Shares of Trevi Finanziaria Industriale took markets by surprise on March 30, 2026, plunging about 37% in a single session after the company unveiled a €100 million rights issue. The sharp drop shocked investors because Trevi also reported record order volumes for fiscal 2025, with new contracts and a robust project backlog driving optimism about its long‑term business.

But the capital raise and debt restructuring plans overshadowed good news, sparking a sell‑off. This clash between strong operational performance and financial concerns has ignited debate among market watchers. Is this a short‑term reaction or a deeper signal for industrial stocks? Read on to understand the details shaping Trevi’s stock story.

Share Price Shock: Why Trevi Fell 37%?

On March 30, 2026, shares of Trevi Finanziaria Industriale plunged about 37% after the company announced a €100 million rights issue and a larger debt refinancing deal. Investors reacted strongly to the financing move, which they saw as dilutive and risky, despite strong earnings and backlog growth. The Italian engineering group’s market value took a hit, overshadowing the positive performance in its core operations.

The capital raise is part of a multi‑pronged financial strategy aimed at improving the balance sheet, including a new €170 million amortizing loan and a 1‑for‑20 reverse share split approved by the board.

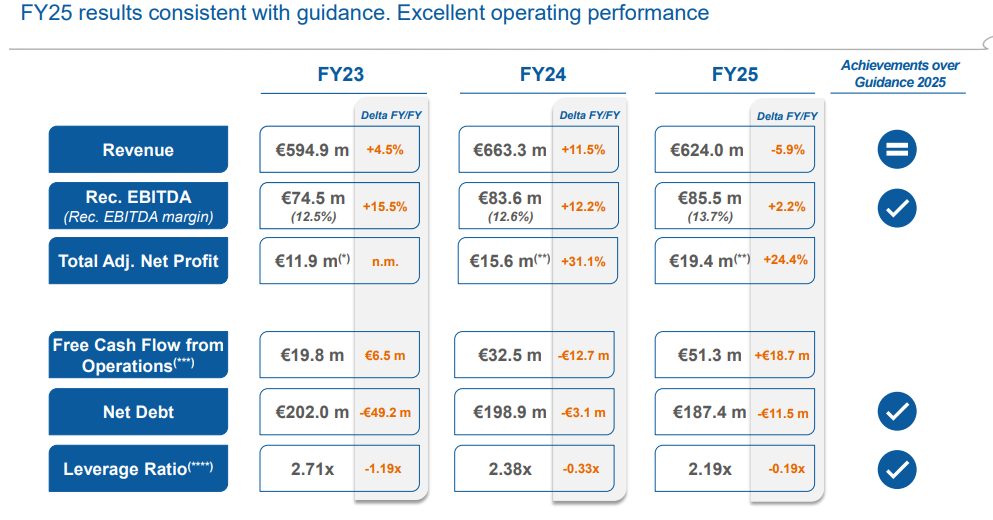

Record Orders and Profit Growth in FY25

Trevi posted record order intake in fiscal year 2025, with €734.3 million in orders, up 21% from the prior year. This strong commercial performance extended into early 2026 with major contracts, such as infrastructure projects in New York and the UAE, pushing the total backlog to about €837 million by late February 2026.

The company also reported a net profit increase to around €8.1-€8.6 million for FY25, compared with roughly €1.5 million the year before. Recurring EBITDA rose to approximately €85.5 million, with margins expanding to 13.7%.

Despite this operational strength, markets focused on the dilutive rights issue and adjusted near‑term outlook, which weighed on share price performance.

What Strategic Shift Did Trevi Announce?

Four‑Part Financial Plan Explained

Trevi’s strategy covers four main elements:

- A €170 million five‑year amortizing loan to refinance part of existing debt, including a mature bond due in 2026.

- A €100 million rights issue to reinforce the capital base and support growth initiatives.

- A 1-for-20 reverse split to support the capital raise and improve share liquidity.

- Short‑ and long‑term financing lines to bolster working capital and competitive bidding capacity.

The board sees this move as essential to boost financial flexibility and execute the 2026-2029 business plan, which targets revenue growth and reduced net financial debt.

How Has CDP Equity Responded?

State‑backed investor CDP Equity, holding about 21.3% of Trevi, has committed to subscribing to its portion of the rights issue. This shows long‑term support from a strategic shareholder.

Stock Forecast and Analyst Views

Current Technical and Consensus Outlook

- Trevi’s shares trade on the Milan Stock Exchange under ticker TFIN.MI, with current prices around €0.46-€0.48. Technical indicators suggest a near‑term sell signal based on moving averages.

- Analyst consensus remains mixed to neutral. One analyst target puts the 12‑month price target near €0.44, about slightly below current levels.

- According to other market data, Trevi is forecast to post earnings growth of about 13% per year, though revenue growth is seen as modest.

These mixed estimates reflect uncertainty created by near‑term financial moves, even though operational fundamentals show improvement.

Growth vs Risk to Investors

Some market models highlight Trevi’s potential for future earnings growth, while others flag volatility and financial position as key risks. These views are common in technical and fundamental analyses and should be reviewed carefully, including using an AI stock analysis tool for deeper pattern recognition before making decisions.

What’s Next for Trevi’s Business and Shares?

Guidance for 2026

The company’s outlook points to revenue of €640-€670 million for 2026 with recurring EBITDA of €70-€80 million, slightly below FY25 levels. This reflects a change in geographic project mix and the timing of work on larger contracts.

Longer‑Term Strategic Goals

Trevi’s 2026-2029 plan aims to:

- Grow revenues with a compound annual growth rate of roughly 5.5%.

- Reduce net financial debt toward near zero by the plan’s end.

- Strengthen competitive position in underground engineering and foundation services.

Final Words

Trevi’s 37% share slide highlights how markets penalize perceived financial risk even when a business posts strong project wins and profit gains. The rights issue and refinancing strategy aim to stabilize and support long‑term plans, but investor confidence remains cautious as short‑term earnings expectations moderate. Monitoring the execution of debt restructuring and backlog conversion will be key to assessing future stock performance.

Disclaimer:

The content shared by Meyka AI PTY LTD is solely for research and informational purposes. Meyka is not a financial advisory service, and the information provided should not be considered investment or trading advice.

What brings you to Meyka?

Pick what interests you most and we will get you started.

I'm here to read news

Find more articles like this one

I'm here to research stocks

Ask our AI about any stock

I'm here to track my Portfolio

Get daily updates and alerts (coming March 2026)