Right now, many lenders are cutting home loan rates. They are doing this because they expect the Reserve Bank of Australia, or RBA, to lower or cut interest rate soon. When the RBA changes its rates, it affects how much we pay on loans.

Lower interest rates mean cheaper loans. This is good news for anyone looking to buy a home or refinance. But why do lenders act before the RBA makes its move? And how will this affect us as borrowers?

Advertisement

Let’sl explore what is happening with home loan rates, why lenders are making these changes now, and what it means for people like us.

Background: What is the RBA Interest Rate?

The Reserve Bank of Australia (RBA) sets the cash rate. This is the interest rate banks pay to borrow money overnight. The cash rate affects how much banks charge us for loans, like home loans.

When the RBA changes the cash rate, banks usually change their interest rates too. If the RBA raises the cash rate, banks may raise home loan rates. This makes borrowing more expensive. If the RBA lowers the cash rate, banks may lower their rates. This makes loans cheaper.

In the past, the RBA has changed the cash rate to control the economy. In the late 1980s, the cash rate was very high at 17% to fight inflation.

Recently, in 2025, the RBA cut the cash rate to 4.10%. This was to help the economy grow as inflation eased and the world faced uncertainties.

Why Lenders are Cutting Home Loan Rates Now

Lenders are cutting home loan rates because they expect the RBA to lower interest rates soon. They want to attract borrowers before the official change.

Inflation is going down, and the economy is growing slower. This makes people think the RBA will cut rates more. Because of this, lenders lower their rates to stay competitive.

Lenders also want to keep their current customers and get new ones. They do this by offering better loan deals.

Impact on Home Buyers and Borrowers

For home buyers, lower interest rates mean reduced borrowing costs, making home ownership more affordable.

Existing homeowners might consider refinancing their loans to take advantage of lower or interest rate cut, potentially saving money on monthly repayments.

However, borrowers should be cautious. Lower rates are beneficial, but they might not last long. It’s essential to plan for potential rate increases in the future.

Economic Implications of the RBA Interest Rate Cut

The RBA cuts Interest rates to help the economy grow. Cheaper loans make people spend and invest more.

Lower rates can help the housing market too. More people can afford to buy homes. This raises demand and might push up house prices.

But there are risks. If borrowing is too easy, people may take on too much debt. This can make the housing market too hot and cause problems.

Future Outlook: What Borrowers Should Expect

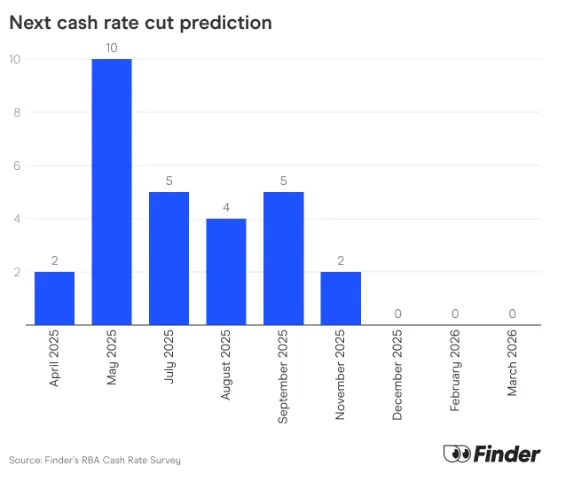

Economists predict that the RBA will cut the cash rate by 25 basis points to 3.85% at its next meeting. Further cuts are anticipated later in the year, possibly bringing the rate below 3%.

Lenders are likely to continue adjusting their rates in response to these changes. Borrowers should stay informed about rate movements and consider refinancing options to secure the best deals.

Wrap Up

Lenders are lowering home loan rates because they expect the RBA to cut interest rates soon. They want to attract and keep borrowers. This is good news for home buyers and homeowners. They can borrow money at lower costs. But it’s important to watch for future rate changes.

Planning ahead is key. Staying informed and getting expert advice can help you handle these changes well.

Advertisement

Frequently Asked Questions (FAQs)

The RBA cuts interest rates to help the economy grow. Cheaper loans make people spend and invest more.

When interest rates go down, monthly mortgage payments get smaller. This makes home loans easier to afford.

When banks cut interest rates, borrowing becomes cheaper, potentially increasing demand for loans and stimulating economic activity.

As of May 16, 2025, the RBA has not yet cut interest rates but is expected to do so on May 20, 2025.

Disclaimer:

This content is for informational purposes only and not financial advice. Always conduct your research.

Advertisement

What brings you to Meyka?

Pick what interests you most and we will get you started.

I'm here to read news

Find more articles like this one

I'm here to research stocks

Ask Meyka Analyst about any stock

I'm here to track my Portfolio

Get daily updates and alerts (coming March 2026)