Morgan Stanley: The Software Stock to Buy and the One to Skip in the $45B Market

The global software market is booming. It’s expected to grow past $45 billion, and companies are racing to lead the pack. From cloud apps to AI tools, the tech world is changing fast, and investors are watching closely. Big banks like Morgan Stanley help guide people through all this noise. They study the market, break down company data, and tell us which software stocks might be winners or which ones to avoid.

Let’s look at one software stock they believe is worth buying and one they suggest we skip for now.

Advertisement

The State of the Software Market

The software market is riding a wave right now. It’s above $45 billion and climbing fast. Investors are drawn by AI, cloud computing, and cybersecurity. These areas are growing at breakneck speed. We see strong demand from businesses that want better tools to work smarter and safer. That growth draws more investors. And that growth fuels more innovation.

At the same time, overall stock valuations feel high. Big gains in tech have driven many software names to trade at lofty multiples. We must weigh growth potential against steep prices. Morgan warns this is shaping up as a stock picker’s market, not a “buy anything” market.

Morgan Stanley’s Evaluation Criteria

Stanley looks at several key factors when grading software stocks. First, they check revenue growth and earnings potential. Second, they review how sticky the customer base is and how easy it is to scale. Next, they assess the company’s moat, its edge over competitors. And last, they check for execution power driven by leadership and strategy.

They also weigh valuation, especially thanks to recent market highs. When bond yields passed 4.5%, Morgan Stanley argued that stock performance will lean more heavily on earnings now not hype.

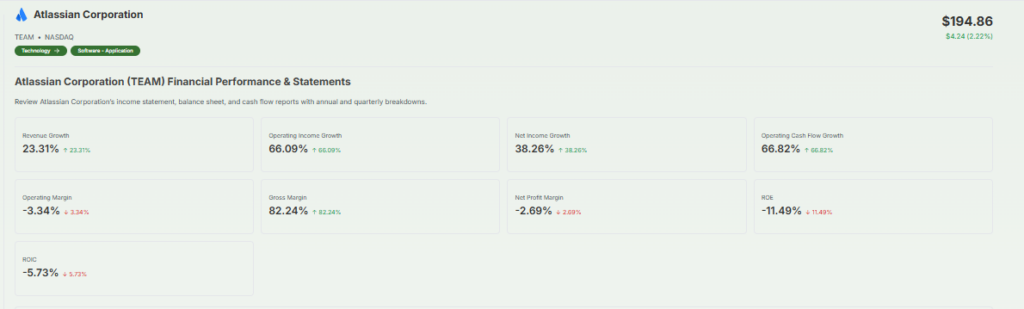

The Stock to Buy: Atlassian

One company, Morgan Stanley, is bullish on Atlassian (TEAM). The firm praised Atlassian as a top pick for 2025. Here’s why we agree:

Atlassian delivers tools for teams like Jira and Confluence. These tools are essential for project work. That makes them sticky. It also gives the company strong annual recurring revenue (ARR). And they keep adding AI features to work smarter.

In early 2025, demand for Atlassian’s software had a big boost. That aligns with Morgan Stanley’s view of a software cycle powered by AI and cloud adoption. As teams roll out AI workflows, tools like theirs get more users and deeper usage.

Valuation support is also strong. Operating margins are healthy. Cash flow is solid. Plus, they provide analyst price targets higher than current levels.

That means Atlassian matches Morgan Stanley’s core criteria: scalable growth, strong tech moat, fair valuation, and execution.

The Stock to Skip: CrowdStrike (or Palantir)

Morgan Stanley recently downgraded CrowdStrike (CRWD) from strong buy to “Equal Weight.” The view? The stock has surged too far, too fast. Here’s the breakdown:

CrowdStrike has strong free cash flow at about 25% annually. It’s a leader in cybersecurity. But it trades at about 21 times 2026 sales, far above the 12x average for large-cap software. That high multiple leaves little room for error. Morgan Stanley believes much of the expected growth is already priced into the stock.

Alternatively, analysts also flagged Palantir (PLTR) as overvalued. They say growth expectations and valuation are already baked in. That left them with an Underweight rating.

Bottom line: Either CrowdStrike or Palantir fits the “skip” slot here. These are companies with strong business, but sky-high valuations. That means we’d rather wait for a better entry point.

Market Reactions & Investor Takeaways

CrowdStrike’s downgrade did shift sentiment. Shares dipped around $477 recently, after a 39% jump year-to-date. Palantir, likewise, fell 5% following Morgan Stanley’s warning. These moves show how powerful analyst calls can be in the market.

For us investors, the lesson is clear: Even strong companies can be poor buys at the wrong time. We need to watch metrics like free cash flow, ARR, growth trends, and valuation closely.

Morgan Stanley’s analysis reminds us to pick stocks smartly, not chase all on-trend names.

Wrap Up

Morgan Stanley gives us a story of two sides in the $45B software market. We have one stock, Atlassian, with strong growth, recurring revenue, and reasonable valuation. And we have another CrowdStrike (or Palantir) with solid fundamentals but stretched prices.

The key lesson? Focus on quality and value, not just hype. When we invest, let’s follow Morgan Stanley’s lead: dig into fundamentals, evaluate valuations, and time our entry wisely. That is how smart money wins big.

Advertisement

Frequently Asked Questions (FAQs)

Morgan Stanley is a strong bank with steady earnings. Some experts like it for long-term growth, but others worry about market risks. It depends on your goals.

Morgan Stanley recommends stocks like Atlassian, Microsoft, and ServiceNow. These companies show strong growth, good profits, and future potential in the cloud and AI markets.

Yes, Morgan Stanley is slowly turning more positive on US stocks in 2025. They see better earnings ahead, but still warn about high prices and interest rates.

Morgan Stanley bought the trading platform E*TRADE in 2020. This helped them serve more everyday investors and expand their online tools and services.

Disclaimer

This content is for informational purposes only and not financial advice. Always conduct your research.

Advertisement

What brings you to Meyka?

Pick what interests you most and we will get you started.

I'm here to read news

Find more articles like this one

I'm here to research stocks

Ask Meyka Analyst about any stock

I'm here to track my Portfolio

Get daily updates and alerts (coming March 2026)