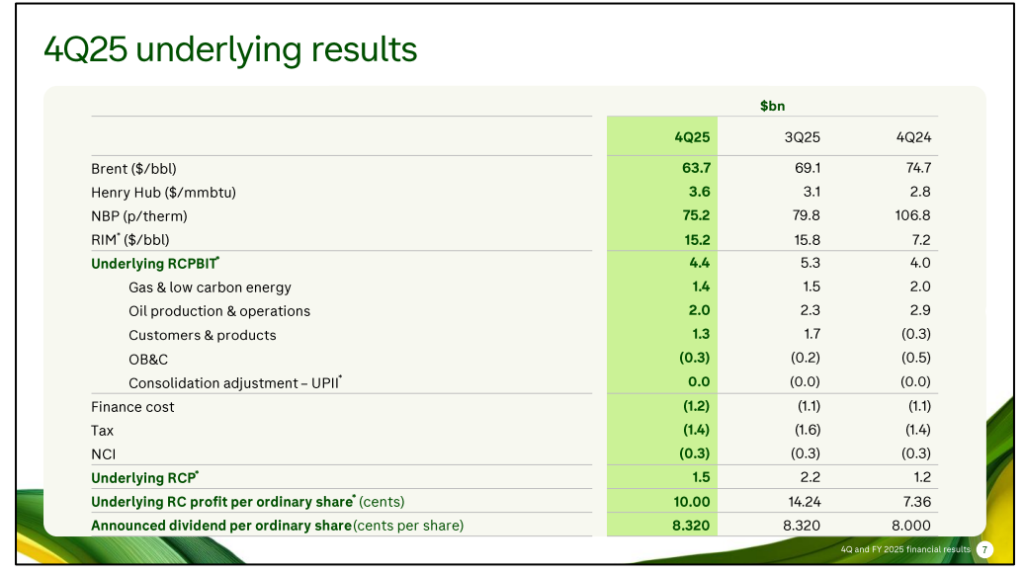

Oil prices remain volatile in early 2026, and BP sits at the center of this shift. The company suspended its share buyback programme despite posting a $1.54 billion fourth-quarter underlying replacement-cost profit that matched expectations.

This move reflects weaker oil fundamentals, falling annual profit, and rising balance-sheet caution across the energy sector. Full-year profit dropped 16% to $7.49 billion, highlighting pressure from softer crude prices.

For investors, BP now represents a transition story shaped by commodity cycles, capital discipline, and strategic refocusing toward oil and gas.

Advertisement

Oil Prices and Profit Pressure Shape BP’s Strategy

Weaker crude trends drive earnings volatility

BP’s annual profit decline stems largely from falling oil prices late in 2025, which compressed margins across upstream and trading operations. Quarterly profit also dropped 30% sequentially, confirming sensitivity to commodity swings even when year-over-year performance improved.

Oil market expectations remain cautious. Some strategists foresee Brent crude near $58 per barrel in 2026 due to persistent oversupply. This environment limits cash generation and encourages defensive capital allocation.

Investor takeaway: Commodity direction, not operational weakness, currently drives BP earnings risk.

BP: Buyback Suspension Signals Capital Discipline

Cash redirected to debt reduction and core investment

BP halted share repurchases to strengthen its balance sheet and prioritize oil-and-gas investment. The company had been spending more than $7 billion annually on buybacks, over a quarter of its cash flow.

Management now targets lower net debt and disciplined capital expenditure near $13 – $13.5 billion. This shift also follows $4 – $5 billion in energy-transition impairments tied to low-carbon assets.

Investor takeaway: BP is prioritizing financial resilience over shareholder distributions during uncertain oil cycles.

Analyst Outlook and BP Stock Positioning

Consensus ratings show limited upside

BP stock closed near $39.04 on February 6, 2026, with analysts assigning a Hold consensus rating and an average target of $40.41, implying 3.51% upside. Recent targets have ranged from $26.50 to $66.00, reflecting uncertainty about oil prices and strategy.

Some firms modestly raised targets, such as Wells Fargo, which increased its projection to $39.

Overall sentiment remains cautious despite selective optimism.

Investor takeaway: BP appears fairly valued unless oil prices strengthen materially.

Market Sentiment and Strategic Direction of BP

Investor discussion increasingly focuses on BP’s return to hydrocarbons and reduced renewable spending. Community commentary highlights strong dividend yield expectations and potential valuation upside if execution improves.

At the same time, concerns persist about long-term underperformance versus major rivals and unclear strategic consistency. Leadership transition also matters. A new CEO is scheduled to take office in April 2026, potentially reshaping capital allocation and growth priorities.

Investor takeaway: Sentiment is mixed, balancing income appeal against strategic uncertainty.

Recent Updates on BP and Oil Markets

- Fourth-quarter underlying profit reached $1.54 billion, matching forecasts.

- Share buybacks were suspended to cut debt and fund core investment.

- Net debt remains around $22.2 billion, reinforcing balance-sheet caution.

- BP recorded roughly $4 – $5 billion in low-carbon impairments.

- Capital expenditure guidance sits near $13 – $13.5 billion.

- Shares have risen about 9% in 2026, lagging major U.S. oil peers.

These developments confirm BP’s pivot toward stability and core hydrocarbons.

Conclusion

BP’s suspension of share buybacks marks a decisive response to sliding oil prices and weaker profitability.

The company is conserving cash, reducing debt, and refocusing on traditional energy production. Analysts currently see limited upside, while sentiment remains divided between income appeal and strategic uncertainty.

Future performance will depend heavily on oil price recovery, capital discipline, and leadership execution in 2026. For investors, BP now represents a defensive energy holding rather than a growth-driven opportunity.

Advertisement

Frequently Asked Questions (FAQs)

BP halted buybacks to reduce debt, preserve cash, and prioritize oil-and-gas investment during weaker oil prices.

Analysts rate BP a Hold with an average $40.41 target and about 3.51% upside.

Oil price recovery, debt reduction progress, and a new leadership strategy could reshape investor sentiment.

Disclaimer:

The content shared by Meyka AI PTY LTD is solely for research and informational purposes. Meyka is not a financial advisory service, and the information provided should not be considered investment or trading advice.

Advertisement

What brings you to Meyka?

Pick what interests you most and we will get you started.

I'm here to read news

Find more articles like this one

I'm here to research stocks

Ask our AI about any stock

I'm here to track my Portfolio

Get daily updates and alerts (coming March 2026)