Shakti Pumps just had a tough day in the stock market. On August 5th, its share price dropped nearly 8% after the company shared its Q1 results for the financial year 2025-26. At first glance, the numbers didn’t look too bad revenue and profit were slightly higher than last year. But when we dug deeper, we saw some cracks.

Investors were hoping for strong growth after a solid last quarter. Instead, the company’s profits fell compared to the previous quarter, and its margins took a hit. That’s not a good sign, especially when you’re spending big on future projects.

So, why did the stock fall when profits still went up year over year? It’s a mix of timing, market expectations, and a few bold moves by the company’s leadership. Let’s break down what really happened, what these results mean, and what we should watch for in the coming months.

Shakti Pumps: Q1 FY26 Financial Highlights

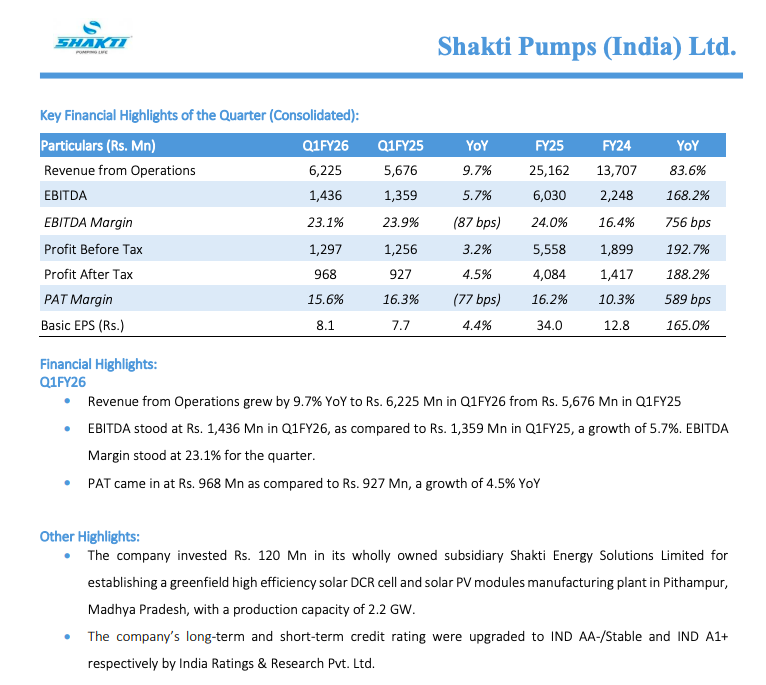

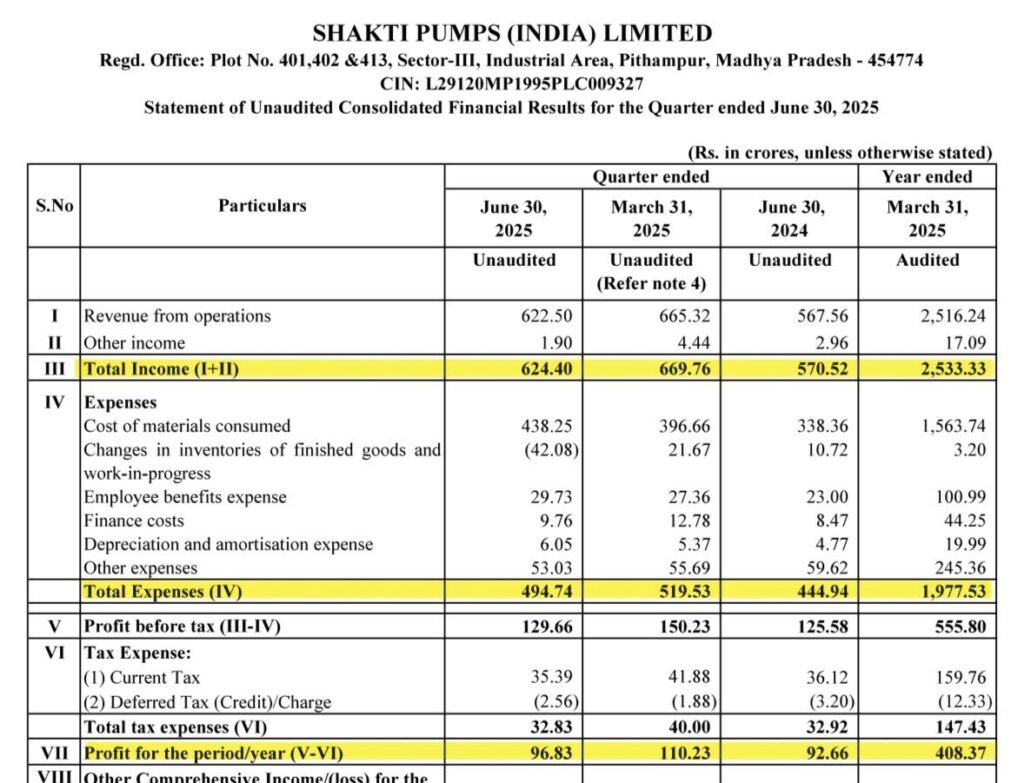

We start with the numbers. In Q1 FY26, Shakti Pumps India posted revenue of ₹622.5 crore, up about 9.7% year‑on‑year from ₹567.6 crore in Q1 FY25, but down 6.4% from ₹665.3 crore in Q4 FY25. Profit after tax stood at ₹96.8 crore, a 4.5% rise YoY, yet dropped 12% sequentially from ₹110.2 crore in the prior quarter. EBITDA rose 5.7% YoY to ₹143.6 crore, though the margin declined to 23.1% from 23.9% in Q1 FY25.

Stock Market Reaction

Despite modest growth, the market responded sharply. Shares plunged nearly 8%, trading down to around ₹865 on the BSE. Intraday low touched ₹825.65, as investors reacted to the sequential slowdown despite the multibagger rally of over 2,700% over five years.

Reasons Behind the Reaction

Sequential Weakness Disappoints

Investors focus more on current momentum than just year‑on‑year gains. Here, sequential revenue and profit declined, and margins shrank. Q4 FY25 had stronger numbers. So the quarter felt underwhelming, overshadowing YoY growth.

Big Capex Plans and Borrowing

Shakti Pumps has unveiled a ₹1,700 crore capex rollout. This includes ₹250 crore each for pump‑motor expansion and EV facility, and ₹1,200 crore for building a solar cell and PV module plant in Pithampur, MP. The board doubled borrowing limits to ₹3,000 crore, causing concern that rising debt may pressure finances, especially with soft earnings momentum.

Governance Moves Raise Eyebrows

The proposal to double the chairman’s pay from ₹9 crore to ₹18 crore annually also drew criticism. Some investors felt it poorly timed after such a tepid quarter.

Positives and Long‑Term Outlook

We see solid long‑term strength here despite near‑term pressure.

As of August 1, 2025, Shakti held an order book of around ₹1,350 crore. It secured orders via state tenders across Maharashtra, MP, Rajasthan, Uttar Pradesh, Haryana, Punjab, and Jharkhand.

Export revenues have grown at nearly 25% CAGR over four years. The company serves markets like Haiti, Uganda, Bangladesh, Nepal, and is expanding in the USA, Middle East and Africa.

Shakti continues to lead solar pump installation under PM‑KUSUM with ~25% market share in key agri states. It is also expanding into rooftop solar under PM Surya Ghar scheme, EV mobility, and industrial solar driving new value.

The company improved receivable days from 178 in FY24 to 152 in FY25, and targets 120 by end-FY26.

Shakti raised ₹2,926 million through a QIP to partly fund the solar project. Ratings firm India Ratings upgraded the company’s credit ratings to IND AA‑/Stable and IND A1+.

Industry & Market Context

The fall in share price isn’t due to sector weakness. The pump and clean energy sector held up better. Instead, the drop reflects investor concern over recent performance and large near‑term debt plans. The stock’s technical indicators also signalled a short‑term downtrend following the earnings shock.

What This Means for Investors?

For short‑term traders, the price dip might offer a reset opportunity if valuations fall into sensible range. But long‑term holders must watch tightly. We must assess how capex is funded, how fast receivables fall, and how soon margins recover. Executive moves like higher pay may also shape confidence.

If Shakti executes its order book, scales up clean‑energy operations, and keeps accounting disciplined, it could regain investor trust and re-enter a growth trajectory.

Wrap Up

Q1 FY26 brought mixed news: growth was modest, margins slipped, and debt plans loomed. The nearly 8% share price slide reflects investor worry over momentum rather than fundamental breakdown. Still, the company has strong capabilities in solar pumps, expanding exports, clean-energy focus, and a robust order pipeline. If in coming quarters Shakti delivers on execution, we may see renewed confidence and a return to growth.

Frequently Asked Questions (FAQs)

Shakti Pumps shares are falling because profit and revenue dropped compared to last quarter. Investors also worry about its big spending plans and a drop in profit margins.

As of August 5, 2025, some investors think Shakti Pumps may be overvalued due to its high past returns. Others believe it’s fairly priced if the company meets its future growth goals.

The company’s future looks positive if it handles spending well. Its focus on solar energy, exports, and clean tech could help it grow in the long run.

Disclaimer:

This is for information only, not financial advice. Always do your research.

What brings you to Meyka?

Pick what interests you most and we will get you started.

I'm here to read news

Find more articles like this one

I'm here to research stocks

Ask our AI about any stock

I'm here to track my Portfolio

Get daily updates and alerts (coming March 2026)