Mortgage markets are shifting under the weight of fresh 2026 forecasts. Experts now see a temporary slowdown in mortgage and business lending this year, even as banks adapt to changing credit demand and economic uncertainty.

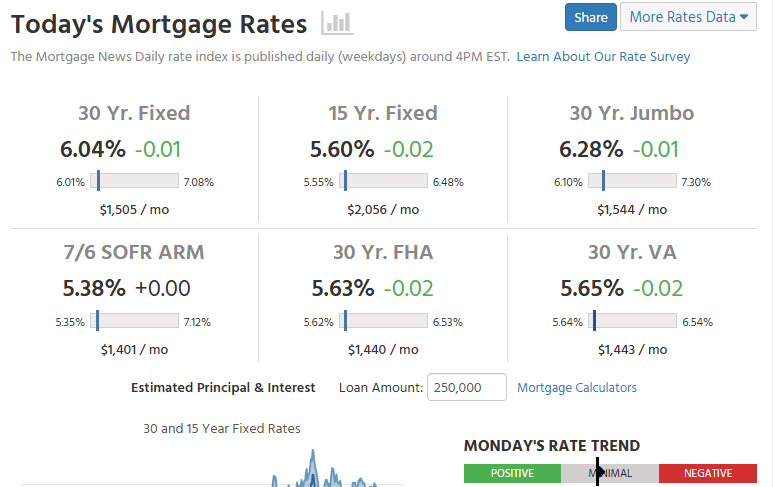

Recent data shows mortgage rates hovering in the low to mid‑6% range, offering modest relief compared with 2025 highs but still challenging for many homebuyers. Meanwhile, pending home sales and overall lending growth are softer than expected, prompting lenders and analysts alike to brace for a cautious year ahead.

Advertisement

Let’s unpack what’s driving these shifts and why this slowdown may be short‑lived.

Why is a Mortgage Slowdown Forecast in 2026?

In 2026, experts expect mortgage lending and overall bank lending to slow down compared to recent years. A major economic forecast shows total bank lending growth slowing in 2026, including mortgages, with stronger growth returning in 2027 and 2028. This suggests a one‑year lull in credit demand and lending activity. Slower lending can dampen home sales and refinancing activity, even if rates ease only modestly.

A temporary slowdown reflects broader economic uncertainty and ongoing caution among consumers and lenders. Both home and business borrowers are waiting on clearer signals from job markets, inflation, and interest policies before making big financial decisions.

Mortgage Rate Outlook for 2026 – What Data Says?

What Will Mortgage Rates Look Like in 2026?

Mortgage rates are expected to remain near the 6% range throughout 2026. Major housing forecasts show average 30‑year fixed rates hovering around 6.3% for the year, with little dramatic drop. This level is below some of the highs seen in 2025 but still high compared to earlier years.

Some analysts believe mortgage rates could dip close to 5.9% later in the year if inflation falls and central banks cut rates. Others remain cautious, saying rates may stay at or slightly above 6% for most of the year.

Why are Rates Staying Elevated?

Mortgage rates are influenced by wider interest rate policy, bond markets, and inflation. Even with inflation cooling, central banks are cautious. That keeps borrowing costs from dropping sharply. This slower shift in policy can keep mortgage rates elevated through much of 2026, limiting how much buyers benefit from lower costs.

Housing Market Signals – Demand, Sales, and Inventory

Are Home Sales Rising or Falling in Early 2026?

Early 2026 housing data shows mixed signals on sales activity. Pending home sales, which reflect signed contracts that haven’t closed yet, dipped slightly in January. This drop suggests slower buying activity, even as mortgage rates edge lower.

At the same time, the number of new and active listings has been rising in some markets, giving buyers more choices. But the slow pace of sales means inventory is still below long‑term norms in many areas.

What’s Happening with Inventory and Prices?

Inventory levels increased year over year, marking many months of gains. Yet this rise has lost momentum in recent months. Home prices are mostly flat nationally, with some local markets diverging.

Prices staying stable and inventory slowly improving can signal better affordability over time, but tight supply continues to challenge buyers in early 2026.

What 2026 Trends Mean for Homebuyers & Investors?

What Should Homebuyers Expect in 2026?

Homebuyers entering the market in 2026 may find more choices and slightly lower rates than in late 2025. But affordability remains a key challenge, as mortgage rates still sit above historical lows. Prospective buyers should:

- Compare loan offers from multiple lenders.

- Consider plans for rate locks if rates tick up.

- Watch market data weekly rather than waiting months for trends.

Tools like AI analysis platforms can also help buyers analyze broader economic signals that affect interest rates and housing markets.

Slight improvements in affordability could encourage more buyers in the spring and summer months if mortgage rates continue their gradual trend downward.

How Should Real Estate Investors Think About 2026?

For investors, 2026 might be a year of strategic opportunities. Slow lending and moderate rate declines can stabilize pricing and open up bargains in markets with rising inventory. It also means:

- Rental property appeal could stay strong if buyers delay purchases.

- Long‑term investors may benefit from steadier price trends.

- Short‑term flips might face slower demand due to higher borrowing costs.

Understanding regional variances is important. Some areas may bounce back faster, while others stay slow until mid‑year.

Final Words

The mortgage market in 2026 is evolving slowly. Both home loan rates and pending sales show cautious improvement, but challenges remain. Mortgage rates are expected to stay near 6%, while home sales and inventory shift unevenly across regions. Market players should be prepared for continued slow growth early in the year, with the chance of stronger activity later if affordability improves and buyer confidence returns.

For homebuyers and investors, staying informed on rate changes, sales data, and inventory trends will be critical. As the year unfolds, 2026 could be a time of measured gains rather than dramatic swings in the housing market.

Advertisement

Frequently Asked Questions (FAQs)

Mortgage rates may drop slightly in 2026. Experts expect them around 5.9-6% if inflation cools and central banks adjust rates. Rates will stay high compared to earlier years.

Mortgage lending is slowing due to higher rates, tighter affordability, and economic uncertainty. Banks are cautious. Homebuyers and businesses are borrowing less until the market becomes clearer.

2026 could be okay for buyers. Mortgage rates are stable near 6%, and housing inventory is rising. Careful planning and comparing lenders can help make smart decisions.

Disclaimer:

The content shared by Meyka AI PTY LTD is solely for research and informational purposes. Meyka is not a financial advisory service, and the information provided should not be considered investment or trading advice.

Advertisement

What brings you to Meyka?

Pick what interests you most and we will get you started.

I'm here to read news

Find more articles like this one

I'm here to research stocks

Ask our AI about any stock

I'm here to track my Portfolio

Get daily updates and alerts (coming March 2026)