Fast Retailing, the company behind Uniqlo, just made a bold move. It decided to stick with its full-year profit forecast, even as global trade problems continue. Many companies are struggling with rising costs due to tariffs and inflation. But Fast Retailing seems ready to face these issues head-on.

Uniqlo ranks among the top global clothing brands today. We’ve all seen their simple, stylish clothes. What’s interesting is how they keep prices stable while other brands are raising them. This is no accident. The company uses smart planning, strong supply chains, and careful cost control.

Staying profitable in the global market is tough. But Fast Retailing shows us that the right strategy can make a big difference. Let’s explore how the company is staying strong, what’s helping them grow, and what risks they still face.

Company Background

Fast Retailing is a big name in global fashion. It runs over 2,500 stores worldwide. Along with Uniqlo, it owns GU, Theory, Comptoir des Cotonniers, and more. The company is popular across Japan, Asia, Europe, and North America.

The Tariff Landscape

The U.S. plans to impose new “reciprocal” tariffs from August 1 on goods shipped from Bangladesh, Vietnam, Sri Lanka, and others. Tariffs range from 20-40%, hitting many Asian factories. That hurts margins. We know this puts pressure on global brands.

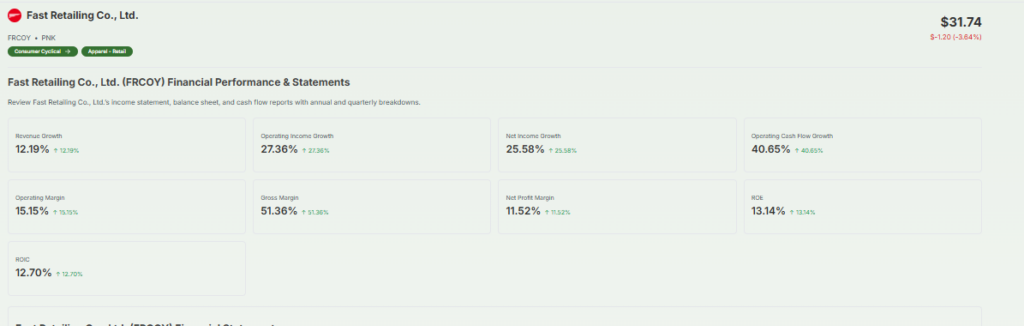

Fast Retailing’s Profit Forecast

Fast Retailing reported a 1.4% rise in operating profit to ¥146.7 billion in the quarter ending May 31.

This missed analyst estimate, yet the full-year forecast stays the same. The company says the tariff impact will be limited to only about 1-3% of profit.

How Fast Retailing Deals with Tariffs?

We see smart planning at play:

- Pre-shipping: They sent products to the U.S. early to dodge August tariffs.

- Supply diversification: They use 380 factories across Asia, not just one country.

- Flexible sourcing: Factories in Vietnam, Bangladesh, and Cambodia help shift loads smartly.

- Price strategy: They plan small price hikes in the U.S. to offset savings losses.

Performance Breakdown by Region

Here is the detailed view:

- Japan: Uniqlo Japan saw 11% sales growth and 17.8% profit increase over nine months.

- Greater China: Sales fell ~5% due to weak demand and cool weather.

- Southeast Asia, India, Australia: Strong growth led by summer-ready clothing.

- North America & Europe: Good momentum. North America could see a nearly 20% drop in H2 profit, but revenue remains strong.

Key Growth Drivers

We’ve identified four main growth engines:

- Lightweight, breathable AIRism and UV-protective wear are hot sellers.

- Online sales help cushion against in-store slowdowns.

- Simple, quality basics with global appeal.

- In China, they closed weaker outlets (“scrap and build”) and opened stronger ones.

Risks and Challenges Ahead

We see clear risks:

- More tariffs or trade friction could further trim profits.

- The China slowdown might last, affecting sales.

- Rising costs, including raw materials, and weak yen, could hurt margins.

- Competition from Zara, H&M, and fast-fashion rivals is stiff.

Final Words

Fast Retailing shows grit. They hold the forecast steady by shipping early, diversifying factories, and shifting prices. We’re seeing a strategy in action. They ride on strong product demand and smart sourcing. But risks remain: tariffs, China, cost swings. Still, their mix of strategy and flexibility makes them a model in rough trade seas.

Frequently Asked Questions (FAQs)

Uniqlo’s owner, Fast Retailing, achieved record-strong profits. In FY2024, operating profit rose over 31% to ¥500.9 billion. This marks a third straight year of record earnings.

For the year ending August 2024, Uniqlo International alone earned ¥283.4 billion in operating profit. Across all segments, Fast Retailing’s total operating profit hit ¥500.9 billion.

Disclaimer:

This content is for informational purposes only and not financial advice. Always conduct your research.

What brings you to Meyka?

Pick what interests you most and we will get you started.

I'm here to read news

Find more articles like this one

I'm here to research stocks

Ask our AI about any stock

I'm here to track my Portfolio

Get daily updates and alerts (coming March 2026)