India’s railway network is the fourth largest in the world. It carries more than 8 billion passengers every year and handles a huge share of freight. With such scale, railway companies play a big role in the country’s growth story. Investors often look at railway PSU stocks because they give both safety and long-term potential. After the Union Budget 2025, railway-related stocks gained more attention as the government increased its spending on infrastructure and modernization.

Among these, Rail Vikas Nigam Limited (RVNL) and Indian Railway Finance Corporation (IRFC) stand out. Both serve different purposes but are equally important for the Indian Railways. RVNL is the builder. It takes charge of big projects, from new tracks to electrification. IRFC is the financer. It raises money and supports the railways with funds and leasing models.

Now, after Q1 FY2025 results, many of us are asking: which stock looks stronger? Is it RVNL with its growth-driven projects, or IRFC with its steady financing model? Let’s compare both (RVNL vs IRFC) and see which one may be the better pick.

Company Overview: RVNL vs IRFC

Rail Vikas Nigam Limited (RVNL)

RVNL builds railway assets. The company executes tracks, bridges, signaling, and electrification. It works mostly on EPC and turnkey models for Indian Railways and state bodies. Execution speed, site clearances, and contractor coordination drive outcomes. A large order book offers multi-year revenue visibility and supports bids in metro, highways, and overseas projects. Recent wins include a ₹178.65 crore signaling and telecom contract from IRCON, due in about 11 months. This shows steady tender momentum even after a soft quarter.

Indian Railway Finance Corporation (IRFC)

IRFC is the dedicated financier for Indian Railways. It raises funds and leases rolling stock and project assets to the railways. The model yields predictable interest income with low credit risk because counterparty risk sits with the sovereign. Scale depends on railway capex and borrowing plans. The investor updates and annual reports highlight a stable annuity profile and tight spreads management.

RVNL vs IRFC: Q1 FY2026 Results Snapshot

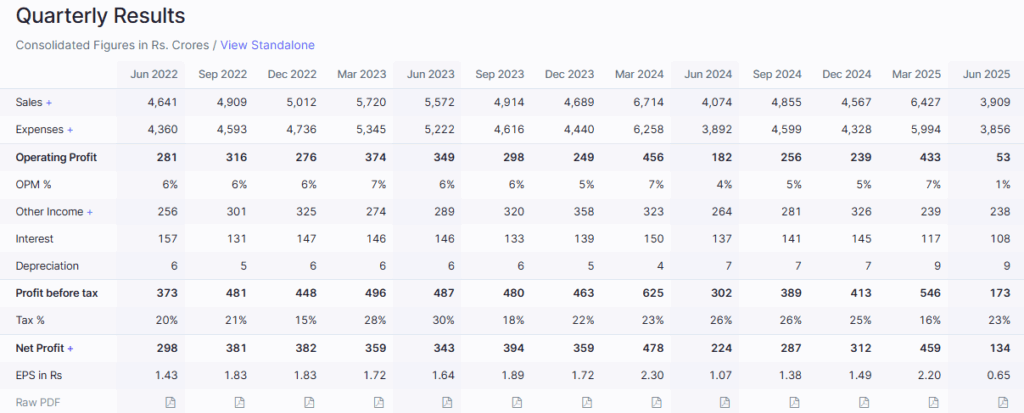

RVNL (Q1 FY2026)

Total income came in at ₹3,908.77 crore, down 4.05% year on year. Operating profit fell sharply to ₹44.02 crore, and PAT declined 39.92% to ₹134.53 crore. Operating margin slipped to 1.13%. The miss reflects slower execution and lower other income. Markets reacted to the earnings dip, but order inflows remain active.

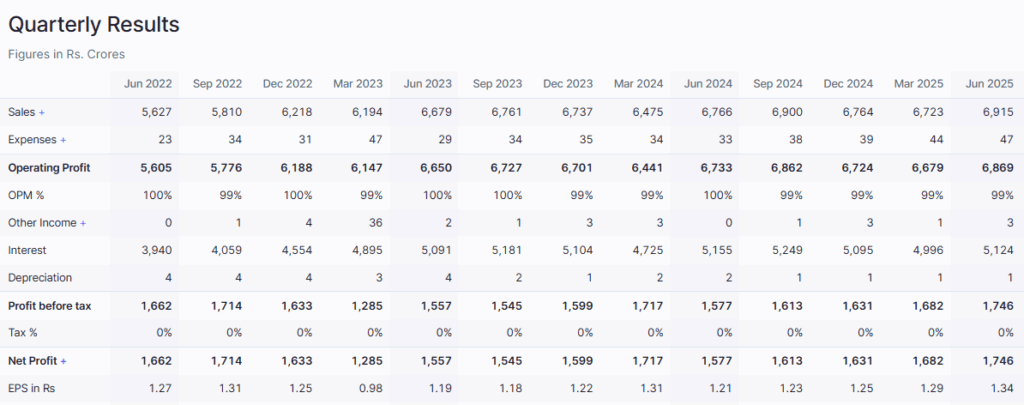

IRFC (Q1 FY2026)

Total income was ₹6,915.38 crore, up 2.21% year on year. Operating profit stood at ₹6,867.22 crore, up 2.02%. PAT rose 10.71% to ₹1,745.69 crore. Operating margin held near 99% due to the leasing model. Growth was modest, yet steady, with spreads protected despite rate moves.

What does that mean?

RVNL showed execution stress in the quarter. IRFC delivered predictable growth and stable margins. The contrast lines up with their different business models.

Business Model & Risk Analysis

Rail Vikas Nigam Limited (RVNL)

EPC execution can scale fast when sites are ready and supplies flow. It also carries risk from delays, inflation, and subcontractor issues. Working capital can tighten when certifications or clearances lag. A large order book reported at over ₹1 lakh crore as of June 30, 2025, helps smooth near-term volatility and supports bids beyond core rail, including metros and overseas jobs. But quarterly profits can swing with project milestones.

Indian Railway Finance Corporation (IRFC)

IRFC’s lease-finance model produces annuity-like cash flows. Credit risk is minimal because the counterparty is Indian Railways. The key variables are the cost of funds, spread management, and the scale of railway capex. Rising rates can compress spreads if not passed through. Capital adequacy and ALM discipline remain central. Recent investor materials show stable revenue growth and profitability in Q1 FY2025-26, consistent with the long-term pattern.

Stock Performance & Valuation

Valuation snapshot (as of mid-August 2025)

RVNL trades at a high P/E relative to its history and sector, around 55-58x TTM on multiple trackers. This implies a premium for execution leverage and rail capex exposure. IRFC trades near 24–25x TTM, closer to the broader financials cohort and below RVNL’s multiple. IRFC’s P/B sits near ~3.0, with a modest dividend yield reported around ~1.3%. Always cross-check live screens before acting.

Recent sentiment drivers

RVNL corrected after reporting a near 40% profit drop in the latest June quarter, then bounced on fresh order news from IRCON. Brokerage commentary also flagged rich valuations versus near-term earnings. IRFC’s sentiment stayed steadier on the back of consistent earnings and visible railway borrowing needs.

Growth Outlook & Future Catalysts

RVNL project pipeline and diversification

Rail electrification, capacity additions, station upgrades, and metro orders remain solid demand drivers. The recent IRCON signaling order underlines healthy tendering. The reported order book above ₹1 trillion suggests multi-year revenue visibility if execution speeds up and clearances come on time. Any uptick in Dedicated Freight Corridor-linked works or high-speed rail packages can boost run-rate.

IRFC-capex cycle and balance sheet strength

Railway capex plans guide IRFC’s disbursements and lease income. As the rail network adds rolling stock and upgrades assets, IRFC’s loan book can rise in lockstep, subject to leverage and spread control. Q1 data points show steady income growth and high operating margins, consistent with a predictable, annuity-type profile. Policy clarity on capex and interest-rate trends is are key watch item.

Which Stock Looks Stronger After Q1 2025?

IRFC looked stronger right after Q1 FY2025. Earnings grew, margins held, and the risk profile stayed low. The stock’s valuation sat at a more moderate P/E band compared with RVNL. For capital preservers who prefer steadier cash flows, IRFC fits better.

RVNL offers higher upside if execution normalizes and orders convert to revenue faster. The large order book and fresh wins support that view. But the latest quarter showed downside when site progress slowed. The premium P/E already prices in a lot of future delivery.

Net take: IRFC for stability and steady compounding; RVNL for higher-beta exposure to rail capex, with quarter-to-quarter swings.

Wrap Up

RVNL vs IRFC, both PSUs sit at the heart of India’s railway build-out. After Q1 FY2025, IRFC’s numbers looked cleaner and more stable. RVNL remains a growth story tied to execution and cash conversion. Short-term sentiment favored IRFC due to steady profit growth and lower perceived risk. Long-term returns for RVNL hinge on converting its large order book into revenue at a faster clip and protecting margins. Any decision should weigh risk tolerance, time horizon, and the live valuation screens cited above.

What brings you to Meyka?

Pick what interests you most and we will get you started.

I'm here to read news

Find more articles like this one

I'm here to research stocks

Ask our AI about any stock

I'm here to track my Portfolio

Get daily updates and alerts (coming March 2026)