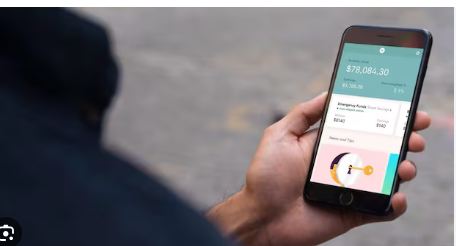

In Canada, the Big Five banks control most of the money we spend, save, and borrow. They’ve been around for over 100 years, and they’ve set the rules for how banking works. But things are starting to change. Wealthsimple Credit Card launched, a Canadian financial tech company known for its easy investing app. It’s not just about helping us invest anymore; it wants to become our all-in-one money manager. The company is now launching a new credit card and preparing to roll out a line of credit.

These tools are designed to be simple, smart, and built around how we actually live. There are no hidden fees, no complicated reward systems, and no need to visit a bank branch. Everything works right from our phones.

This move puts Wealthsimple in direct competition with Canada’s biggest banks. But can a digital-first company really challenge the old-school banking giants?

Let’s explore how Wealthsimple’s new credit card and borrowing features work, what makes them different, and why they might be a real game-changer for the way we manage our money.

Canada’s Big-Bank Shake-Up: Wealthsimple Launches Credit Card & Instant Line of Credit

Canada’s big banks have dominated for decades. They set the rules on spending, saving, and borrowing, often charging fees we accept as normal. But now, a digital challenger is here.

Wealthsimple, known for easy-to-use investing, is launching its credit card. It’s also preparing to roll out an instant asset-backed line of credit by the end of 2025. We think this could change the game.

2% Cash Back and No FX Fees

Wealthsimple’s credit card offers unlimited 2% cash back on every purchase, no categories, no spending caps. It also removes foreign transaction fees, which usually tack on around 2.5% when we spend outside Canada. For many of us, that means more reward on every purchase.

No Annual Fee For Many

If we’ve got $100,000 or more with Wealthsimple, or we deposit $4,000+ monthly, the card has no annual fee. Others pay just $10 a month. No hidden costs, no surprises, just clear, fair pricing.

A Metal Card for Premium Users

Premium clients get a metal credit card that feels sturdy and sleek. Wealthsimple lets us lock our card, change our PIN, and use tap-to-pay without limits, especially on virtual cards. That level of control is a big plus.

Instant Line of Credit: Borrow Smartly

By the end of 2025, we’ll be able to borrow instantly against our Wealthsimple account balances. The line of credit is expected to start at just 4.45% interest, a far cry from typical credit card rates (20-24%) or HELOCs (5.5–5.7%). It’s fast, secure, and easy no branch visits or piles of paperwork.

Built-In Chequing Account: Top-Tier Perks

Wealthsimple also upgraded its chequing account formerly “Cash”, into a full-featured Chequing product.

- Interest up to 2.75% for high-balance accounts.

- 1% cash back on every debit purchase.

- No monthly fees, ATM fees, or FX charges.

- Early paycheque deposits, up to one day early.

- Up to $1 million CDIC insurance by spreading deposits across partner banks.

- New features: mobile cheque deposit, digital cheque acceptance, and even cash/cheque delivery, starting in Toronto.

We practice everything from spending to saving on one app, and that matters.

What This Means for Users

We think these products speak to how we want to manage money today. We get higher rates, more rewards, and fewer fees, all on our phones. The reason is that we don’t lose time standing in line or hiding in menus.

The instant line of credit helps during emergencies or big purchases, without needing home equity or a big credit check. We just tap our balance.

Plus, digital “trust features” like trusted locations, customizable transaction limits, and verified contacts make us feel safer.

Wealthsimple vs Big Banks

Wealthsimple isn’t a bank, but it is issuing its credit card. That’s a first for a non-bank fintech in Canada. It also underwrites its loans, and partner banks hold deposits behind the scenes.

This gives them low overhead, and no branches means lower costs. Wealthsimple uses banking to boost its investing business. They expect we’ll invest more if we keep more money in their ecosystem.

In Canada, the Big Six still hold over 90% of assets. But surveys show 38% of us are unhappy, and 25% considered switching banks. Wealthsimple sees opportunity.

Community Buzz

On Reddit, users are hyped:

Still, some wonder if features like trusted places or digital cheques are useful. Others miss brick-and-mortar support. But most agree this is a serious digital shake-up.

What’s Ahead

Wealthsimple plans to keep building. They’re exploring mortgages with Pine, deeper trading tools, new private market & crypto offerings, and even more branchless services like cheque and cash delivery. Rumors of an IPO grow louder once their full financial stack proves scalable.

The Final Word

The Wealthsimple credit card and line of credit mark a bold step toward challenging Canada’s major banks. Everything is digital, transparent, and designed around our lives. We might borrow, spend, save, and invest all in one clean app.

The real challenge will be earning people’s trust, following all rules, and seeing if users are willing to make the switch. If they succeed, Wealthsimple could rewrite how Canadians handle money, without a single bank branch needed.

Frequently Asked Questions (FAQs)

Wealthsimple is not a bank, but it works with banks like Canadian ShareOwner and Peoples Trust. These partner banks help hold and protect customer money in the background.

You can use Wealthsimple like a bank for spending, saving, and getting paid. But it isn’t a real bank and doesn’t have physical branches or full banking services.

Yes, it can affect your credit score if you use its credit card or borrow money. Like other lenders, Wealthsimple may report your credit use to credit agencies.

A line of credit lets you borrow money when needed, up to a limit. Cash credit is usually for businesses and is based on their inventory or sales records.

Disclaimer:

This content is made for learning only. It is not meant to give financial advice. Always check the facts yourself. Financial decisions need detailed research.

What brings you to Meyka?

Pick what interests you most and we will get you started.

I'm here to read news

Find more articles like this one

I'm here to research stocks

Ask our AI about any stock

I'm here to track my Portfolio

Get daily updates and alerts (coming March 2026)