Rocket Companies just made headlines and it’s not by chance. The RKT stock jumped 8.04% in a single day, and here’s why: the company announced a major move to acquire parts of Redfin, a well-known real estate platform. Alongside this, Rocket also rolled out a brand-new pricing strategy that’s turning heads in the mortgage industry.

We’re seeing big shifts in how homes are searched, bought, and financed. Rocket’s bold steps could change the game.

Let’s break it all down into what the deal includes, why the market reacted so strongly, and what it means going forward.

Company Snapshot: Rocket Companies (RKT)

Rocket Companies is a Detroit-based fintech powerhouse. Many know it for Rocket Mortgage, the online mortgage platform born from Quicken Loans. Over time, Rocket expanded into real estate tech fueled by acquisitions like Redfin and Mr. Cooper and fintech like Rocket Money and Rocket Loans.

Despite broader mortgage pressures this year, the company reported strong Q1 revenue near $2.67 billion and a 32.5% pre-tax margin. Still, it posted negative free cash flow (~–$811 million) and a $212 million net loss, highlighting its investment-heavy phase.

The Redfin Acquisition: Key Details

On July 1, 2025, Rocket closed its $1.75 billion all-stock purchase of Redfin. This deal brings together Rocket’s digital mortgage reach and Redfin’s popular home‑search and brokerage platform. The companies now aim for “Rocket Preferred Pricing,” offering a 1 percentage‑point rate buydown in the first year or up to $6,000 in lender credits when financing through Rocket Mortgage with a Redfin agent.

The merger simplifies homebuying by converging search, mortgage, and brokerage in one seamless flow.

Market Reaction: Why the 8.04% Surge?

When the acquisition and pricing program became public, RKT stock jumped 8.04% in a single day. Intraday gains also spiked; RKT briefly surged nearly 9%.

Investors appeared energized by synergies and cost savings in homebuying. They also welcomed new mortgage offerings, like bridge loans tied to home equity. Analysts see potential continued upside ahead of Q2 earnings, scheduled for late July.

New Pricing Strategy: What’s Changing?

Rocket Preferred Pricing is the newest move. Buyers working with Redfin agents can choose a 1% rate cut in year one or up to $6,000 lender credit. This applies for conventional, FHA, or VA loans.

The goal is simple: lower upfront costs and bundle financing with search and brokerage tools. It’s a bold bet in a high-rate market to win more business and keep clients in the integrated ecosystem.

Investor Perspective: Bull vs. Bear Case

Weighing the upside and risk:

Bull Case:

- The Redfin integration fast-tracks growth and boosts efficiency.

- Offering unique bundled discounts may win more customers.

- Recent mortgage volume and revenue gains show momentum.

Bear Case:

- Combining large units can lead to operational hiccups.

- High interest rates may dampen loan volumes and profits.

- Workforce cuts (~2%) hint at cost pressure.

Analysts are mixed: average 12‑month targets hover ~$13.86, with highs near $16. That reflects cautious optimism.

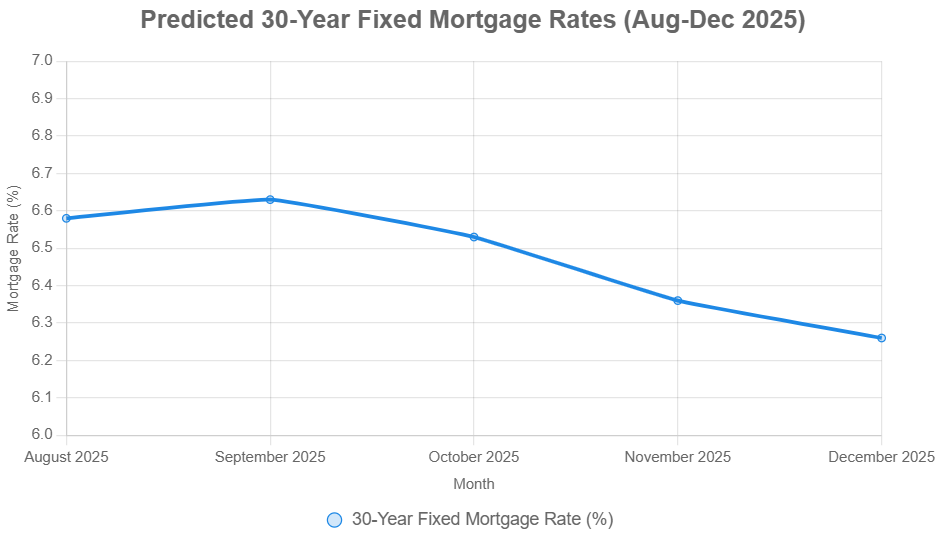

Industry Outlook: Mortgage & Proptech Trends

The mortgage sector is in flux. High interest rates hovering near 6.7%-6.9% have slowed demand. Yet, proptech firms like Zillow and Rocket benefit from consumer preference for digital services.

Rocket stands out by offering a full-stack solution: search, finance, brokerage, and servicing via Mr. Cooper acquisition. This aligns with broader industry trends favoring one-stop platforms but exposes them to antitrust scrutiny. U.S. senators have flagged the deal, claiming it may limit competition and raise costs.

What to Watch Going Forward?

Here’s what investors should track:

- Q2 earnings (late July): Any surprises in volumes, margins, or pricing.

- Integration milestones: How smoothly Redfin merges into Rocket, and how lender discounts impact origination growth.

- Macro factors: Fed rate decisions and mortgage yield curves.

- Regulatory action: Any updates from the DOJ/FTC on antitrust concerns.

Analyst ratings remain varied Goldman Sachs and UBS are neutral with $14-$16 targets, while Keefe Bruyette & Woods trimmed to Market Perform at $13.

Bottom Line

Rocket’s 8.04% stock jump reflects investor excitement around its bold new strategy. Rocket is betting on efficiency and customer loyalty. While high interest rates and regulatory oversight pose challenges, the Redfin acquisition and new pricing tools mark a major shift.

For investors, the coming quarters will reveal whether this integrated vision can deliver growth and whether lower rates or tighter scrutiny help or hinder Rocket’s journey.

Frequently Asked Questions (FAQs)

Analysts expect Rocket stock (RKT) to stay between $13 and $16 over the next year. Some believe it may grow if interest rates drop or business improves.

Rocket bought Redfin in a deal worth about $1.75 billion. The payment was made in stock, not cash, and the deal was completed in July 2025.

Rocket used only its own stock to buy Redfin. The two companies now work together, offering discounts to homebuyers who use both Rocket Mortgage and Redfin services.

Redfin stock rose because investors liked the Rocket deal. They saw a chance for better services, more customers, and stronger business by working with Rocket.

It means Rocket Companies now owns Redfin. They want to bring home searching, loans, and real estate agents all into one place for buyers.

Disclaimer:

This content is for informational purposes only and not financial advice. Always conduct your research.

What brings you to Meyka?

Pick what interests you most and we will get you started.

I'm here to read news

Find more articles like this one

I'm here to research stocks

Ask our AI about any stock

I'm here to track my Portfolio

Get daily updates and alerts (coming March 2026)