Qfin Holdings’ Q2 2025 Earnings: Contradictions in Loan Demand and Risk Controls

Key Takeaways

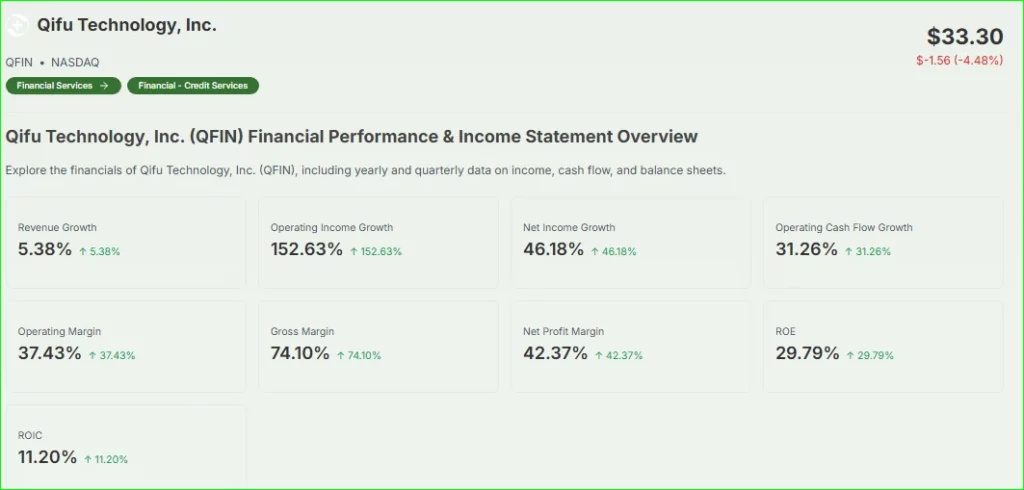

- Revenue and profits rose strongly with total revenue of RMB 3.53 billion (USD 486.3 million) and net income of RMB 1.04 billion (USD 143.3 million).

- Earnings per ADS improved to USD 0.88 from USD 0.78, showing consistent profitability growth year-over-year.

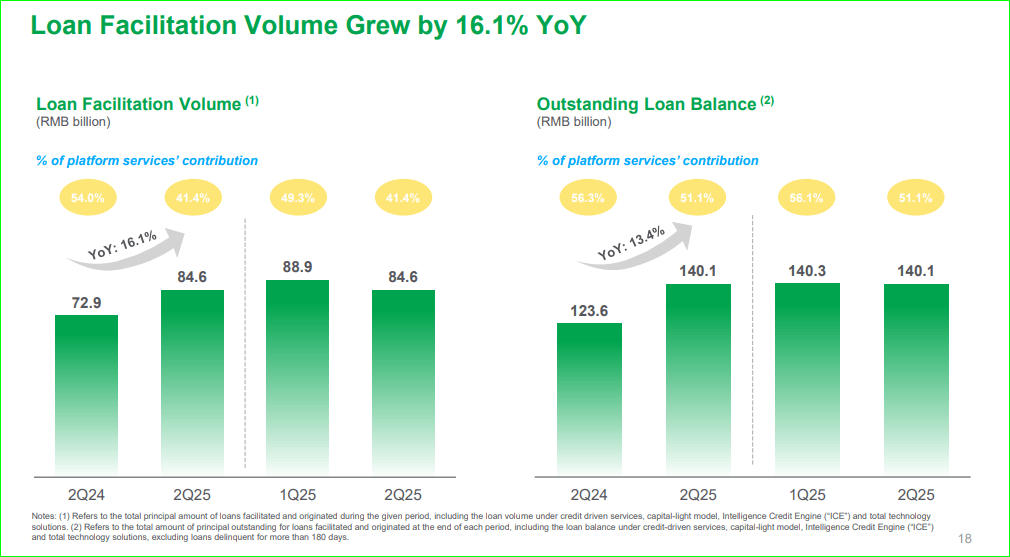

- Loan demand is rising but QFIN remains cautious, focusing on high-quality borrowers rather than rapid expansion.

- Non-performing loans stayed stable at 30.8%, reflecting disciplined credit risk management and portfolio quality.

- Funding and liquidity remain strong through diversified bank and non-bank partnerships, keeping costs competitive.

QFIN Holdings (Qifu Technology, Inc.), a leading digital consumer finance platform in China, reported mixed second-quarter 2025 results that revealed both strong earnings momentum and underlying contradictions between growing consumer loan demand and the company’s cautious risk control measures. While revenue and profits exceeded expectations, management’s tone suggested a more conservative lending approach despite an expanding market.

Strong Headline Numbers but Nuanced Trends

According to the Qfin Holdings’ Q2 Earnings release, total revenue for the quarter rose 15.7% year-over-year to RMB 3.53 billion (USD 486.3 million), driven primarily by stable transaction volumes and improved take rates. Net income reached RMB 1.04 billion (USD 143.3 million), translating to earnings per ADS of USD 0.88, up from USD 0.78 in the same period last year.

The Nasdaq listing summary for QFIN highlighted that the company’s non-performing loan (NPL) ratio remained steady at 30.8% in its risk-sharing loan portfolio, a figure closely watched by investors. The stable NPL level suggests effective credit controls but also indicates a reluctance to aggressively expand lending to riskier borrowers despite a recovery in consumer demand.

Investor Reactions and Market Sentiment

Market watchers took note of the stock’s muted price action following the results. One post-earnings tweet from @Chart_Guy observed:

“$QFIN popped briefly after earnings but sellers stepped in. Loan growth is there, but they’re not pushing the throttle due to risk.”

Another market comment from @overnight_stock summarized the mood:

“Solid quarter for $QFIN, but conservative guidance caps upside. They’re playing defense in a growth environment.”

This sentiment reflects the key contradiction of Q2 2025, demand for consumer loans is rising in China, yet QFIN remains firmly committed to a measured approach.

The Loan Demand vs. Risk Management Paradox

China’s consumer finance sector has seen a rebound in 2025 as post-pandemic spending habits normalize. QFIN’s management acknowledged “robust loan origination interest” during the quarter, but in the same breath emphasized “stringent borrower assessments” and “prioritization of high-quality growth over scale.”

This stance was clearly outlined in the Ainvest coverage, which noted that the company is actively balancing profitability and portfolio quality rather than chasing market share. It also pointed out that QFIN’s funding cost optimization strategy, particularly through deeper partnerships with institutional lenders, is helping maintain margins without relaxing risk controls.

Funding Strategies and Institutional Partnerships

The Q2 release also emphasized the role of diversified funding channels in sustaining performance. QFIN continues to secure capital from both traditional banks and non-bank financial institutions, enabling it to match loan origination growth without excessive balance sheet exposure.

Management reiterated that these partnerships are critical to maintaining liquidity flexibility and ensuring that lending expansion does not come at the expense of credit quality. This strategy has also helped QFIN keep funding costs competitive in a tightening regulatory environment.

Official QFIN Press Release Highlights

In its official investor relations statement, QFIN’s CEO and CFO emphasized the following key points:

- Focus on quality over quantity in loan origination, targeting borrowers with stronger credit profiles.

- Stable NPL ratio at 30.8% in the risk-sharing portfolio, indicating disciplined credit management.

- Revenue growth supported by higher transaction fees and funding cost efficiencies.

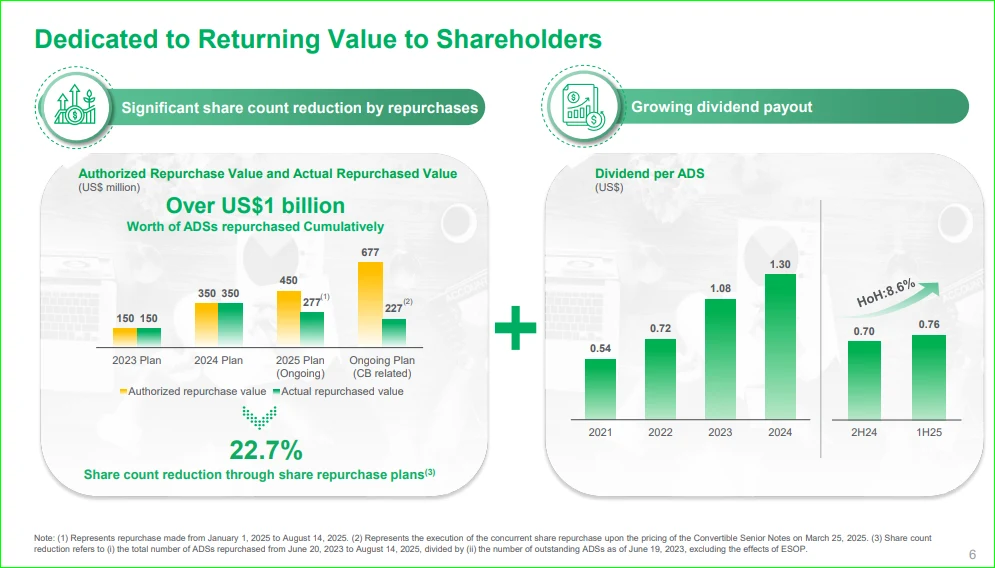

- Steady dividend policy to reward shareholders while investing in technology and risk assessment capabilities.

Management also reaffirmed its full-year 2025 guidance, forecasting moderate loan growth with a continued focus on asset quality.

Analyst Perspectives for Qfin Holdings’ Q2 Earnings

MarketBeat’s earnings report on QFIN echoed the sentiment that while the numbers were solid, the company’s cautious guidance may limit short-term stock upside. Analysts see the conservative approach as a double-edged sword:

- Positive: Limits exposure to potential credit losses if China’s macroeconomic recovery falters.

- Negative: May result in slower market share gains compared to more aggressive competitors.

Some also pointed out that QFIN’s ongoing investments in AI-driven credit scoring and borrower monitoring tools could pay dividends in future quarters, allowing for safer scaling when management deems conditions right.

Competitive Landscape and Regulatory Context

QFIN’s measured stance comes at a time when Chinese regulators are maintaining close oversight of consumer lending platforms. The emphasis on compliance, transparency, and borrower protection is pushing many fintechs toward higher-quality portfolios.

In this environment, QFIN’s choice to prioritize long-term sustainability over short-term growth may be strategically sound, even if it frustrates some growth-focused investors.

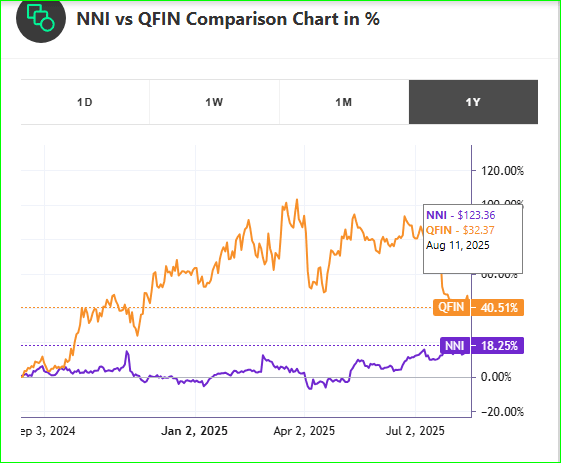

NNI vs QFIN Stock Performance Comparison

The chart comparing NNI and QFIN stock performance over the past year highlights key differences in growth and market sentiment:

- QFIN outperformed NNI significantly over the 12-month period, with a year-to-date increase of 40.51%, compared to NNI’s 18.25%.

- QFIN reached $32.37 per share on August 11, 2025, while NNI traded at $123.36 on the same date.

- Volatility trends show QFIN experienced sharper short-term movements, reflecting investor reactions to earnings updates and regulatory developments.

- Steady upward trend for QFIN demonstrates resilience in the consumer finance sector despite cautious lending practices.

- NNI showed moderate growth with less volatility, indicating stability but slower upside compared to QFIN’s dynamic performance.

- Implication for investors: QFIN’s stronger relative performance may appeal to growth-focused investors, while NNI may suit those seeking steadier returns.

Outlook for the Remainder of 2025

For the second half of the year, QFIN plans to:

- Expand partnerships with financial institutions to diversify funding.

- Continue refining borrower selection using advanced risk analytics.

- Maintain steady dividend payouts while reinvesting in technology.

While management acknowledges the competitive pressures in China’s consumer lending sector, they remain confident in delivering profitable, sustainable growth without compromising risk standards.

Conclusion

QFIN’s Q2 2025 results reflect a company walking a careful line. Earnings and revenue growth were solid, but the underlying narrative is one of restraint. In a market hungry for consumer credit, QFIN is deliberately choosing to keep risk in check, even if it means slower expansion.

For investors, the takeaway is clear: QFIN is playing the long game, betting that disciplined lending today will position it for stronger, safer growth tomorrow.

FAQ’S

QFIN reported total revenue of RMB 3.53 billion (USD 486.3 million) and net income of RMB 1.04 billion (USD 143.3 million), showing strong earnings growth compared to the previous year.

Earnings per ADS rose to USD 0.88 from USD 0.78, indicating consistent profitability growth year-over-year.

The NPL ratio stayed stable at 30.8%, reflecting disciplined credit risk management and a focus on high-quality borrowers.

Although consumer loan demand is rising, QFIN remains cautious, prioritizing strong borrower profiles over rapid expansion to maintain portfolio quality.

QFIN secures capital through diversified partnerships with banks and non-bank financial institutions, helping it optimize funding costs and sustain lending without increasing risk exposure.

Investors responded cautiously; despite solid earnings, conservative guidance limited short-term stock gains, highlighting the company’s careful risk management approach.

The company is investing in AI-driven credit scoring and borrower monitoring tools to enhance risk assessment, allowing for safer future scaling.

QFIN plans moderate loan growth, continued focus on asset quality, expansion of institutional partnerships, and steady dividends while reinvesting in technology and risk analytics.

Disclaimer

This content is made for learning only. It is not meant to give financial advice. Always check the facts yourself. Financial decisions need detailed research.

What brings you to Meyka?

Pick what interests you most and we will get you started.

I'm here to read news

Find more articles like this one

I'm here to research stocks

Ask our AI about any stock

I'm here to track my Portfolio

Get daily updates and alerts (coming March 2026)