Nintendo just posted a sharp profit jump, powered by booming Switch 2 sales. In its earnings update released in February 2026, the company reported strong gains for the quarter ending December 31, 2025. Demand for the new console stayed high through the holiday season. Gamers rushed to upgrade. Investors took notice.

But the story is not all upside. Rising chip and memory costs are starting to squeeze the global gaming industry. Supply chain pressure is building again, driven by AI-related chip demand. That could test Nintendo’s margins in the months ahead.

This mix of strong sales and looming risk makes Nintendo’s outlook especially interesting right now. And it explains why markets are watching every move closely.

Nintendo’s Financial Breakout on Switch 2 Sales

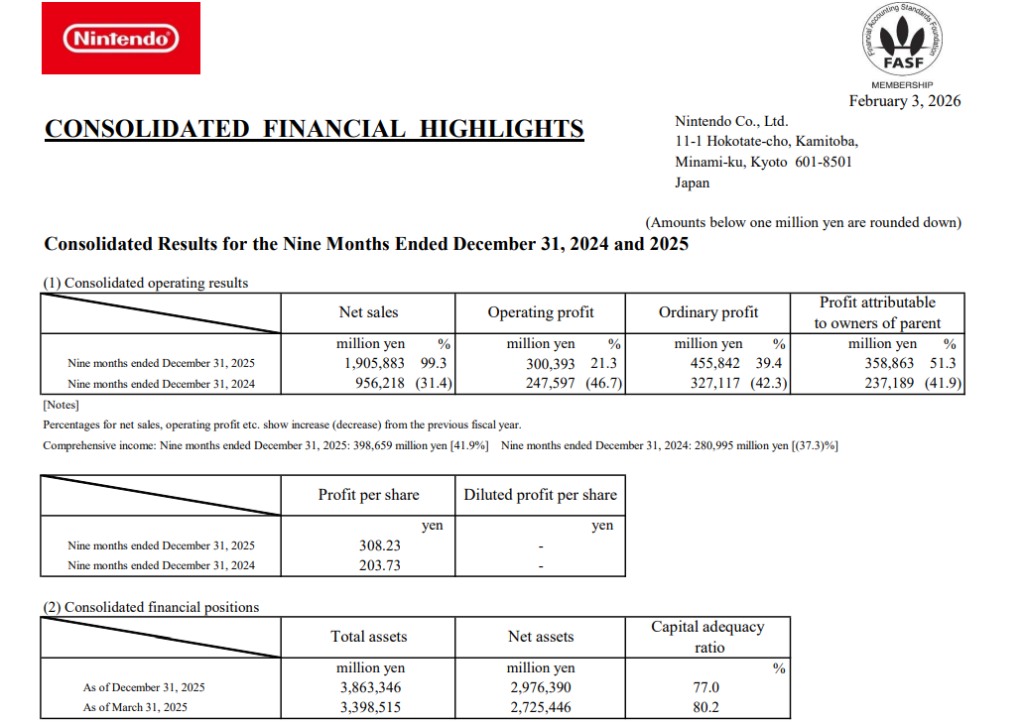

Nintendo’s latest earnings reports for fiscal 2026 show very strong results thanks to the new Switch 2 console launched on June 5, 2025. As of December 31, 2025, the company sold about 17.4 million Switch 2 units in the first nine months of the fiscal year and maintained a target of 19 million units for the full year ending March 31, 2026.

Net profit jumped more than 50 % year-over-year to ¥358.9 billion (~$2.3 billion) from April through December 2025, while revenue nearly doubled to about ¥1.9 trillion (~$12 billion). Analysts and market trackers also say the Switch 2 led US video game hardware sales in December 2025, boosting overall hardware spending even as some competitors struggled.

The strong numbers reflect both high production and consumer demand, particularly during the holiday season and amid positive software attach rates from major titles.

Chip Shortage Risks, The Dark Cloud on Nintendo’s Horizon

While Switch 2 sales have been impressive, rising semiconductor costs and global chip shortages pose a growing risk. Prices for DRAM and flash memory, essential parts of the Switch 2, soared sharply in late 2025, driven by strong demand from AI data centers and other tech sectors.

Several industry analysts say these cost increases could force price hikes for consoles down the line, potentially pushing the Switch 2’s price above its current ~$450 USD level. That matters because Nintendo historically sells hardware at or near cost, limiting its ability to absorb component price spikes without hurting profit margins.

According to some forecasting models, DRAM prices could surge over 100 % in 2026, and NAND flash costs may rise nearly 90 %, worsening cost pressures if Nintendo’s existing inventory and price contracts expire. This trend underscores how AI-driven chip demand now directly affects even gaming companies.

How Nintendo Can Navigate Ahead?

Nintendo is not standing still in the face of supply challenges. The company entered fiscal 2026 with sizable inventories and long-term component contracts, which analysts say have shielded earnings so far.

To sustain momentum and protect margins, Nintendo may:

- Boost production to meet demand before cost spikes bite.

- Secure longer supply contracts to lock in prices for key parts.

- Leverage popular games and exclusive titles to keep software sales strong and encourage hardware adoption.

Future game releases, such as anticipated entries in the Super Mario, Pokémon, and Legend of Zelda series, could further support platform engagement and help offset cost headwinds.

Conclusion: Sales Soar, Challenges Grow

Nintendo’s Switch 2 has driven strong profit growth and robust hardware demand through late 2025 and into 2026. But rising chip costs highlight that rapid tech shifts, especially from AI expansion, now affect even global gaming giants.

Nintendo’s success so far shows careful strategy and product appeal. Yet staying ahead in 2026 and beyond will require smart supply chain management, competitive pricing strategies, and fresh content to keep players engaged.

Frequently Asked Questions (FAQs)

Nintendo’s profit rose mainly because the Switch 2 console sold very well after its June 2025 launch. Sales hit over 17 million units by December 31, 2025, boosting revenue and earnings.

Chip and memory costs are rising globally, especially for RAM and storage. This may raise production costs for Switch 2 and affect future pricing or profit margins.

Stock trends are mixed. Strong Switch 2 sales support long‑term value, but investor worry over chip price pressure and game lineup has caused some share drops recently.

Disclaimer:

The content shared by Meyka AI PTY LTD is solely for research and informational purposes. Meyka is not a financial advisory service, and the information provided should not be considered investment or trading advice.

What brings you to Meyka?

Pick what interests you most and we will get you started.

I'm here to read news

Find more articles like this one

I'm here to research stocks

Ask our AI about any stock

I'm here to track my Portfolio

Get daily updates and alerts (coming March 2026)