Infosys shares have kicked off FY26 with a strong start.

India’s second-largest IT services company, Infosys, has reported a 9 percent year-on-year (YoY) increase in profit after tax (PAT) in its Q1 FY26 results, drawing attention from investors and analysts alike. The company posted a net profit of ₹6,921 crore, signaling stable earnings even amid a global IT slowdown.

Advertisement

So, the question on everyone’s mind is: Should you invest in Infosys shares now? Let’s break it down.

Infosys Shares Gain Momentum After Q1 Results

Infosys shares came into the spotlight immediately after the earnings announcement. The company’s revenue for the quarter stood at ₹38,202 crore, reflecting a modest revenue growth of 5.8 percent YoY. The EBIT margin also remained strong at 20.4 percent, beating some street estimates.

According to ET Now, the sequential revenue growth was slightly weaker, but the strong margin performance and new deal wins balanced the outlook.

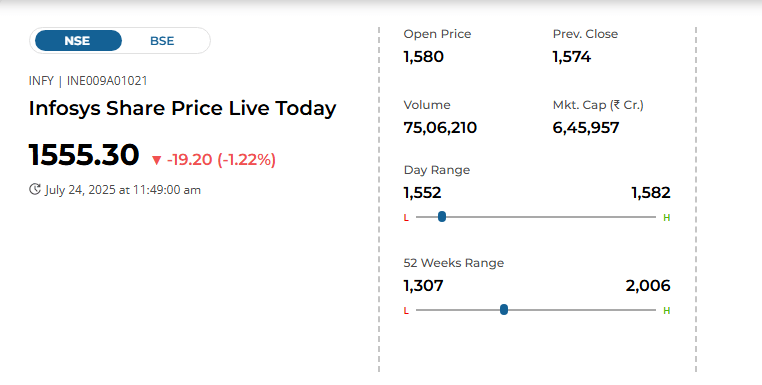

Infosys Share Price Today Reflects Cautious Investor Sentiment

As of July 24, 2025, the Infosys share price is trading at ₹1,555.30, down ₹19.20 (-1.22%) from the previous close. Despite reporting a 9% growth in PAT (Profit After Tax) in Q1, the stock opened at ₹1,580 but slipped during intraday trade.

Here’s what the live data tells us:

- Day’s Range: ₹1,552 – ₹1,582

- 52-Week Range: ₹1,307 – ₹2,006

- Volume Traded: Over 75 lakh shares

- Market Cap: ₹6.45 lakh crore

This decline indicates mixed investor reactions to the Q1 numbers. While profit growth appears healthy, the muted revenue guidance may have led to profit booking or short-term caution.

Investors are now looking for stronger cues from upcoming quarters or global IT sector stability before making aggressive buy decisions on Infosys shares.

Pro Tip: Keep an eye on the ₹1,550 support level. If the stock dips below it with high volume, it could indicate short-term weakness.

What’s Driving the Growth for Infosys?

Infosys reported large deal wins worth $4.2 billion this quarter, with 54 percent of these being net new contracts. This indicates strong demand for Infosys services, especially in areas like cloud, AI, and digital transformation.

In its report, Business Standard noted that these new deals could help support future revenue growth even as some global clients cut back on discretionary spending.

Why are Investors Divided on Infosys Shares?

While the earnings are solid, some experts suggest caution. Infosys maintained its FY26 revenue growth guidance at 1 to 3.5 percent, which is considered conservative. This flat guidance has led to mixed analyst reactions, especially with growing global uncertainties.

As per CNBC-TV18, the company is staying cautious due to a slower recovery in client spending, especially in the US and Europe.

What Do the Charts Say About Infosys Shares?

Technical analysts believe that Infosys shares have support around ₹1,450 and resistance near ₹1,580. As long as the price holds above the support zone, a breakout could be possible in the coming weeks.

NDTV Profit tweeted:

“Infosys sees decent PAT growth, but cautious guidance keeps stock movement in check. Keep an eye on volume breakout levels.”

Should You Buy, Hold, or Sell Infosys Shares?

Here’s what analysts recommend:

- Buy, if you believe in long-term digital transformation growth and trust Infosys to maintain strong deal momentum.

- Hold, if you’re already invested and waiting for better growth clarity in the next quarter.

- Sell, only if you’re a short-term trader worried about limited upside in the next few months.

A tweet from @Stockstudy8 summed it up:

“Q1 looks good for Infosys. PAT up 9 percent. But guidance flat. Investors should watch the next quarter closely.”

What About Dividends and Payouts?

Infosys did not announce any new dividend this quarter. The company is known for regular dividend payouts, so investors can expect announcements closer to the end of FY26 or after Q2 results.

Economic Times reported that Infosys continues to focus on cost optimization while maintaining consistent returns to shareholders.

Is the AI Push Helping Infosys?

Yes, Infosys is actively investing in generative AI and cloud automation tools. These innovations are expected to improve productivity and reduce costs for global clients, which may enhance deal value and win rates.

As highlighted in this YouTube review of Infosys Q1 results, analysts pointed to the AI transformation pipeline as a major long-term opportunity for Infosys.

Final Thoughts: Are Infosys Shares Worth Buying Now?

Infosys has delivered a solid Q1 performance with healthy margins, strong deal wins, and steady profit growth. However, its low revenue guidance and ongoing global uncertainties suggest that investors should stay cautious.

If you’re looking at Infosys shares for the long run, the company’s financial strength, brand trust, and digital focus make it a promising pick. For short-term traders, it may be wise to wait and watch how the next quarter unfolds.

Advertisement

FAQ’S

Yes, Infosys is considered a fundamentally strong IT company with consistent growth and dividend payouts. However, investors should analyze market conditions and long-term goals before investing.

Analysts expect moderate growth for Infosys with short-term volatility due to global IT demand. Long-term outlook remains positive if digital transformation continues.

Yes, Infosys is expected to grow with increasing global demand for AI, cloud, and digital services. Strategic deals and expansion into new tech areas support this growth.

As of July 2025, the PE ratio of Infosys is approximately 23-25, depending on intraday price and trailing earnings. It reflects moderate valuation within the IT sector.

Blue-chip stocks like Infosys, TCS, and Reliance are safe bets in uncertain markets. However, always consider market trends, sector strength, and individual goals before investing.

Infosys is expected to offer an average 6–9% salary hike in 2025, with higher hikes for high performers. However, this may vary based on company performance and market conditions.

Infosys has given a return of around 20–25% over the last 3 years, including dividends. This includes periods of strong growth and some market correction.

Look for companies with strong fundamentals, low debt, increasing profits, and positive sector outlook. Also track news, earnings reports, and technical indicators.

Disclaimer

This content is made for learning only. It is not meant to give financial advice. Always check the facts yourself. Financial decisions need detailed research.

Advertisement

What brings you to Meyka?

Pick what interests you most and we will get you started.

I'm here to read news

Find more articles like this one

I'm here to research stocks

Ask our AI about any stock

I'm here to track my Portfolio

Get daily updates and alerts (coming March 2026)