Paytm Q1 Results 2025: Fintech Giant Poised for First-Ever Profit Amidst 27% Revenue Growth

Paytm Q1 Results 2025 just made history. For the first time since its launch, the Indian fintech giant is expected to post a profit in Q1 of FY26. That’s big news, especially for a company that’s often made headlines for losses, investor doubts, and regulatory challenges.

We’re talking about a 27% jump in revenue compared to last year. That’s not just growth, it’s a strong comeback. It shows Paytm is finally finding a balance between spending smart and scaling fast.

Let’s explore what’s driving the growth, how it managed to cut costs, and what this means for its future.

Paytm: Company & Quarter Context

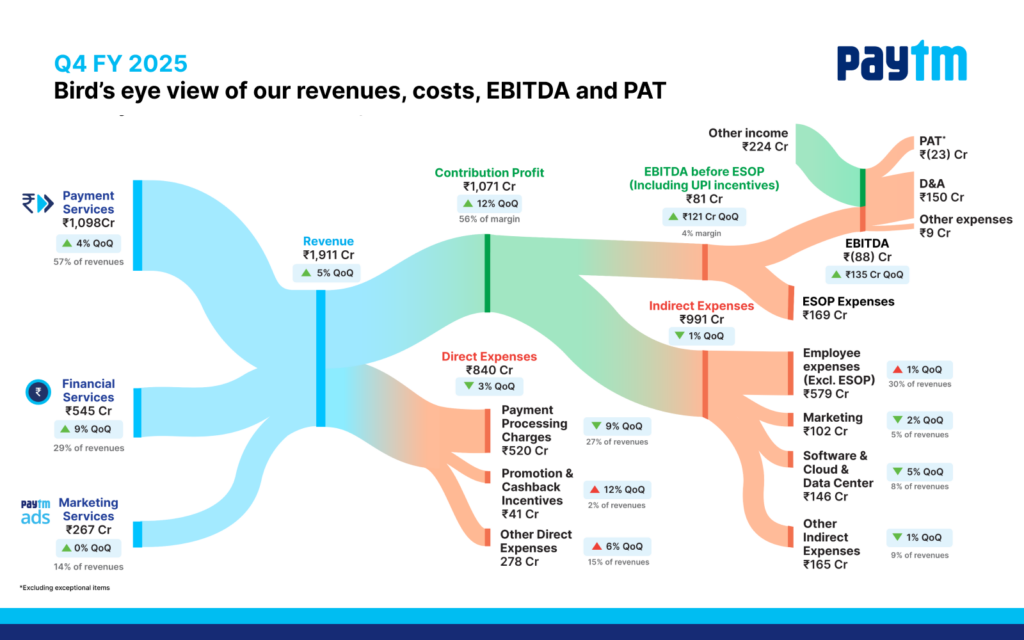

We have watched Paytm evolve from a payments startup into a full-stack fintech provider. The last three quarters have seen heavy losses, shaped by rising ESOP charges and high incentives. In Q4 FY25, Paytm reported a net loss of ₹544.6 crore, including a hefty ₹522 crore ESOP charge. With that burden easing, Q1 FY26 marks a turning point.

Revenue Growth Breakdown

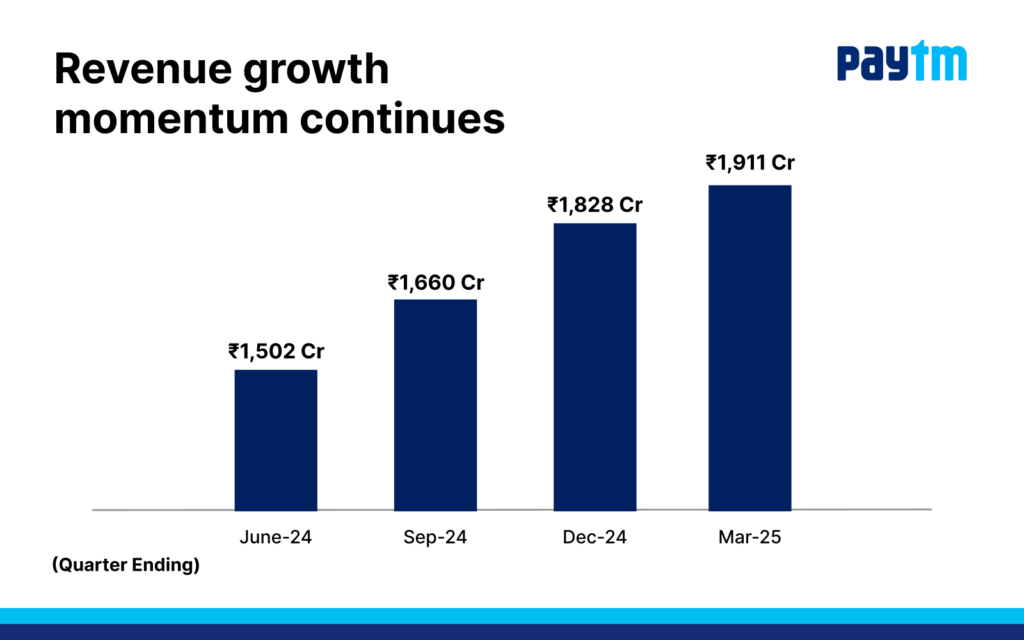

Analysts predict a solid 27 % jump in revenue to about ₹1,910 crore in Q1 FY26. On a quarter‑on‑quarter basis, growth is flat, hinting at stable core operations. Payments activity, excluding UPI incentives, likely rose ~6 % QoQ and ~21 % YoY. Meanwhile, loan disbursals are expected up ~8 % QoQ and ~23 % YoY, largely driven by merchant credit. These gains came from two key areas:

- Payment services: volume growth and increased merchant usage.

- Financial services: as loan activity rebounds, notably in merchant lending.

Profitability Leap

After years of losses, Paytm is poised to report its first-ever quarterly profit. JM Financial forecasts a ₹18.9 crore PAT, while Motilal Oswal sees a modest ₹2 crore profit. That would be a sharp turnaround from a ₹839.6 crore loss in Q1 last year.

On the EBITDA front, analysts expect a small positive result around ₹21 crore with margins near 1.1 %. This performance relies on tighter spending and reduced ESOP charges.

Key Operational Drivers

Paytm has steadily rebuilt its merchant ecosystem. The company continues a slow activation of payment devices and UPI re-onboarding partners like Yes Bank, Axis Bank, HDFC, and SBI. Merchant disbursal volumes, device usage, and active merchant count have all shown encouraging upticks.

Loan disbursements, especially to merchants, are growing. Personal lending remains cautious. Lower exposure to riskier FLDG-backed loans also eases future provisioning. This lends stability to financial services revenue.

Cost & Margin Management

Paytm’s cost base is improving. ESOP-related charges dropped sharply from ₹492 crore last quarter, down to an expected ₹75-100 crore range in Q1. Employee expenses are coming under control. However, payment processing costs jumped from ~49.8 % of payment revenue in Q4 to ~55 % in Q1, due to the lack of UPI incentives.

Overall, growth in indirect costs is manageable, but margin gains hinge on these expenses.

Analyst Perspectives & Risks

Brokerages are bullish. JM Financial views Q1 as a structural turnaround. YES Securities is optimistic on payment and lending momentum. MOFSL expects just a thin profit.

Key concerns include:

- Can margins hold up with rising processing costs?

- How will loan quality and MAS exposure evolve?

- Will UPI monetisation and regulatory clarity help sustain growth?

Market Reaction & Share Performance

Markets have shown strong confidence. Paytm shares surged 132 % over the past 12 months, reclaiming the ₹1,000+ level. The stock jumped ~3 % ahead of Q1 results.

Technical analysts point to bullish patterns such as a cup‑and‑handle and inverted head‑and‑shoulders. If momentum holds, the stock could target ₹1,700, though downside support lies near ₹950-980.

Additionally, Paytm may move to the MSCI Standard index in August. This shift could attract around $212 million in institutional investment.

Paytm Q1 Results 2025: Forward Outlook

We expect Paytm to maintain profitability into FY26. Key drivers will include:

- Continued growth in merchant lending and payments.

- Disciplined expense management.

- ESOP cost normalisation.

- Additional revenue from UPI and unutilized regulatory avenues.

However, sustained performance matters more than a single profitable quarter. Investors will watch upcoming quarters closely.

Wrap Up

Paytm Q1 Results 2025 could be a watershed moment. Paytm appears to have shifted from losses to profits thanks to steady revenue growth, cost control, and repayment discipline. The real challenge now is to keep this growth going, manage costs wisely, and make the most of new opportunities in the digital finance space.

Frequently Asked Questions (FAQs)

In 2025, Paytm’s stock traded around ₹1,000. Its total value changes with the market, but it has grown over 130% in the last year.

Paytm saw a 27% rise in revenue and is likely to post its first profit. The company is improving its costs and growing payments and loan services.

Experts say Paytm may stay profitable if it controls costs and grows safely. But risks like loan losses or rule changes can still affect its growth.

In Q1 FY2026, Paytm earned nearly ₹1,910 crore in revenue. Its net profit is expected to be between ₹2 to ₹19 crore, depending on final numbers

Disclaimer:

This content is for informational purposes only and not financial advice. Always conduct your research.

What brings you to Meyka?

Pick what interests you most and we will get you started.

I'm here to read news

Find more articles like this one

I'm here to research stocks

Ask our AI about any stock

I'm here to track my Portfolio

Get daily updates and alerts (coming March 2026)