Tata Power’s latest financials have turned heads this February. On 4‑5 February 2026, the Indian energy giant reported a 25% drop in net profit for the October–December quarter of FY26, with earnings slipping to around ₹772 crore from over ₹1,030 crore a year ago. At the same time, revenue from operations fell roughly 9%, highlighting pressure on core sales.

This wasn’t just a minor dip. It reflects deeper shifts in the power sector, from weak thermal generation to rising renewables, and has sparked fresh debate among investors and analysts alike. Stay with us to unpack what’s behind these numbers and what it means for Tata Power’s growth path in 2026 and beyond.

Tata Power Q3 FY26 Financial Highlights and Market Reaction

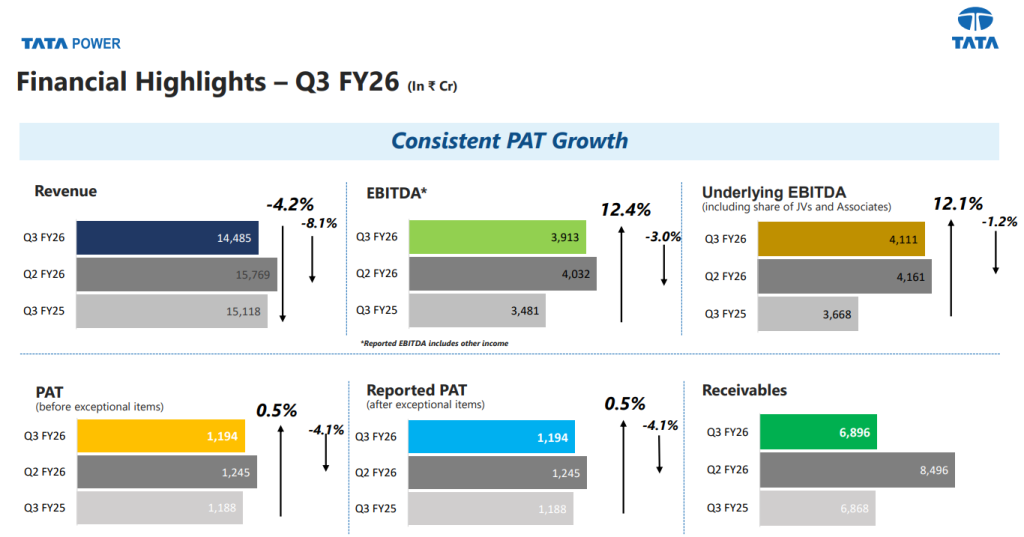

Tata Power’s third quarter (Q3 FY26) performance delivered mixed results that surprised investors and analysts when figures were released in early February 2026. The company reported a year‑on‑year net profit decline of approximately 25%, with profit falling to around ₹772 crore for the quarter ended December 31, 2025. This was down from about ₹1,030.7 crore in the same quarter of FY25, reflecting significant earnings pressure.

Revenue from operations also dropped by roughly 9.4% to ₹13,948 crore compared with ₹15,391 crore in Q3 FY25. EBITDA declined nearly 9% to around ₹3,055 crore, although margins remained relatively stable around 21.9%.

Investors reacted to the earnings miss by trimming the stock, with Tata Power shares sliding around 2% on weak revenue trends and bottom‑line contraction despite some operational strengths.

Segment Performance: What Drove the Numbers

Why Did the Earnings Slide?

The earnings slide in Q3 was driven largely by challenges in traditional generation assets. The Mundra Ultra Mega Power Plant in Gujarat remained largely non‑operational in Q3 due to technical and contractual factors, hurting thermal power sales; the segment saw steep declines.

In contrast, Tata Power’s renewable energy and transmission segments showed growth. The company reported strong execution in renewable projects and increased contributions from distribution and solar businesses, indicating diversification benefits.

How Did Renewables and Other Segments Perform?

Tata Power’s clean energy business delivered notable growth in Q3 FY26:

- Renewable energy business PAT surged 156%, while revenue jumped 78%, indicating robust performance in solar and wind segments.

- Solar cell and module manufacturing saw strong output and profit growth, reflecting Tata Power’s deeper involvement in the solar value chain.

- Distribution business, including operations in Odisha and Delhi, posted significant profit growth compared to the year‑ago period.

- The transmission business also recorded an 80% YoY PAT increase.

This pattern shows that while legacy thermal assets struggle, clean energy and infrastructure units are driving future growth.

Broader Power Sector Context and Demand Trends

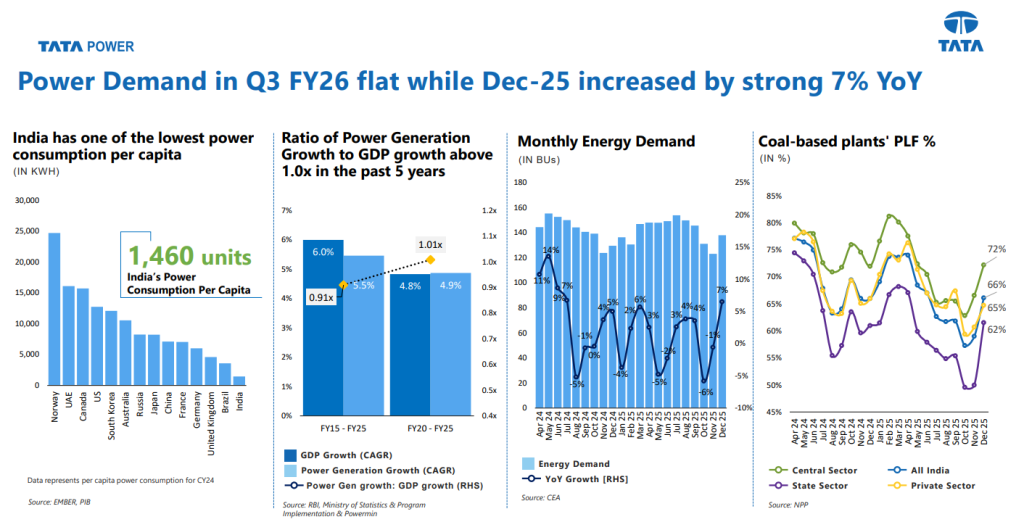

Tata Power’s results must also be seen in the context of wider sector dynamics in India. Overall power demand in the country fell marginally (≈0.4%) in the quarter, affected by unseasonal weather and cooler temperatures, according to market analysts. Coal‑fired generation also declined sharply, compounding challenges for thermal power operators.

However, utility scale renewables and power distribution segments continue to see strong demand as India pushes for energy transition and grid expansion, trends that favor companies investing in green energy infrastructure.

Tata Power Stock and Future Outlook

Tata Power Stock Snapshot and Forecast

According to data sourced from Meyka’s AI‑driven stock news aggregator and market trackers, The Tata Power Company Limited (TATAPOWER.BO) remains actively traded with updates and sentiments affecting price movements throughout 2026. The real‑time feed shows fluctuations that reflect market responses to earnings and sector changes.

Here’s a broader stock forecast and outlook from market sources:

- Analysts’ average 12‑month price target for Tata Power ranges between roughly ₹405-₹420, with upside potential if execution improves. Estimated targets reach above ₹500 at the higher end, while downside scenarios put targets near ₹285.

- Independent models suggest the company can grow earnings by ~14% annually and revenue by ~8% in coming years, driven by renewables and grid businesses.

These forecasts reflect cautious optimism, acknowledging sector transition but soft demand in conventional power segments.

What Do Analysts Say on Tata Power Performance?

Market expert models such as those from MarketsMojo point to financial challenges, including higher leverage, weak return ratios, and margin pressures, that may weigh on valuations if not addressed. However, successful execution in clean energy projects and improved EBITDA trends could strengthen confidence.

Some brokerages have retained “buy” or “hold” stances, noting that short‑term issues like thermal plant shutdowns and one‑time expenses are not indicative of long‑term growth potential when balanced against strong renewable execution.

What’s Next: Tata Power Strategy and Growth Drivers

Tata Power’s leadership continues to push strategic initiatives that extend beyond conventional generation. CEO Praveer Sinha has highlighted plans to explore small modular nuclear reactors (SMRs) and expand capacity across renewable and storage technologies once regulatory clarity emerges, aligning with India’s broader energy goals.

Additionally, ambitious capex plans up to ₹1.25 trillion through FY30 aim to scale capacity to 30 GW, with an emphasis on clean energy sources. This long‑term strategy underscores Tata Power’s shift toward a diversified, future‑ready portfolio.

Conclusion: Mixed Results but Long‑Term Opportunities

Tata Power’s Q3 FY26 shows mixed results. Profit and revenue fell due to thermal challenges, while renewables and distribution grew. Analysts see moderate upside if clean energy and diversification plans succeed.

Frequently Asked Questions (FAQs)

Tata Power’s profit fell about 25% in Q3 FY26 (Dec 2025) mainly due to weak thermal power sales and higher operating costs. Renewable segments grew but could not fully offset losses.

Revenue declined nearly 9% to ₹13,948 crore in Q3 FY26 (Dec 2025). Renewable energy, solar, and transmission segments grew, while traditional thermal power sales dropped sharply.

The results show short-term pressure on Tata Power’s stock due to profit and revenue decline. Analysts expect moderate growth if renewable and distribution segments perform well.

Disclaimer:

The content shared by Meyka AI PTY LTD is solely for research and informational purposes. Meyka is not a financial advisory service, and the information provided should not be considered investment or trading advice.

What brings you to Meyka?

Pick what interests you most and we will get you started.

I'm here to read news

Find more articles like this one

I'm here to research stocks

Ask our AI about any stock

I'm here to track my Portfolio

Get daily updates and alerts (coming March 2026)