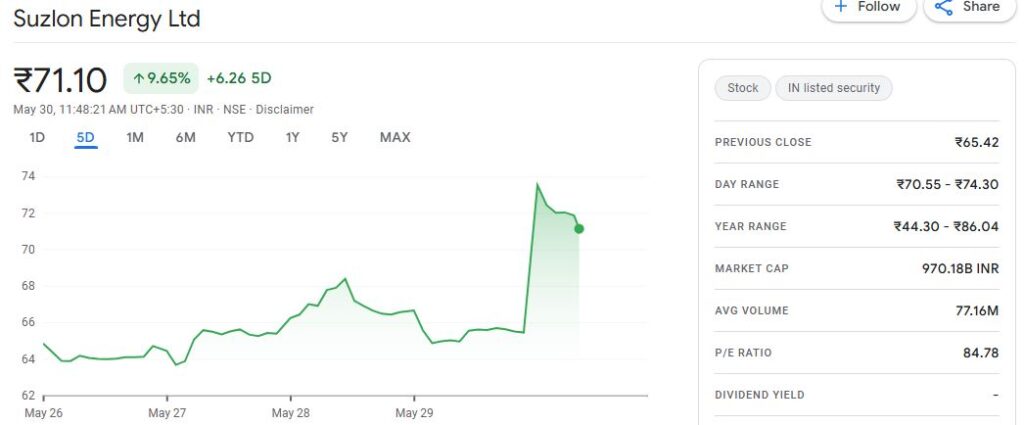

Suzlon Energy’s stock jumped 14% recently. This rise came after the company shared its strong results for the fourth quarter. Investors and analysts both cheered. The positive news gave a clear sign that Suzlon is on the right track. Let’s explore what made Suzlon Energy Q4 results stand out.

We will also look at why experts upgraded their views on the company. Finally, we will discuss what this means for Suzlon’s future. If you want to understand why Suzlon is gaining attention, keep reading.

Overview of Suzlon Energy

Founded in 1995, Suzlon Energy is an Indian multinational wind turbine manufacturer headquartered in Pune. Suzlon is a leading player in the renewable energy sector with approximately 20.9 GW of wind energy capacity installed across 17 countries.

The company offers a range of products and services, including wind turbine generators, operation and maintenance services, and turnkey solutions for wind energy projects.

Detailed Q4 Financial Results

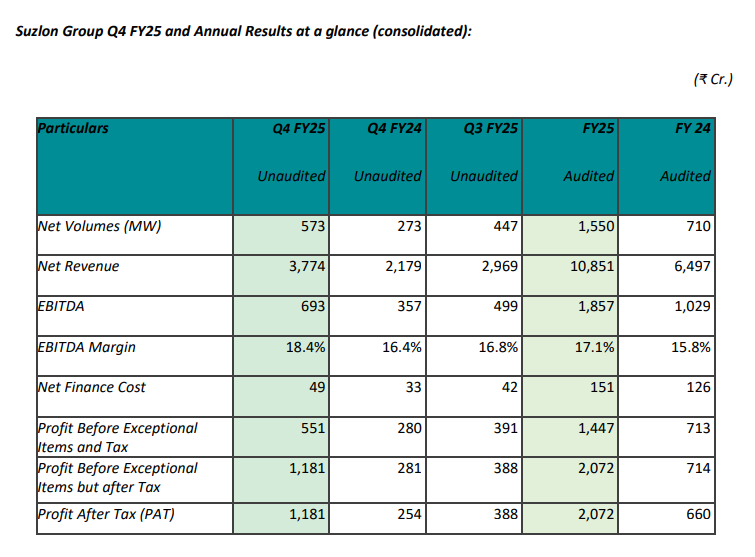

- Net Profit: ₹1,182 crore, a 365% increase from ₹254 crore in Q4 FY24.

- Revenue: ₹2,969 crore, up 73% from ₹1,552 crore in the same quarter last year.

- EBITDA: ₹500 crore, reflecting a 102% year-on-year growth.

- EBITDA Margin: 16.8%, indicating improved operational efficiency.

- Order Book: The company reported a record-high order book of 5.5 GW, with Commercial & Industrial (C&I) and Public Sector Undertaking (PSU) customers constituting approximately 80% of the total order book.

Analyst Upgrades and Market Reaction

After Suzlon Energy’s strong Q4 results, its stock price went up a lot. Motilal Oswal raised the target price to ₹83. They see a 27% chance the stock will rise more. This is because the company did well and market conditions look good.

Other analysts are also hopeful about Suzlon. ICICI Securities kept a “buy” rating with a target price of ₹54. They praised Suzlon’s strong new orders and better financial numbers. Many believe Suzlon has good chances to grow in the near future.

Factors Which Drive the Strong Q4 Performance

- Suzlon made a new record by delivering 447 MW in Q3 FY25. This helped the company earn more money.

- They improved their factories in Puducherry and Daman. Now, they can make 4.5 GW of wind energy parts.

- Suzlon got big orders, like a 204.75 MW project from Jindal Renewables. This made their biggest project grow to 907.20 MW.

- The government supports green energy. This helps Suzlon grow even more with good rules and rewards.

Future Outlook and Growth Prospects

Suzlon Energy is poised for continued growth, driven by its strong order book, expanded manufacturing capacity, and strategic partnerships. The company’s focus on Commercial & Industrial and Public Sector Undertaking customers positions it well to capitalize on the increasing demand for renewable energy solutions.

Analysts expect Suzlon Energy’s stock to rise about 30%. This is because new rules help the wind energy sector. One rule, called the Revised List of Models and Manufacturers (RLMM), says wind turbines must use more local parts. This helps Suzlon and other companies grow in India.

Wrap Up

Suzlon Energy Q4 results and analyst upgrades show the company is strong in renewable energy. Suzlon is ready to meet the rising demand for clean energy with many new orders and bigger factories. Their focus on important customers helps them stay ahead in the market.

Frequently Asked Questions (FAQs)

Suzlon’s stock price increased due to a 365% rise in Q4 net profit to ₹1,182 crore and a strong order book of 5.5 GW.

Analysts project a 30% compound annual growth rate (CAGR) in Suzlon’s profit from FY25 to FY27, driven by a healthy order book and expanded manufacturing capacity.

Suzlon with a strong financial performance, expanded capacity, and positive analyst outlook, is considered a good buy, though investors should assess individual risk tolerance.

Analysts have set a 12-month price target range of ₹60–₹83 for Suzlon. It indicates potential upside of 21-30%, depending on market conditions and execution.

Disclaimer:

This content is for informational purposes only and not financial advice. Always conduct your research.

What brings you to Meyka?

Pick what interests you most and we will get you started.

I'm here to read news

Find more articles like this one

I'm here to research stocks

Ask our AI about any stock

I'm here to track my Portfolio

Get daily updates and alerts (coming March 2026)