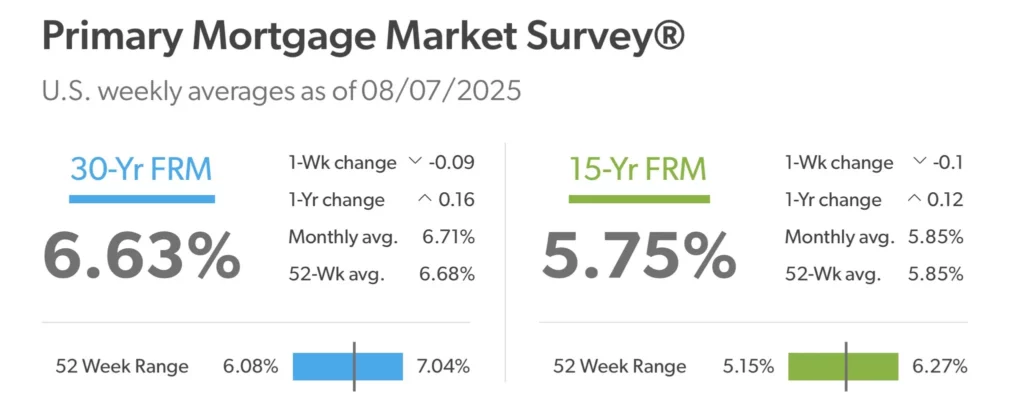

The average U S 30-year fixed mortgage rate is now around 6 .63 %, its lowest since April 2025, according to Freddie Mac data for the week ending August 7 2025. That’s a mild relief but still above the much-hoped-for 6 % mark.

Why is it not at 6 % yet?

Advertisement

Mortgage rates tend to move in step with the 10-year Treasury yield, not directly with the Fed’s short-term rate. The Federal Reserve has left its key rate unchanged recently, but Treasury yields remain sticky, keeping borrowing costs elevated.

Where Are Mortgage Rates Right Now?

As of early August 2025, the average 30-year fixed mortgage rate has eased to around 6.57 percent, a 10-month low, down from 6.74 percent at the end of July.

That decline reflects small shifts in long-term borrowing costs, but remains well above the 6 percent level many hopeful homebuyers are waiting for.

So Why Are Rates Still Above 6 Percent?

One big reason is the 10-year Treasury yield, which heavily influences mortgage pricing more than the Fed’s short-term interest rate. Though the Federal Reserve has paused rate hikes, bond markets still demand higher yields, keeping mortgage rates elevated.

Meanwhile, inflation remains sticky and economic growth is uncertain, so lenders aren’t yet confident enough to push rates below 6 percent.

Expert Forecasts on Mortgage Rates

Economists at Realtor.com and Fannie Mae expect mortgage rates to land near 6 .4 % by the end of 2025, and possibly hit 6 % in 2026. While that’s not immediate relief, it suggests a steady downward path if inflation continues to cool.

So, is there any hope for an earlier drop?

Some analysts believe softer economic data, like weaker job growth, could nudge the Fed toward rate cuts, which might help mortgage rates ease sooner.

Social Media Reaction

The discussion around mortgage rates has also been active on X, with industry experts and market watchers sharing their perspectives.

Patti Cohn wrote: “Mortgage rates are inching down, but we’re not at 6 % yet. The real impact will come when the Fed signals cuts.”

Kirk Simmon tweeted: “Buyers are watching closely. Even a small drop can mean thousands saved over a loan’s lifetime.”

LNMBUSA posted: “Mortgage rates have hit a 10 month low, but the market is still cautious. Inventory and prices remain challenges.”

TM Research added: “Expect rates to hit 6 .4 % before year end. 6 % is possible in 2026 if economic conditions align.”

What Would It Mean if Rates Hit 6 Percent?

Even shaving off a few tenths of a percent can mean real savings. For a $400,000 loan, dropping from 6.6 percent to 6 percent could save hundreds per month, and thousands over the loan term.

However, many existing homeowners have locked in sub-4 percent rates, so lower rates now may tempt only new buyers or investors; not everyone will refinance.

Affordability Reality Check

Zillow’s research suggests that for a median-income household, true affordability would require mortgage rates to drop to about 4 .43 %. In high-cost cities, even rates below 4 % would not be enough unless home prices also adjust.

What Could Help Push Rates Further Below?

Here’s what needs to happen:

- Inflation must ease decisively, giving long-term yields room to fall.

- Economic data must soften, especially in jobs and growth, to lessen rate pressure.

- Market confidence needs to improve, allowing banks to lower loan pricing.

Until these fall into place, 6 percent remains a plausible, but not immediate, target.

What Should Buyers Do Now?

If you’re looking to buy a home or refinance, experts recommend:

- Shopping around for the best mortgage quotes

- Watching the 10-year Treasury yield as a leading indicator

- Being ready to lock a rate when it dips

Even a small decrease from today’s 6 .63 % to around 6 .4 % could save thousands over the life of a loan.

Broader Housing Context

Affordability isn’t just about interest rates. Supply constraints, high home prices, and rising insurance costs all play a role.

Even if rates edge lower, long-term solutions require better housing supply, wage growth, and regulatory reforms to truly make homeownership affordable.

Final Thoughts

We’re closer to seeing 6 percent mortgage rates than we have been in a long time. Recent drops show momentum, but sustained economic cooling and yield declines are needed for that number to become reality.

For now, expect rates to hover in the mid-6 percent range through 2025. If inflation and economic jitters abate, reaching 6 percent by early 2026 becomes realistic, but it won’t happen overnight.

Advertisement

FAQ’S

Experts forecast rates could reach 6 % in 2026 if inflation cools and the Fed cuts rates.

Historically, 7 % is higher than average but lower than past peaks like in the 1980s.

Most projections suggest around 6 .4 % by the end of 2025, but not much lower.

A 5-year fix offers longer stability, while a 2-year fix can be cheaper initially but may face higher rates later.

A 3-year term provides flexibility, while a 5-year term gives longer rate security.

If rates are rising, locking today can protect you from future increases.

Yes, if you want lower monthly payments, but you’ll pay more interest over time.

You may miss out on lower rates if the market drops, and early repayment can have penalties.

It depends on your budget, shorter terms save interest, longer terms lower monthly payments.

Disclaimer

This is for information only, not financial advice. Always do your research.

Advertisement

What brings you to Meyka?

Pick what interests you most and we will get you started.

I'm here to read news

Find more articles like this one

I'm here to research stocks

Ask our AI about any stock

I'm here to track my Portfolio

Get daily updates and alerts (coming March 2026)