UnitedHealth Group (UNH) has long been one of the most stable and trusted names in the U.S. healthcare industry. It manages millions of members, offers a wide range of insurance plans, and operates major health services through its Optum division. Yet, in 2024, we saw something unexpected: UNH stock suffered its steepest drop since the 2008 financial crisis. For a company known for steady growth, this decline was a shock to both investors and the healthcare sector.

Why did this happen? Rising medical costs, tighter regulations, and weaker-than-expected earnings all played a role. Market volatility and investor fears only made things worse. Now, as we step into 2025, the big question is clear: can UNH bounce back?

Advertisement

Let’s find out the reasons behind the UNH stock fall, the challenges ahead, and the opportunities that might help the company recover. Let’s break it down step by step, so we can see the bigger picture and make sense of where UNH is heading next.

UNH Stock: The Steep Decline

UnitedHealth’s slide in 2025 shocked the market. The UNH stock fell more than 22% on April 17 after the company missed earnings and cut its outlook, its steepest one-day drop since the late 1990s. The miss was the first since 2008. Management blamed higher-than-expected medical costs and softer results at Optum, the services engine that usually smooths earnings. Investors quickly priced in a slower profit path for the rest of the year.

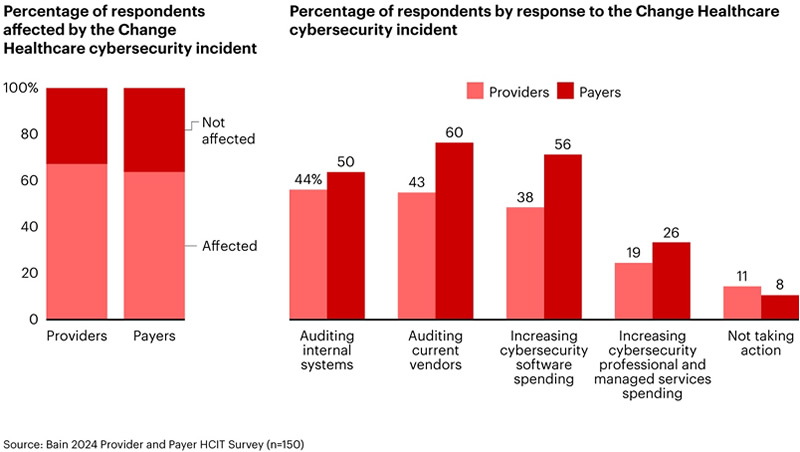

Pressure didn’t end there. A ransomware attack at Change Healthcare in 2024 kept costing more through 2025, complicating claims flows and adding security and remediation expenses. Government data now shows the breach affected about 192.7 million people, making it the largest healthcare data incident on record. That scale raised compliance and legal risks and forced more investment into cybersecurity.

Leadership turmoil added to nerves. In May 2025, CEO Andrew Witty stepped down abruptly; former CEO and current chair Stephen Hemsley returned to the role. Big changes at the top often keep investors cautious until a new plan is clear.

Broader Market and Sector Context

Managed-care peers also felt the heat as medical use spiked among old, especially for outpatient and physician services. Sector selling was sharp on April 17, but most rivals rebounded faster than UnitedHealth, signaling company-specific issues layered on top of industry trends. Elevated utilization and funding headwinds hurt 2025 profits across Medicare Advantage.

Policy also mattered. The Centers for Medicare & Medicaid Services set 2025 Medicare Advantage rates that implied modest revenue growth and continued phase-ins of prior policy changes. Plans faced tighter economics while costs climbed. That combination pressured margins across the industry.

Financial Performance Analysis

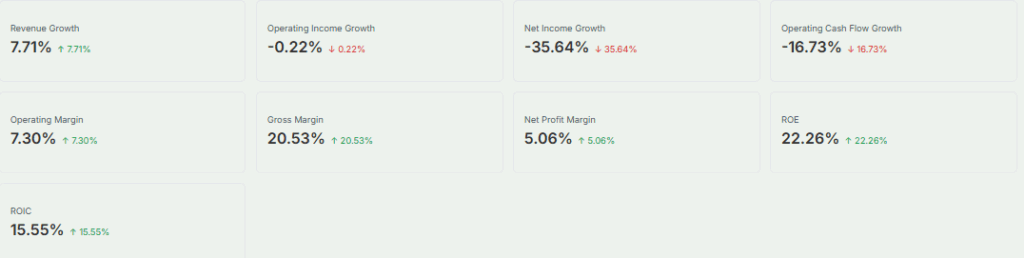

UnitedHealth’s Q1 2025 revenue was $109.6 billion, up year over year but below expectations. Adjusted EPS of $7.20 missed the Street. Management cut full-year adjusted EPS guidance to $26.00-$26.50 and later re-established a lower outlook after suspending it during the spring turmoil. The company cited elevated medical costs and lower-than-planned Optum profit.

Q2 2025 results stayed soft. Adjusted EPS of $4.08 missed consensus; the medical loss ratio remained high, reflecting the same cost pressure theme. Operating margin at UnitedHealthcare dropped to 2.4% from 5.4% a year earlier. These numbers illustrate how quickly utilization and reimbursement dynamics can hit earnings for even the scale leader.

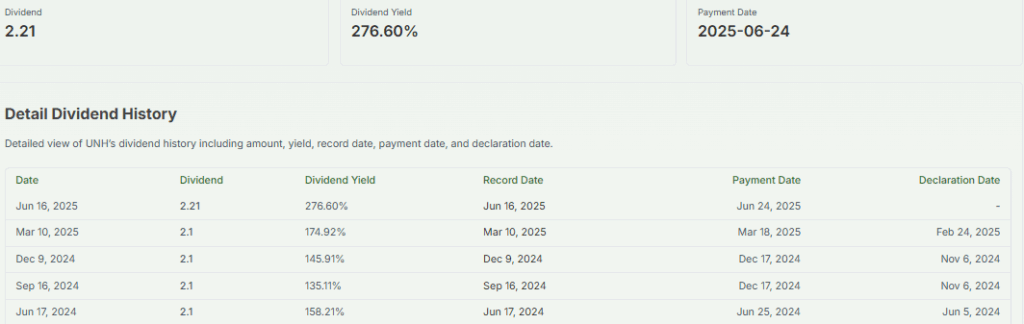

Even so, the balance sheet and cash generation support ongoing dividends. In August 2025, the board authorized a $2.21 quarterly dividend, continuing a long record of increases. Dividend coverage remains a focus point for investors looking for signs of stability.

UNH Stock: Key Challenges Ahead

Regulatory risk remains central. Medicare Advantage payment updates for 2025 were measured, while prior risk-adjustment changes are still phasing through. That means less room for margin error if medical use stays high. Ongoing Justice Department scrutiny of practices around Medicare Advantage adds legal and reputational risk that can overhang valuation.

Operational costs are running hot. Higher outpatient and physician visits, plus catch-up care by older, lift claims quickly. The cyberattack fallout still demands investment in technology, security, and provider advances. Each dollar spent here is vital, yet it weighs on near-term profit.

Finally, leadership change introduces execution risk. A credible, detailed recovery plan must show how Optum, UnitedHealthcare, and technology platforms re-sync to deliver predictable earnings.

Recovery Catalysts for 2025

Several levers could aid a rebound. First, stabilization in utilization trends would lower the medical loss ratio and restore margin visibility. Management has already reset guidance, which can reduce the risk of more negative surprises if costs moderate.

Second, Optum’s scale in pharmacy benefits, care delivery, and analytics still offers long-term growth. Fixes inside Optum product upgrades, leadership stability, and better integration with payor operations could rebuild confidence. Company commentary points to under-investment areas now getting attention

Third, continued dividend payments signal balance-sheet strength. A steady or rising payout can support total return while investors wait for earnings to recover.

Finally, influential buyers can help sentiment. Berkshire Hathaway’s newly disclosed 5-million-share stake sparked a positive reaction, highlighting conviction from a marquee long-term investor. Large, patient capital can create a floor in turbulent periods.

Analyst Predictions and Investor Sentiment

By mid-2025, several research shops reduced targets and shifted tones from confident to cautious. The April selloff blindsided Wall Street, given UnitedHealth’s long record of “beat and raise.” Some analysts still see long-term value once the utilization spike normalizes, but most want proof through two or more clean quarters. Sentiment remained fragile through July as guidance stayed below earlier hopes.

Retail investors are split. Income-seekers point to the dividend and franchise quality. Traders focus on headline risk around costs, policy, cyber, and leadership. That push-pull explains the sharp moves around earnings days and filings.

Risk vs. Reward for Investors

Near-term risk is clear: elevated medical costs, regulatory friction, cyber remediation, and leadership transition. Another guidance cut or operational stumble could drag shares lower. On the other hand, stabilization in utilization, smoother Optum execution, and consistent dividends create upside optionality from depressed levels. Long-horizon holders who can accept volatility may find improving risk-reward if the company stacks a few solid quarters together.

Bottom Line

UnitedHealth’s 2025 story is about resetting and rebuilding. The franchise still spans insurance, pharmacy, data, and care delivery at an unmatched scale, but recent shocks exposed weak points. The path to recovery runs through cost control, Optum fixes, steady policy navigation, and regained credibility with the Street. Proof will come in the numbers quarter by quarter.

For now, the dividend, a new long-term shareholder in Berkshire, and a lower bar on guidance offer early support while the company works back to form.

Advertisement

Frequently Asked Questions (FAQs)

It is hard to say now. UnitedHealth may recover if costs ease, earnings improve, and guidance stays steady. But many risks remain as of August 15, 2025.

Maybe. If its business gets back on track, Optum does better, and medical costs calm down, UnitedHealth could bounce back. Yet risks still exist today, August 15, 2025.

It might. If earnings improve and investor confidence returns, the stock could rise. But it depends on the results and news after August 15, 2025. Many unknowns remain.

Disclaimer:

This is for informational purposes only and does not constitute financial advice. Always do your research.

Advertisement

What brings you to Meyka?

Pick what interests you most and we will get you started.

I'm here to read news

Find more articles like this one

I'm here to research stocks

Ask Meyka Analyst about any stock

I'm here to track my Portfolio

Get daily updates and alerts (coming March 2026)