The stock market has been anything but quiet in early February 2026. Big names are moving on fresh earnings, supply issues, and changing investor expectations. Alphabet trimmed back on gains despite strong results, while Qualcomm’s stocks slid sharply after warning about memory shortages that are squeezing smartphone makers. Arm Holdings posted solid revenue yet its shares still dipped, showing how tough the AI chip race has become.

Meanwhile, e.l.f. Beauty surged on upbeat profit guidance, and BT drew attention for steady performance in telecom. These shifts matter for traders and long‑term investors alike. In an environment full of rapid sector rotation and macro uncertainty, now is the time to look closer at what’s driving these stocks and where they might head next.

Alphabet (GOOGL) Stock: Latest Data, Forecast & Analyst Insights

Current stock details and market context

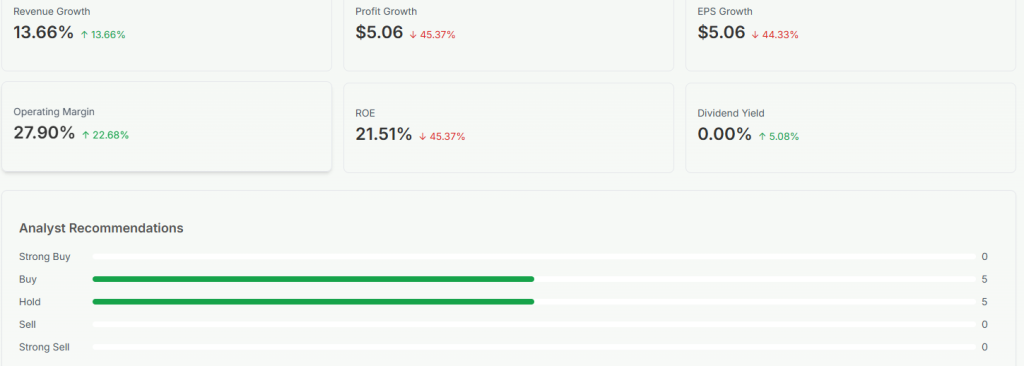

Alphabet’s Class C shares (GOOG) closed around US$340.70 on February 5, 2026, trading near key support and resistance levels. The 52‑week high sits near US$350.15, and the stock has delivered roughly 60% gains over the past year. Market sentiment is mixed, with tech sector rotation and AI spending narratives influencing investor positioning.

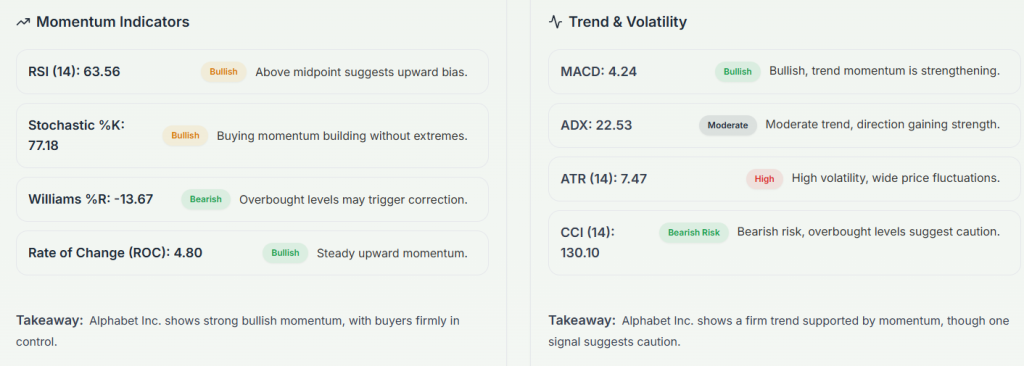

Technical analysis summary

Technical indicators show Alphabet above its 50‑day and 200‑day moving averages, signaling overall bullish trend support. However, momentum metrics like RSI and MACD hint at a short‑term pause or consolidation, suggesting traders may await clearer catalysts before a breakout continuation.

What Meyka says?

Meyka noted that Alphabet appeared among notable after‑hours movers, with tech peers and ad‑tech dynamics shaping its late‑session activity. Chart patterns imply volatility near current price levels.

Supporting insights from other analysts

Major financial outlets report that Alphabet’s strong Q4 2025 earnings and a hefty 2026 capital expenditure guidance (US$175-185 billion) pushed the stock into volatility, as investors balance growth outlook against higher spending expectations.

Qualcomm (QCOM): Weak Guidance and Chip Demand Headwinds

What’s driving the stock now?

Qualcomm shares fell about 9% in after‑hours trading on February 5, 2026, after reporting Q1 revenue of US$12.25 billion (a 5% year‑over‑year rise) but issuing cautious guidance due to unstable smartphone chip demand and memory supply bottlenecks that cloud near‑term visibility.

Technical and fundamental signals

Technically, QCOM remains below crucial moving averages, pointing to near‑term bearish pressure. Valuation metrics show a mid‑pack valuation in semiconductors with free cash flow and dividend features supporting long‑term holders.

Meyka’s assessment & forecast

Meyka’s stock grade for Qualcomm is A with a Buy suggestion, noting strong cash generation and resilient licensing revenue. Its 12‑month target range sits in the high US$170s to low US$180s if demand stabilizes later in 2026.

Other analyst views

Market commentary highlights that memory shortages affecting smartphone completions are a principal constraint on Qualcomm’s outlook. This has triggered a re‑rating of near‑term estimates despite solid technological positioning in 5G and edge AI platforms.

Arm Holdings (ARM): Strong Revenue Growth, Stock Weakness

Quarterly results and stock reaction

Arm reported record revenue of about US$1.24 billion in Q3 2026, a 26% year‑over‑year increase, and royalty revenue up 27%, driven by broader adoption of Arm architectures in AI and data center markets. Adjusted EPS was US$0.43, slightly above expectations.

However, the stock slid over 7–10% in after‑hours trading, partly due to licensing revenue missing estimates and investor focus on handset market pressures.

Technical and market context

Premarket trading trends showed Arm ADRs declining despite beating revenue and earnings, indicating broader tech volatility and concerns about near‑term smartphone market weakness.

Outlook and analyst commentary

Arm projects Q4 revenue above Wall Street forecasts, bolstered by demand for energy‑efficient AI chip designs across servers and edge devices. Analysts note that Arm’s role in the AI infrastructure stack remains a long‑term growth driver, even if stock price currently trades at a discount relative to fundamentals.

What investors should watch?

Key data points include royalty growth trends in cloud and smartphone chips and any updates from Arm’s March 24 event for new announcements.

e.l.f. Beauty (ELF): Earnings Beat and Strong Outlook

Recent performance and earnings

e.l.f. Beauty stock soared roughly 15-16% in after‑hours trading on February 4, 2026, after reporting Q3 fiscal 2026 results with 38% net sales growth to US$489.5 million and raising its full‑year 2026 outlook. The company forecast net sales of US$1.60-1.61 billion and EPS of US$3.05-3.10, both above Wall Street expectations.

Meyka’s long‑term price forecast

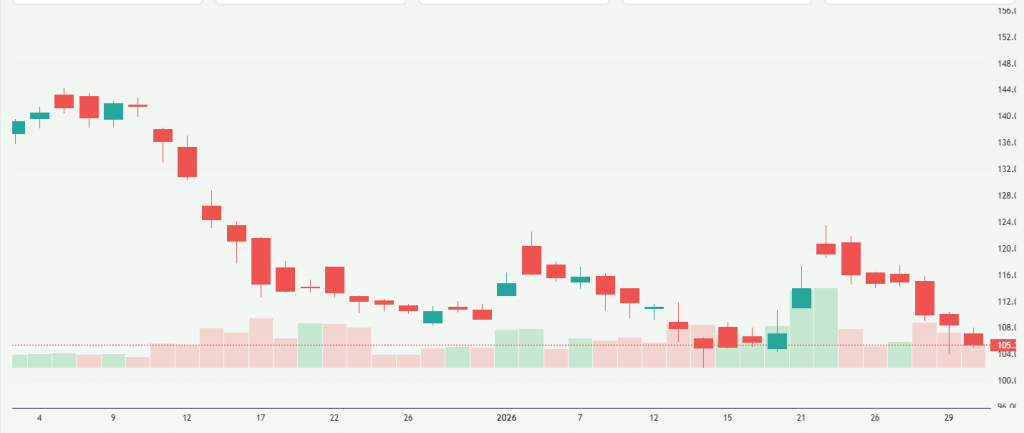

Meyka AI’s price model projects mixed near‑term and long‑term trends. For example, a 1‑year forecast around US$107 (+23.9%) suggests potential long‑term gains, while shorter horizons show volatility.

Consumer segment insights

Major analysts emphasize e.l.f.’s strong brand presence, continued international expansion, and diversified supply chains. Growth in affordable beauty and distribution channels like Sephora contributed to better results.

Considerations for investors

Tariffs and margin pressures remain risks, but recent earnings and raised guidance show resilience amid economic headwinds.

BT Group (BT.A): Telecom Stability and Strategic Moves

BT’s latest results and stock status

BT Group’s stock has been trading around 206-209 pence as of early February 2026, showing strength against a 52‑week range of about 142-224 pence and offering a dividend yield near 3.9%. The company continues to reaffirm guidance and aims for increasing free cash flow in the coming years.

Strategic developments

On February 4, 2026, BT completed the sale of its Radianz unit, which helped stock gains and reflected portfolio realignment. Broadband performance is stabilizing with fewer line losses than expected, and full‑fibre broadband reach has expanded above 21 million homes and businesses, positive operational signals.

Analyst sentiment and risks

Analyst views are mixed, with target prices ranging widely, reflecting uncertainty about telecom demand and competitive pressures. Some upgrades see consolidation potential in European telecoms, but a neutral consensus persists.

Investor takeaway

BT remains a value‑oriented telecom play with current income appeal and strategic growth in fibre and 5G, though near‑term revenue contraction and competition persist.

Wrap Up

February 2026 highlights both opportunities and caution for major stocks. Alphabet invests in AI and cloud, Qualcomm faces chip supply challenges, Arm grows royalties, e.l.f. Beauty beats earnings, and BT remains stable. Investors should monitor earnings, sector trends, and technical signals. Tools like AI stock analysis platforms can help spot early market moves. Understanding fundamentals and analyst insights is key to smart investing.

Frequently Asked Questions (FAQs)

Alphabet stock fell in early February 2026 after the company said it would spend much more on AI and other projects. Higher spending worried some investors despite strong earnings.

Qualcomm stock dropped because the company gave weak sales guidance for 2026. It said a global shortage of memory chips was hurting smartphone demand and overall outlook.

e.l.f. Beauty’s stock has mixed signals. Sales grew and results beat estimates, but revenue forecasts and cost pressures made some investors cautious.

Disclaimer:

The content shared by Meyka AI PTY LTD is solely for research and informational purposes. Meyka is not a financial advisory service, and the information provided should not be considered investment or trading advice.

What brings you to Meyka?

Pick what interests you most and we will get you started.

I'm here to read news

Find more articles like this one

I'm here to research stocks

Ask our AI about any stock

I'm here to track my Portfolio

Get daily updates and alerts (coming March 2026)