospects?

Pivot to Domestic AI Chips

Zhipu is accelerating use of China‑made chips to handle demand for compute power. This shift helps cut costs and align with domestic supply‑chain strategies while strengthening performance for its large models, including GLM‑5. Zhipu’s GLM‑5 has reached performance levels comparable to global AI chips through deep optimization on local hardware.

Product and Model Advances

The company continues to push updates to its GLM family of models, including high‑parameter offerings and expanded API capabilities. These upgrades are central to its commercialization path and attract developers and enterprise clients. Growth in API usage, with annual recurring revenue surging many times over, suggests increasing monetization of product usage.

Competition and Market Position

Zhipu operates in a crowded Chinese AI market that includes rivals such as MiniMax, Moonshot AI, ByteDance, and Alibaba. While domestic competition is intense, Zhipu’s IPO, international model access via Z.ai, and expanding user base, in over 200 countries, give it broader exposure.

Zhipu AI Shares: What the Numbers Mean for Investors?

Momentum vs Risk

The dramatic revenue increase in 2025 shows clear demand for AI services and strong execution on sales. But widening net losses highlight that simply growing revenue doesn’t guarantee profit in capital‑intensive AI markets. Analysts are watching whether Zhipu can convert its growth into sustainable earnings.

Price and Usage Trends

Aggressive API pricing increases of over 80% in early 2026 did not slow demand, a positive signal that customers value Zhipu’s capabilities and performance. API usage trends reflect stronger user engagement and willingness to pay for premium services.

Stock and Analyst Views

Some brokerage firms have issued target price boosts and positive commentary based on Zhipu’s revenue performance and API ecosystem expansion. Long‑term investors are focusing on potential operational efficiencies and future profitability as key catalysts.

How Zhipu’s Performance Compares With Broader AI Trends?

China’s AI Sector Expansion

Zhipu’s performance fits into a wider surge in AI development across China. Multiple companies have increased R&D and model launches, contributing to a competitive environment that drives innovation but also margin pressure.

Broader Tech Market Signals

Global investors are watching how AI companies monetize technology. Major firms, including big tech in other regions, have faced market skepticism when growth has failed to produce clear profit paths, while firms with strong recurring revenue models are viewed more favorably.

Analyst Tools and Forecasts

AI stock analysis tools highlight that revenue growth trajectory, API usage trends, and cost control remain core metrics for evaluating companies like Zhipu. Investors need to weigh growth against widening losses when sizing positions.

Wrap Up

Zhipu’s 2025 revenue surge and share price jump highlight its emergence as a key AI player. The strong top‑line performance shows real demand for its models but also underscores the challenge of turning growth into profits. Investors now focus on margin improvements, API monetization, and cost discipline to gauge the stock’s longer‑term direction.

Advertisement

Frequently Asked Questions (FAQs)

Zhipu AI shares jumped 35% on April 1, 2026, after strong revenue growth and high investor confidence in its business.

In 2025, Zhipu AI’s revenue more than doubled, rising about 132% to roughly 724.3 million yuan by year-end.

As of 2025, Zhipu AI is still losing money, with net losses widening to 4.72 billion yuan despite revenue growth.

Disclaimer:

The content shared by Meyka AI PTY LTD is solely for research and informational purposes. Meyka is not a financial advisory service, and the information provided should not be considered investment or trading advice.

Advertisement

What brings you to Meyka?

Pick what interests you most and we will get you started.

I'm here to read news

Find more articles like this one

I'm here to research stocks

Ask our AI about any stock

I'm here to track my Portfolio

Get daily updates and alerts (coming March 2026)