Verisk Analytics is a big name in the data world. It helps companies manage risk using smart data tools. In the past year, its stock price has climbed fast. Many investors got excited and rushed in. But now, there’s a twist.

A major analyst just downgraded the stock. Why? They believe it’s too expensive right now. Verisk may still be a strong company, but the price tag seems too high. This change is making some investors nervous.

As we look closer, we’ll explore why the downgrade happened. We’ll also check if Verisk is still a good choice for the long run. Let’s break down the facts and find out what’s really going on with this stock.

About Verisk Analytics

Verisk Analytics is a U.S.-based data analytics company. It started in 1971 and became a public company in 2009. Verisk serves businesses in insurance, energy, and financial services. It helps them manage risk using deep data tools.

Verisk is best known for its work in insurance analytics. It collects and analyzes millions of data points to help insurers set prices and predict risks. Over time, it added services for climate risk, fraud detection, and even energy market forecasts.

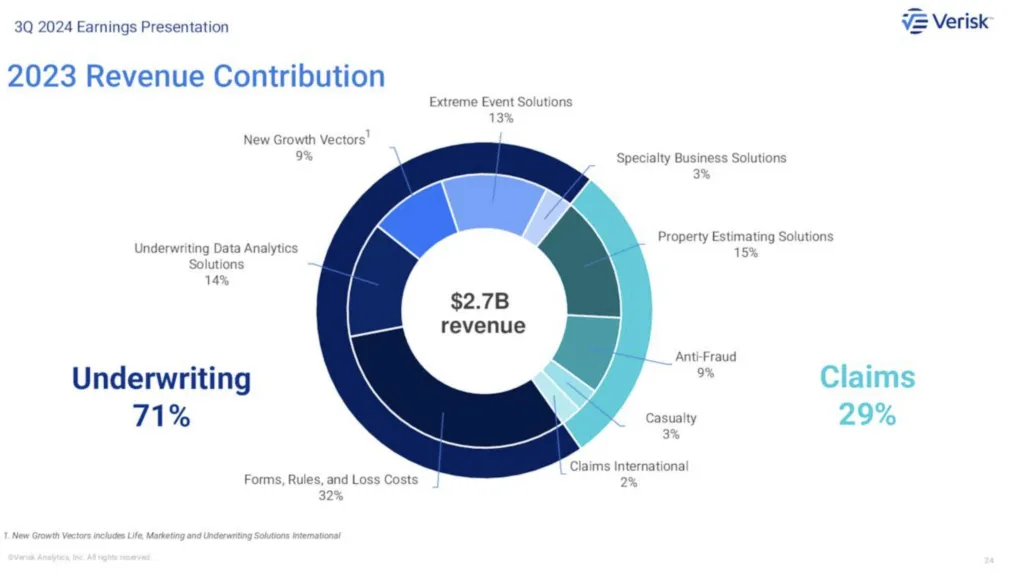

In 2024, Verisk sold its financial services unit to focus more on insurance. This helped improve margins. Its revenue reached over $2.7 billion in 2023, with a solid profit margin of around 32%.

Recent Stock Performance

In the last 12 months, Verisk’s stock climbed nearly 25%. This outpaced the S&P 500, which grew around 15% in the same time. The stock hit a high of over $250 in early 2025, showing strong investor confidence.

Why the excitement? A few reasons.

- First, Verisk’s focus on core insurance analytics paid off.

- Second, the company started using AI to boost its data tools.

- Third, it reported better-than-expected earnings for multiple quarters.

Investors believed Verisk was now leaner, more focused, and future-ready. That’s why many jumped in. But now, some experts feel the stock may have gone too far, too fast.

The Analyst Downgrade

In April 2025, Baird downgraded Verisk from Outperform to Neutral. The main concern? High valuation.

The analyst said Verisk’s stock price already reflects most of the good news. With the stock trading at high multiples, there’s limited room for upside. In short, the price may be too high for the earnings it brings in.

They also raised concerns about slowing growth. While AI and core insurance tools are solid, future expansion could be slower. Verisk sold non-core units, so it now has fewer areas to grow.

After the downgrade, Verisk’s stock fell about 2% in a single day.

Trading volume also increased, showing that many investors were reacting fast to the news.

Valuation Metrics Breakdown

As of May 2025, Verisk trades at a price-to-earnings (P/E) ratio of around 42, which is much higher than the industry average of 25. Its EV/EBITDA ratio is over 28, again higher than competitors like CoreLogic or Fair Isaac Corp.

These high numbers tell us that the stock is priced for perfection. Even a small earnings miss could hurt the price. Analysts at Baird and JPMorgan have both called this level of valuation “stretched.”

Despite reporting strong earnings in Q1 2025, including 10% revenue growth, the company’s guidance was flat for the next quarter. This made some investors nervous. The big question now is: Can future earnings support this stock price?

Growth vs. Valuation Debate

There’s a clear split in views. Supporters say Verisk is a top-tier data company. Its deep roots in insurance analytics, use of AI, and strong profits mean it will do well long term.

Critics, though, point to the price. They argue that the stock has already priced in years of growth. One analyst said, “It’s a great company, but not at any price.”

So, is Verisk a growth gem or a value trap? That depends on whether it can surprise investors with new wins like better AI tools, new markets, or big deals. We think it’s smart to keep both views in mind before making any decision.

What Investors Should Watch

If you’re tracking Verisk, here are key things to keep an eye on:

- AI developments: New features that improve their risk tools.

- Partnerships: Deals with insurance firms or AI tech companies.

- Earnings reports: Especially if they beat expectations.

- Regulation: Rules around data privacy could impact operations.

- Market response: Is the hype fading or still strong?

The next earnings call will be in July 2025. That could shift investor mood depending on the results and guidance.

Wrap Up

Verisk is a strong company with great tools and profits. But its stock price may be running ahead of reality. The recent downgrade is a red flag, not a red light.

As investors, we need to stay smart. Watch how the company performs, how the market reacts, and if growth can catch up to the high price.

Frequently Asked Questions (FAQs)

As of early 2025, Verisk has a market value of around $40 billion. This is based on its stock price and the number of shares in the market.

Verisk has over 7,000 employees and makes more than $2.7 billion each year. It serves clients in over 30 countries, mostly in the insurance and risk fields.

Verisk helps companies understand risk using smart data tools. It works mostly with insurance, helping them price plans, detect fraud, and manage disasters using data.

Verisk was criticized in past years for handling personal data. Some groups raised concerns about data privacy and how the company collects and shares customer information.

Disclaimer:

This content is for informational purposes only and not financial advice. Always conduct your research.

What brings you to Meyka?

Pick what interests you most and we will get you started.

I'm here to read news

Find more articles like this one

I'm here to research stocks

Ask our AI about any stock

I'm here to track my Portfolio

Get daily updates and alerts (coming March 2026)