Microsoft just surprised everyone. It reported better-than-expected earnings and shared big plans. The biggest shock? It’s planning to spend over $100 billion on AI and cloud infrastructure this year alone. That’s more than what many countries spend on defense!

Wall Street loved it. Right after the announcement, Microsoft’s stock jumped nearly 8%. Investors saw this as a strong signal that Microsoft isn’t just part of the AI race; it wants to lead it.

We’ve seen AI grow rapidly over the past year. From chatbots to smart tools in Office, AI is already changing how we work. Now, with this new investment, Microsoft aims to develop even more powerful tools and generate significant revenue in the process.

But can the company keep up this momentum? Is the 8% gain just the beginning, or is it too much hype?

Let’s explore the facts, the risks, and what this means for Microsoft and us as users and investors.

The Latest Earnings Beat

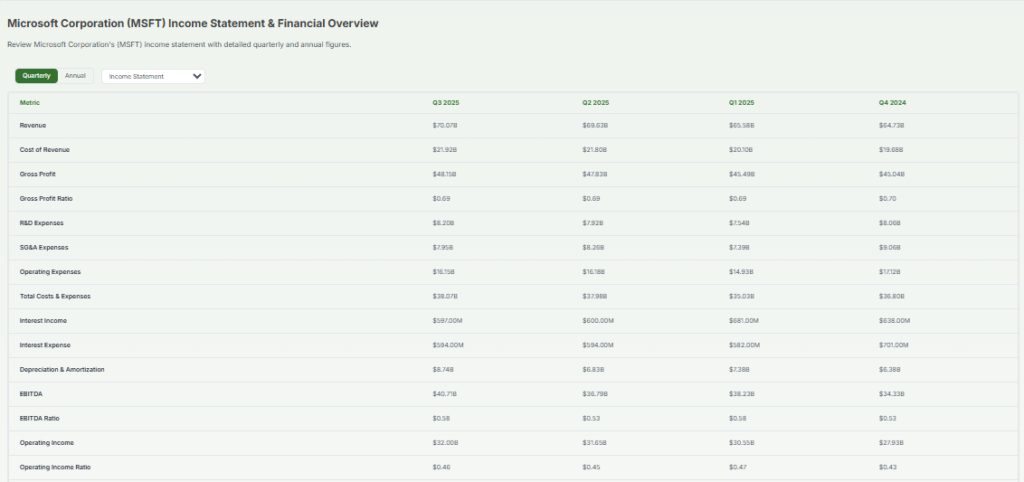

On 30 July 2025, Microsoft released its fiscal Q4 earnings. It reported $76.4 billion in revenue, a rise of 18% year-over-year, and earnings per share of $3.65, beating Wall Street expectations of $3.37 EPS and $73.8 billion in revenue.

Azure and the Intelligent Cloud segment brought in over $75 billion in revenue, growing 34%, well ahead of forecasts.

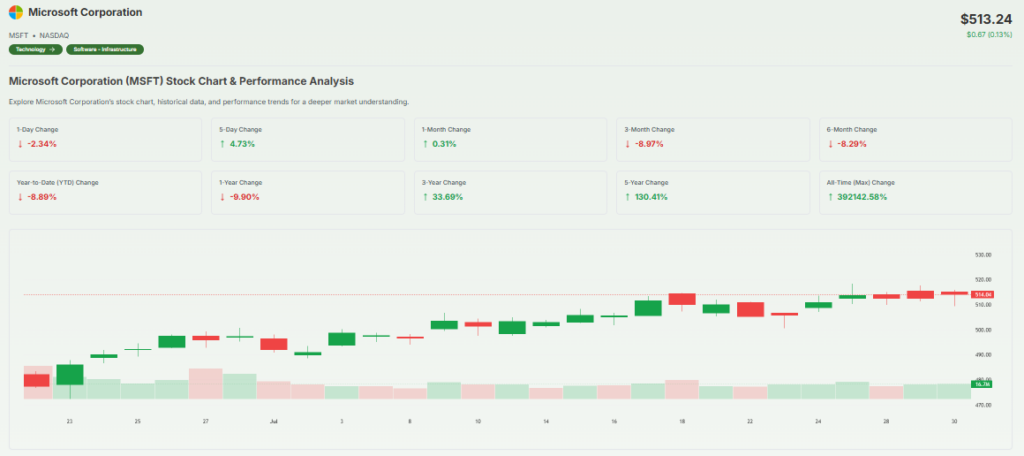

The market responded enthusiastically. Microsoft’s stock surged 7-9% in after-hours trading. This gain pushed the company’s market capitalization close to or above $4 trillion. The shares have risen about 22% so far in 2025.

Wall Street Cheers a $100 B AI Bet

Microsoft has outlined plans to spend more than $100 billion in capital expenditures in the upcoming fiscal year. That figure represents a 14% increase and is mainly aimed at expanding data center capacity and hiring AI talent.

This massive investment aims to power its AI tools like Microsoft 365 Copilot and support huge workloads via Azure. Analysts see this bold move as a signal that Microsoft wants to lead the AI-era competition against peers like Amazon and Alphabet.

What is Pushing the Stock Up?

Azure and AI Power Demand

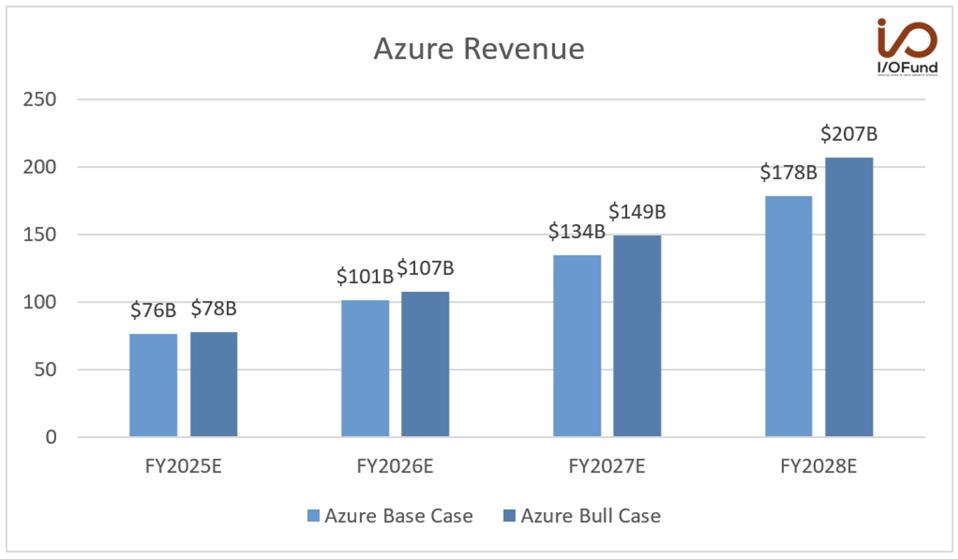

AI features in tools like Copilot and GitHub Copilot are helping drive enterprise AI adoption. Azure’s revenue grew 34-39%, far ahead of many expectations. Analysts forecast continued high Azure growth up to 29% annually in the coming years, highlighting its role in Microsoft’s strategy.

Analyst Optimism

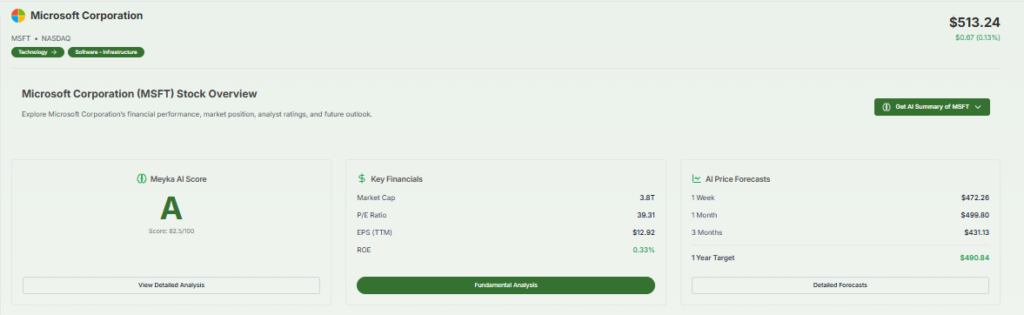

Every one of 19-20 analysts tracked by Visible Alpha rates Microsoft a Buy or equivalent. The average price target of $580 to $600 suggests potential upside of about 12-20% from recent trading levels.

Oppenheimer, Wedbush, Citi, and Jefferies all highlight Microsoft’s pricing power, strong margins, and deep AI offerings as reasons for their bullish ratings.

Internal AI Efficiency Gains

Executives say Microsoft is using AI to boost internal operations. One presentation cited over $500 million in savings in call centers and noted that AI generated about 35% of the code for new products in 2024. These internal improvements reinforce confidence that Microsoft can monetize AI at scale.

Will the 8% Gain Stick?

Capex Payoff Questions

Spending over $100 billion on exploding AI growth. Some analysts worry the return on that capital may take time to materialize. AI infrastructure often requires a huge upfront cost before revenue comes in.

Increasing Competition and Talent Pressure

New rivals like DeepSeek in China aim to challenge big players with cheaper models. Meanwhile, top AI engineers now command multimillion-dollar offers across the industry, a strain on Microsoft’s margins.

Normalizing Capex Growth

While capex is expected to hit about $30 billion in Q1 FY2026, CFO Amy Hood has warned that growth in AI infrastructure spending will likely slow in the latter half of fiscal 2026.

Macro and Regulatory Risks

Wider economic pressures like interest rates and regulation could affect growth. Microsoft is also under scrutiny from regulators over its AI deals and market power, especially given its OpenAI partnership.

Long‑Term View: Beyond Today’s Pop

Microsoft has guided for double‑digit revenue and income growth in FY2026, even as capital expansion moderates. Analysts suggest a clear path to a $4-5 trillion market cap over the next 18 months if AI revenue holds pace.

The partnership with OpenAI remains central. Microsoft still shares revenue with OpenAI, and any structural changes like acquiring a stake or renegotiating terms could lift earnings more meaningfully by 2030. AI-based revenue is expected to represent a significant portion of cloud business by 2030, with Azure possibly generating 64% of total company revenue.

Final Verdict

We believe the nearly 8% stock jump after Microsoft’s Q4 2025 announcement is not just hype. Strong earnings, aggressive AI investment, and solid analyst momentum back that move. Yet, sustaining that gain will depend on translating huge capex into profits. Execution risk remains with competition rising and regulatory oversight tightening.

In the coming years, Microsoft’s lead in AI infrastructure, enterprise software, and energy-efficient data centers may deliver strong returns if it can show tangible ROI. We’ll need to watch Azure growth, capex trends, and how Microsoft handles competition and regulation.

Frequently Asked Questions (FAQs)

As of July 31, 2025, Microsoft plans to spend over $100 billion on AI and cloud this year. Most of it will go toward data centers and smart tools.

Many investors think Microsoft is a strong AI stock. It has smart tools like Copilot and big cloud services. But, like all stocks, there are risks too.

No, Microsoft does not own 50% of OpenAI. It has invested billions in the company, but OpenAI stays independent. Microsoft shares profits from some AI tools instead.

Yes, Microsoft earns money by offering OpenAI’s models through Azure. It also uses OpenAI in products like Copilot. The company gets a share of revenue from these tools.

Disclaimer:

This is for information only, not financial advice. Always do your research.

What brings you to Meyka?

Pick what interests you most and we will get you started.

I'm here to read news

Find more articles like this one

I'm here to research stocks

Ask our AI about any stock

I'm here to track my Portfolio

Get daily updates and alerts (coming March 2026)