Palantir Technologies (NASDAQ: PLTR) delivered a powerful finish to 2025, reporting $1.41 billion in revenue for Q4, well above Wall Street’s expectations and driven by surging demand for its AI‑powered software. U.S. commercial sales jumped more than 130% year‑over‑year, while government contracts grew around 66%, underlining Palantir’s growing footprint in both enterprise and federal markets.

The results on February 2, 2026 sparked renewed investor interest, highlighting how AI adoption and strategic public‑sector deals are reshaping PLTR’s growth story. With a bold outlook for 2026 and record contract values, this quarter could mark a turning point for the controversial yet compelling data analytics firm.

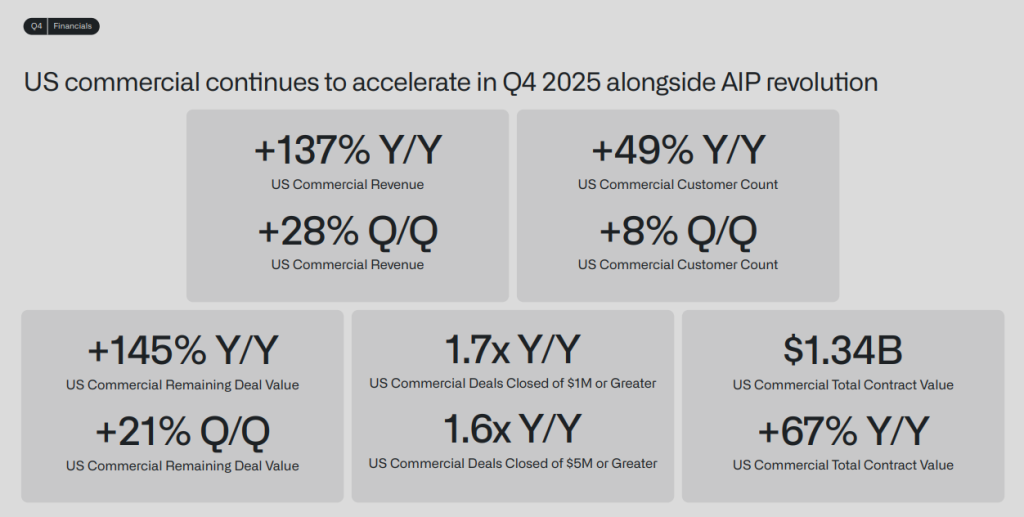

Palantir Q4 Earnings Beat: Key Financial Takeaways

Palantir Technologies (NASDAQ: PLTR) delivered a standout Q4 2025 performance that beat consensus estimates across major metrics. The company reported $1.41 billion in revenue, a 70 % year‑over‑year increase that exceeded Wall Street expectations of around $1.33 billion. Adjusted earnings per share came in at $0.25, above the expected $0.23, signaling a stronger profit trend than analysts had forecast.

The quarterly results were powered by growth in both commercial and government segments. U.S. commercial revenue surged 137 % YoY to $507 million, while U.S. government revenue increased 66 % to $570 million. These figures show broad demand for Palantir’s software across both enterprise and public sectors.

Palantir also closed a record $4.26 billion in total contract value during Q4, highlighting a healthy sales pipeline and strong enterprise adoption.

How Much Did Palantir Grow? (Revenue Details & Trends)

Revenue growth was the headline story for Q4 2025:

- Total Revenue: $1.41 billion, up 70 % YoY.

- Full‑Year 2025 Revenue: Approximately $4.48 billion, marking strong overall growth.

- Rule of 40 Score: A rare 127 % figure combining growth and profitability strength.

- U.S. Revenue: Grew 93 % YoY to $1.08 billion.

This performance reflects both the rapid uptake of Palantir’s AI and data analytics solutions and its ability to secure large multi‑year commercial and government deals.

Growth in key segments signals that Palantir is expanding beyond its traditional defense and intelligence base into mainstream enterprise AI deployment.

Why Did PLTR Outperform Earnings Expectations?

AI Adoption & Commercial Expansion

Palantir’s focus on AI‑powered platforms like AIP (Artificial Intelligence Platform) has become a central revenue driver. Strong AI adoption across industries is helping companies better analyze and act on complex datasets. This strategic tech focus has led to accelerated commercial sales and contract renewals.

Commercial trends show Palantir is no longer reliant solely on government spending. Even though government deals remain large, commercial revenue growth outpaced other segments, highlighting an industry‑wide pivot toward AI investments.

Government Contracts Remain Strong

Government spending continues to be a backbone for Palantir’s top line. Contracts with U.S. agencies, particularly in defense, intelligence, and federal analytics, gave a 66 % revenue boost in this quarter alone. These deals typically span multiple years, providing predictable recurring revenue.

2026 Guidance: What Investors Need to Know

Palantir issued bullish guidance for 2026, setting a revenue forecast of $7.182 billion to $7.198 billion, which represents around 61 % year‑over‑year growth. This projection stood well above analysts’ earlier estimates.

Additionally, Q1 2026 revenue guidance came in at $1.53 billion–$1.54 billion, implying continued momentum as the year begins.

These forecasts, if achieved, would solidify Palantir’s role as a long‑term growth stock tied to AI and government analytics demand.

PLTR Stock: Forecast & Technical Summary

What Meyka Says?

According to Meyka’s latest AI‑assisted model, PLTR received a Grade B+ with a score of 77.29, indicating a Buy suggestion based on fundamentals, sector performance, and growth outlook. The 12‑month forecast from Meyka AI is $307.23, implying nearly 95 % upside from late January 2026 levels.

Meyka also highlights valuation risks due to Palantir’s high price‑to‑earnings and price‑to‑sales multiples. Traders should use this forecast as guideposts, not guarantees, as stock moves can be volatile.

Technical Analysis Snapshot

- Overall Sentiment: Neutral, with weak trend strength.

- Momentum Indicators (RSI, MACD): Hint at mild bearish pressure, signaling short‑term sideways trading.

- Support/Resistance: Key levels around $169 and $197 per share.

- Volatility: Moderate, suggesting potential swings near earnings catalysts.

Other analysts also show mixed technical signals. TipRanks reports varied moving average cues, indicating both buy and sell conditions in different timeframes.

Risks & Challenges for PLTR Moving Forward

Investors should consider valuation and political risks. Some analysts point to Palantir’s premium valuation relative to other software companies. This means that if growth slows or guidance disappoints, the stock could face downward pressure.

Palantir’s work with government agencies, especially controversial contracts involving immigration systems, also brings public scrutiny and potential regulatory challenges. CEO Alex Karp has publicly defended the company’s technology and safeguards, but sensitive use cases can affect sentiment.

Conclusion; What This Means for Investors

Palantir’s Q4 2025 earnings beat and optimistic 2026 outlook demonstrate that the company is capitalizing on two powerful trends: enterprise AI adoption and sustained government demand. Revenue growth, record contract values, and strong forecasts offer a compelling narrative for growth‑oriented investors.

However, valuation levels, technical indicators, and regulatory headlines are potential headwinds that investors must watch. Balancing these opportunities and risks with tools like AI stock analysis (including models such as Meyka AI) can help guide smarter decisions.

For readers tracking PLTR stock, the message is clear: execution and momentum in AI and federal contracts will shape performance in 2026 and beyond.

Frequently Asked Questions (FAQs)

Palantir’s Q4 2025 revenue beat expectations due to strong AI software sales and growing government contracts. Total revenue reached $1.41 billion, reported on February 2, 2026, showing 70% growth YoY.

In Q4 2025, AI-driven commercial sales grew 137% YoY, while government contracts contributed $570 million, up 66%. The mix shows strong growth in both sectors. Data released February 2, 2026.

Palantir expects 2026 revenue of about $7.18 billion, a 61% increase. Analysts see strong AI and government demand, with a 12-month price forecast of around $307.23. Forecast released February 2, 2026.

Disclaimer:

The content shared by Meyka AI PTY LTD is solely for research and informational purposes. Meyka is not a financial advisory service, and the information provided should not be considered investment or trading advice.

What brings you to Meyka?

Pick what interests you most and we will get you started.

I'm here to read news

Find more articles like this one

I'm here to research stocks

Ask our AI about any stock

I'm here to track my Portfolio

Get daily updates and alerts (coming March 2026)