Opendoor Technologies, also known as OPEN on the stock market, is shaking things up. It’s a company that buys and sells homes using technology. In recent months, its stock was trading around $0.61, and some analysts gave it a cautious upgrade. That means they see some good signs, but still worry about the risks.

Why the upgrade? Opendoor is changing how it does business. It’s trying a new plan that uses fewer company-owned homes and more help from real estate agents. This is a big shift from their old strategy, and it might help them save money.

Advertisement

We’re seeing a company that once burned through cash now trying to be smarter. They’ve trimmed costs and improved some numbers. But there’s still a long road ahead.

Let’s explore how Opendoor got here, what the new plan looks like, and why experts are both hopeful and careful about the future.

Background on Business Model

Opendoor pioneered the iBuying model. They make fast offers on homes, fix them, then resell for profit. This model needs lots of cash. That caused big financial losses and job cuts in 2021-2022. High interest rates mean homes don’t move fast, and Opendoor held too many homes at high cost.

Catalyst: Strategic Shift

Opendoor now leans on a new asset-light strategy. They’ve launched agent partnerships in 11 test markets.

Instead of buying every home, they refer customers to local agents. That brings in referral fees. It saves cash and cuts risk. They’re also reducing home buys by ~ 60% compared to last year. This strategy boosts profits, not just sales volumes.

Analyst Upgrade: What’s Changed

Analysts upgraded Opendoor from Sell to Hold. They note the smart pivot and better financial results.

The average price target is now about $1.15, about 90% upside. GuruFocus estimates a GF Value of $1.50, implying nearly 147% upside.

But big banks like Citi, UBS, and Deutsche Bank still see risks. They rate Opendoor a neutral Hold, and reduce targets to $0.80-$1.35.

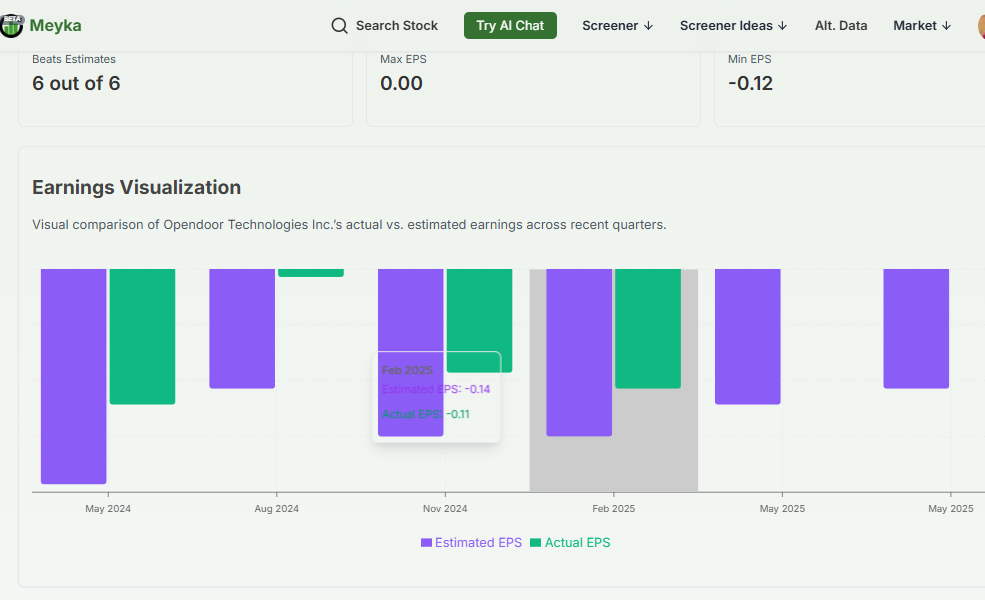

Financial Performance & Outlook

Opendoor’s Q1 2025 results surprised positively:

- Revenue: $1.2B vs estimate $1.07B

- EPS loss cut to -$0.12 vs -$0.13 estimate

- Contribution profit: $54M (4.7% margin)

- Adjusted EBITDA loss improved to $30M from $50M

They cut fixed costs by 33%. Q2 2025 outlook shows revenue of $1.45-1.525B and first positive adjusted EBITDA ($10-20M).

Risks remain: ~$2.3B debt, high mortgage rates (≈7%), and slowing housing.

Bull vs Bear Viewpoints

Bull case:

- Asset-light model raises margins

- Agent referrals replace heavy home buying

- Lower costs, leading to a profit focus

Bear case:

- Housing market may stay weak

- Debt and inventory pose dangers

- Profit may slip if Opendoor reverses course

Street opinion remains cautious. Many rate it Hold or Neutral, not yet bullish.

Strategic Outlook & Market Position

Opendoor now competes not just with iBuyers like Zillow or Redfin, but also with traditional agents.

Success depends on:

- Scaling agent partnerships

- Keeping acquisitions low and margins high

- Navigating housing cycles

If done right, Opendoor could lead again, but execution must be sharp.

Final Words

Opendoor’s cautious upgrade reflects a shift to smarter, leaner operations. We see a company trying to turn losses into profits by using agents and cutting costs.

Still, debt, housing market headwinds, and execution risk remain. The next few earnings releases and pilot market results will be key.

Advertisement

Frequently Asked Questions (FAQs)

Opendoor is down because home sales have slowed, interest rates are high, and the company has lost money. Investors are worried about future profits and risky business changes.

Opendoor may have a future if its new plan works. It is spending less money now and trying smarter ways to sell homes through agents and partners.

Opendoor might be a good stock for some, but it’s risky. It has upside, but there are still problems like debt and a weak housing market.

No, Opendoor is not profitable yet. It still loses money, but the losses are smaller now. The company hopes to make a profit in the future.

Big investors in Opendoor include BlackRock, Vanguard, and SoftBank. These are large investment firms that own shares in many different public companies.

Analysts give Opendoor a target price between $0.80 and $1.50 for 2025. The stock could go up, but it also depends on housing trends and company changes.

Disclaimer:

This content is made for learning only. It is not meant to give financial advice. Always check the facts yourself. Financial decisions need detailed research.

Advertisement

What brings you to Meyka?

Pick what interests you most and we will get you started.

I'm here to read news

Find more articles like this one

I'm here to research stocks

Ask Meyka Analyst about any stock

I'm here to track my Portfolio

Get daily updates and alerts (coming March 2026)