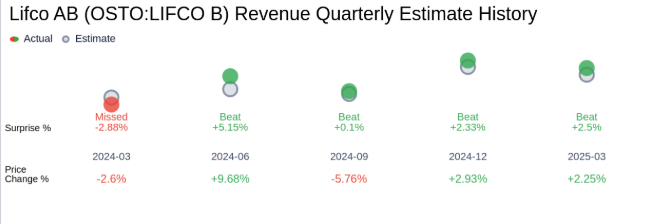

Lifco shares just took a sharp 9% hit. Why? Its second-quarter profit dropped more than expected. The reason: weaker margins.

Lifco is a Swedish company known for buying and running small and medium-sized businesses. It works across three key areas: Dental, Demolition & Tools, and Systems Solutions. Over the years, Lifco has been a favorite among investors. Its steady growth and smart acquisitions kept the stock strong.

But now, things look a bit shaky. In Q2 2025, Lifco reported lower profits even though sales were stable. That scared the market. Investors sold off their shares, and the stock fell hard.

Let’s look at Lifco’s earnings, rising costs, and why its margins are under pressure. We’ll also explore what this means for the company’s future and for investors.

About Lifco AB

Lifco is a Swedish group. It focuses on buying and growing niche businesses. It works in three main areas: Dental, Demolition & Tools, and Systems Solutions. By end-2024, Lifco included 257 companies in 34 countries and had an EBITA margin of 22.6% on SEK 26.1 billion in sales. It has a long-term mindset and a decentralized setup.

Q2 Earnings Report Highlights

In Q2, Lifco saw net sales grow 3.2% to SEK 6.94 billion. Acquisitions added 7.2%, while organic sales were just 0.5%. Currency effects cut sales by 4.4%.

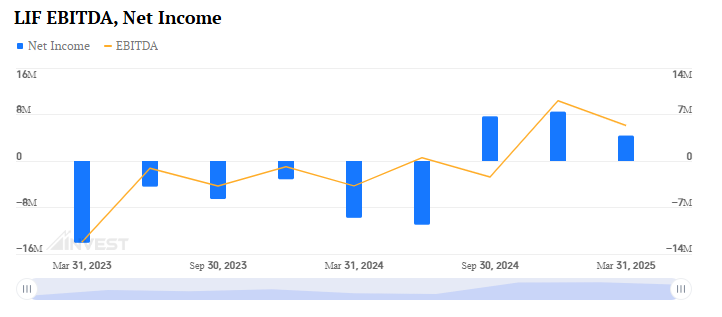

EBITA fell 2.8% to SEK 1.56 billion. The margin shrank to 22.5%, from 23.9% a year ago.

Net profit was SEK 880 million, down 3.8% from SEK 914 million last year.

Operating cash flow dropped 8.5% to SEK 971 million, and profit before tax fell 4.3% to SEK 1.18 billion.

Causes Behind the Weaker Margins

Margins weakened due to several reasons.

First, the product mix shifted. Lifco sold more low-margin items in key divisions.

Second, Systems Solutions saw sliding organic growth. Its contract manufacturing unit billed extra for surplus materials, cutting profit.

Third, currency tailwinds were missing, given a 4.4% negative exchange-rate effect.

Lifco Shares: Stock Market Reaction

The market responded fast. Lifco shares plunged about 9% in one day.

The drop followed missed EBITA and profit forecasts. Analysts pointed out weak margins and disappointing organic growth.

Trading volume spiked as investors sold. The stock’s valuation now looks more cautious.

Segment‑Wise Breakdown

Dental: Half-year sales rose to SEK 3.24 billion, but Q2 sales dropped 2.4%. EBITA fell 5.4%, hurt by the later Easter and weaker demand.

Demolition & Tools: Half-year sales jumped 5.5% to SEK 3.41 billion. EBITA improved 13.7% to SEK 861 million. But Q2 EBITA dipped 1.7% from product mix issues.

Systems Solutions: H1 sales grew 14.8% to SEK 7.22 billion, but organic growth was flat. EBITA margin slipped to 22.2%, down from 24.3%.

Long‑Term Fundamentals and Strategy

We see Lifco’s acquisition model still working. In H1, it added seven companies, adding about SEK 800 million in sales.

Net debt rose modestly to SEK 12.84 billion (1.3 × EBITDA). It remains within the 3× target.

But organic sales slowed to 0.5%. That shows weaker pricing power and demand.

We want to see more focus on portfolio mix, cost control, and organic growth. It’s still early to tell if acquisitions will offset margin hits.

Lifco Shares: Analyst Views and Market Outlook

Analysts revised estimates. Full-year 2025 revenue forecasts fell from SEK 28.99 billion to SEK 27.82 billion. EPS estimates dropped from SEK 8.43 to SEK 8.00.

Valuation is now under pressure. P/E stands at about 52.7×, making it one of the highest in its peer group.

The consensus remains “Hold”. Price targets range around SEK 345, below current levels.

Analysts say Lifco must prove it can reverse margins and grow organically.

What Does It Mean for Investors?

We think this Q2 miss is a warning sign. It shows Lifco needs to sharpen its mix and pricing.

If margins stay under pressure, the stock might fall further. But if they improve, this dip could be a chance to buy.

Risks to monitor: margins, organic growth, debt levels, and integration success.

For long-term investors, this might be a moment to weigh patience. For others, it’s a chance to reassess exposure.

Wrap Up

Lifco’s Q2 shows slower organic growth and squeezed margins. Its acquisition model still works, but profit is under strain. Investors are watching closely for margin recovery and stronger internal growth. Until then, we see caution. But the path ahead is clear: fix the mix, improve pricing, and grow organically or face continued pressure.

Frequently Asked Questions (FAQs)

Lifco AB buys and grows small to mid‑sized businesses. It works in three areas: dental supplies, demolition tools, and systems solutions. It operates globally in over 30 countries.

Lifco includes around 257 companies as of mid‑2025. These firms operate across Sweden, Europe, North America, and Asia.

In the last twelve months, Lifco earned about €2.49 billion (or SEK 26 billion). Its revenue grew approximately 6% year-over-year.

We can open a stock account with a broker. Then, search for the ticker “LIFCO‑B.ST” on Nasdaq Stockholm and place a buy order.

Lifco’s P/E ratio is high, around 50-52×. This is above its average of about 44× and its peers in its group.

Disclaimer:

This content is for informational purposes only and not financial advice. Always conduct your research.

What brings you to Meyka?

Pick what interests you most and we will get you started.

I'm here to read news

Find more articles like this one

I'm here to research stocks

Ask our AI about any stock

I'm here to track my Portfolio

Get daily updates and alerts (coming March 2026)