NVIDIA slipped about 2.5 percent today as part of a broader chip sector pullback, highlighting the volatile tech landscape despite its strong AI-driven growth.

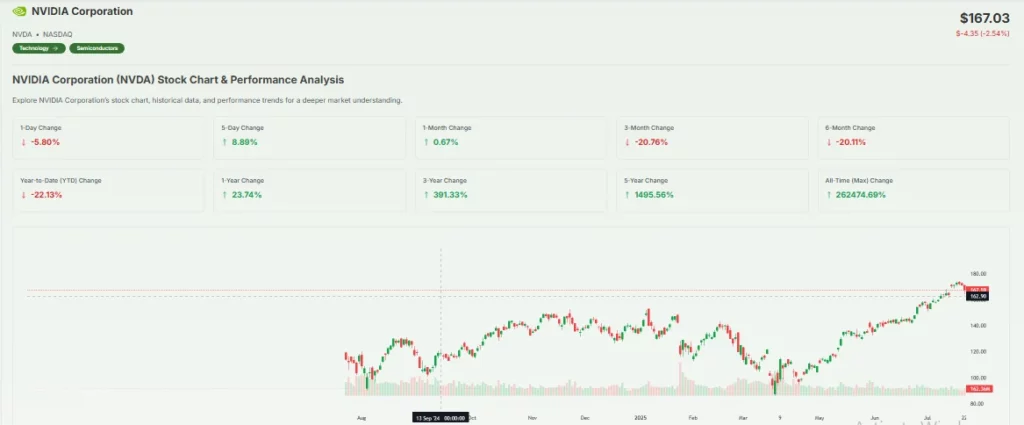

NVIDIA shares closed at $167.03 on Tuesday, falling 2.5 percent from recent highs after investors took profits following an impressive rally. With about 183 million shares traded, slightly below the 200 million‑share average, this dip appears more like a calm consolidation than a panic sell-off.

Why is this happening now, though?

Chip Sector Pullback: What’s Causing It?

The chip sector broadly declined following recent gains in semiconductor stocks like AMD and Broadcom. That industry‑wide move seems to reflect short‑term profit‑taking, not a hit to core fundamentals.

Analysts also point to macro‑level factors, including rising bond yields and mixed tech earnings, pulling investors toward less‑volatile sectors.

Peer Stock Movements and Market Sentiment

Other major semiconductor players like AMD, TSMC, and Intel also saw modest declines today. These movements indicate that the dip is sector-wide and likely driven by rotation into safer assets like utilities and treasuries.

Investor sentiment remains cautious but constructive, especially with AI and data center demand still intact.

Did the News on China Export Help NVIDIA?

Yes, but the results were mixed. NVIDIA announced it plans to resume exports of its H20 AI chips to China under a U.S. license. CEO Jensen Huang emphasized that selling compliant GPUs like RTX Pro would “accelerate recovery” of China revenue.

Still, U.S. legislators raised concerns that exporting these chips may bolster Chinese military AI. So while the resumption is positive for long‑term growth, mixed political signals may be weighing on the stock today.

Export Restrictions Still a Concern

Despite resuming shipments, the U.S. Commerce Department’s tighter export control regime remains a long-term headwind. Analysts warn that future regulatory shifts could again disrupt overseas sales.

That’s why investors are closely monitoring Washington-Beijing relations, as any escalation could immediately impact NVIDIA’s sales outlook.

Is This Pullback a Buying Opportunity?

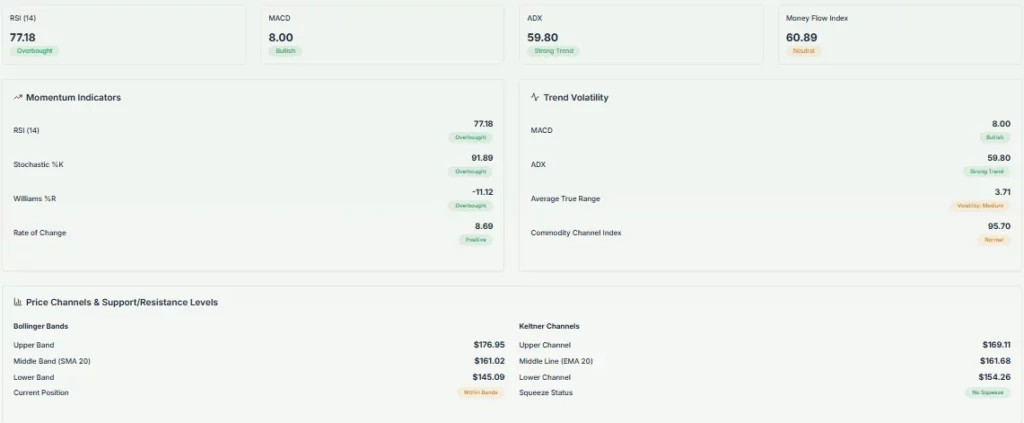

A lot depends on technical levels and earnings guidance. Technical analysts suggest support around $165, near the 200‑day average , with deeper support between $159 and $150 if the market dips further.

On the upside, many expect the AI demand narrative to resume, especially once China shipments ramp up and tech peers report strong earnings

Retail vs. Institutional Activity

Recent trading data shows that retail investors trimmed positions more aggressively than institutional investors. Mutual funds and ETFs continue to hold strong positions in NVIDIA, suggesting confidence in long-term fundamentals.

This divide often reflects short-term panic selling from smaller accounts, while larger players remain calm.

Can Broader AI Momentum Carry NVIDIA Higher?

Absolutely. Most analysts still expect strong secular growth in AI infrastructure. For example, UBS forecasts around 12 percent profit growth across global tech in 2025, fueled by AI investment. Meanwhile, NewStreet Research predicts the top AI chipmakers, including NVIDIA, will beat revenue estimates in 2026.

That shows resilience in long‑term growth, even if short‑term trading is choppy.

Product Roadmap Remains Strong

NVIDIA’s roadmap includes upcoming Blackwell GPUs and more refined AI accelerators for enterprise data centers. These chips promise improved energy efficiency and higher compute power, helping NVIDIA maintain dominance.

Such product innovation reinforces analysts’ conviction in its AI leadership through 2026 and beyond.

How Important Is the Chinese market now?

China remains a key battleground. The return of H20 deliveries could bring $10 to $15 billion in added revenue this fiscal year, boosting earnings by as much as 50 cents per share. Still, supply constraints and political scrutiny mean the full benefit may take time.

And while geopolitical tension looms, NVIDIA is working on a new compliant chip, the B30, tailored to China’s export limits.

Emerging Competitors in China

As NVIDIA adapts, Chinese firms like Biren Tech and Huawei are also accelerating their chip development efforts. While still behind in performance, they could slowly erode NVIDIA’s market share in the region.

Still, analysts believe that NVIDIA’s software ecosystem gives it a competitive edge that’s hard to replicate.

Market Reaction

“NVDA down 2.5 percent as chip sector catches a breather after tech earnings”

— @marketcompiler

This tweet captures investor sentiment perfectly: a calm pause, not a crisis.

What Should Investors Watch Next?

Upcoming triggers include:

- Earnings from NVIDIA and peers like AMD, Intel, and TSMC.

- Macro data on inflation and Fed decisions, affecting tech appetite.

- China reopening, how fast H20 and RTX Pro shipments scale.

- Institutional holdings and fund flows into tech ETFs, which could hint at early signs of bullish reversals.

These will shape whether the pullback continues or reverses sharply.

Final Take on the Chip Sector and NVIDIA

The chip sector pullback is a natural pause in a dynamic industry. While NVIDIA took a modest hit, its AI leadership, China export strategy, and analyst backing suggest this dip could be a buying window rather than a breakdown.

If you follow chip‑sector signals, watch support around $165–$150, upcoming tech earnings, and export updates for clues on the next move.

FAQ’S

Nvidia stock dropped due to broader chip sector volatility and profit-taking by investors after recent gains. Market analysts also cite stretched valuations.

Some analysts believe Nvidia is overvalued due to high price-to-earnings ratios, despite strong growth in AI and data center demand.

As of the latest data, less than 1% of Nvidia’s float is shorted, indicating low bearish sentiment among investors.

Yes, with its high market cap and trading volume, Nvidia has previously moved over $300 billion in market value within a few sessions.

Estimates vary, but some analysts forecast Nvidia could double its value in five years, driven by AI, gaming, and enterprise demand.

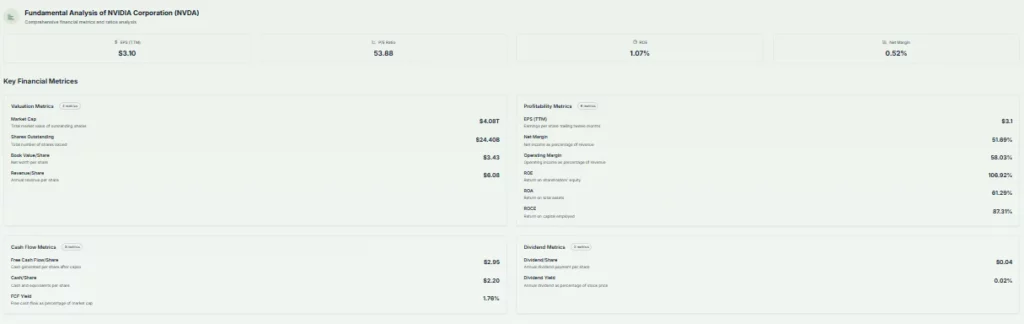

Nvidia’s long-term debt stands at around $10 billion, which is considered manageable relative to its revenue and cash reserves.

Some analysts think AMD is moderately overvalued, though it remains competitive in GPUs and CPUs against Nvidia and Intel.

It’s possible if AI and chip demand continue to surge, but Nvidia would need sustained earnings growth and market dominance.

Investing early in Nvidia could have made you a millionaire, but future gains may be slower, requiring strategic long-term holding.

Long-term estimates suggest Nvidia could be worth $5 trillion or more by 2040, assuming dominance in AI, robotics, and autonomous systems.

Disclaimer

This content is for informational purposes only and not financial advice. Always conduct your research.

What brings you to Meyka?

Pick what interests you most and we will get you started.

I'm here to read news

Find more articles like this one

I'm here to research stocks

Ask our AI about any stock

I'm here to track my Portfolio

Get daily updates and alerts (coming March 2026)