Kaynes Technology has delivered strong financial momentum in 9MFY25 and Q3FY26, reinforcing its position in India’s fast-growing electronics manufacturing services sector. Revenue growth, rising profitability, and a robust order book highlight improving execution visibility. Yet, past stock volatility and valuation concerns keep investors cautious.

This balance between operational strength and market skepticism defines the current investment narrative around Kaynes Technology. Understanding the latest earnings data, growth drivers, and sentiment signals helps investors assess whether the company’s financial acceleration can translate into sustained shareholder returns.

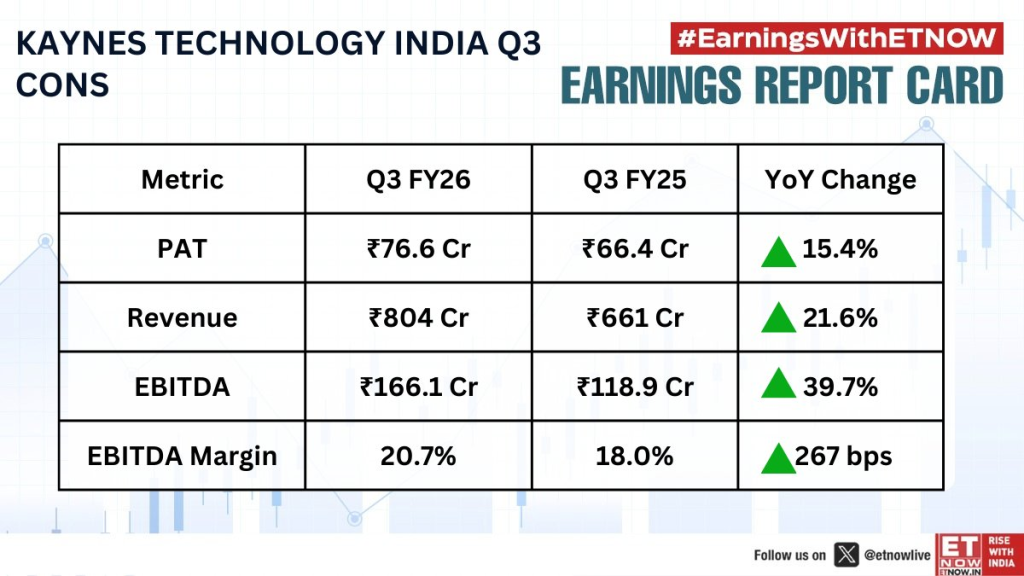

Financial Performance Strengthens Across 9MFY25 and Q3FY26

Revenue, EBITDA, and Profit Growth

Kaynes Technology reported ₹23,837 million in revenue for 9MFY25, up 37 percent year-over-year, while PAT rose 54 percent to ₹2,726 million. EBITDA climbed 55 percent to ₹3,778 million, confirming margin resilience during expansion.

For Q3FY26, revenue stood at ₹8,040 million, increasing 22 percent YoY, and PAT reached ₹766 million, up 15 percent. These numbers show consistent scaling rather than one-time gains. Rising profitability alongside revenue growth signals improving operating leverage, a critical indicator for EMS companies pursuing long-term margin expansion.

Order Book Visibility and Growth Trajectory

Strong Pipeline Supports Future Revenue

Kaynes Technology’s order book reached ₹90,722 million, providing multi-year revenue visibility and supporting capacity expansion plans.

Earlier disclosures also showed strong execution momentum, with order backlog rising from ₹3,798 crore to ₹6,047 crore YoY and EBITDA margin improving to 14.2 percent in Q3FY25.

This sustained backlog expansion suggests structural demand from sectors such as EVs, aerospace, and industrial electronics. For investors, strong order visibility reduces downside risk tied to cyclical slowdowns.

Stock Volatility, Guidance Cuts, and Valuation Debate

Market Reactions Remain Mixed

Despite profit growth, Kaynes Technology previously cut FY25 revenue guidance to ₹2,800 crore from ₹3,000 crore, triggering a sharp share-price decline of more than 19 percent.

The stock has also experienced deep corrections, falling 46 percent from its record high of ₹7,824.95 after a period of extraordinary gains.

Valuation metrics remain elevated, with TTM EPS at ₹45.8 and P/E near 129.8×, reflecting strong growth expectations already priced into the stock.

This tension between rapid earnings growth and premium valuation continues to shape investor sentiment toward Kaynes Technology.

Market Sentiment and Investor Discussion

Retail investors remain divided on Kaynes Technology’s outlook. Some highlight strong fundamentals, order visibility, and semiconductor-linked expansion as long-term positives. Others question execution capability and valuation sustainability after sharp price swings.

This mixed sentiment reflects a classic growth-stock dilemma. Strong business momentum attracts long-term investors, while volatility encourages short-term caution.

Recent Updates on Kaynes Technology

- Kaynes Technology reported 37 percent revenue growth and 54 percent PAT growth in 9MFY25, confirming strong operational scaling.

- Q3FY26 revenue rose 22 percent YoY, while profit increased 15 percent, showing continued quarterly momentum.

- The company’s order book expanded to ₹90,722 million, strengthening forward revenue visibility.

- Historically, execution delays forced a reduction in FY25 revenue guidance to ₹2,800 crore, which pressured the share price.

- The stock has shown extreme volatility, including a 46 percent fall from peak levels after rapid earlier gains.

- Elevated valuation ratios, including P/E near 129.8×, indicate strong growth expectations embedded in pricing.

Together, these updates show improving fundamentals but persistent valuation and sentiment risks.

Conclusion

Kaynes Technology’s 9MFY25 and Q3FY26 results confirm strong financial momentum, driven by rising revenue, expanding margins, and a record order book. These fundamentals support a long-term growth narrative tied to India’s electronics and semiconductor ecosystem. However, valuation premiums, past guidance cuts, and sharp stock volatility keep investor sentiment cautious.

For investors, the key question is sustainability. If execution remains consistent and margins continue expanding, Kaynes Technology could justify premium pricing. Without sustained delivery, volatility may persist. Careful monitoring of order execution, earnings growth, and valuation normalization remains essential before making long-term allocation decisions.

Frequently Asked Questions (FAQs)

Revenue reached ₹23,837 million, and PAT rose to ₹2,726 million, reflecting 37 percent and 54 percent year-over-year growth respectively.

Q3FY26 revenue was ₹8,040 million, and PAT stood at ₹766 million, showing continued year-over-year growth momentum.

Guidance cuts, execution delays, and high valuation multiples contributed to sharp price corrections despite profit growth.

A ₹90,722 million order book, expanding margins, and strong EMS sector demand provide structural growth visibility.

Disclaimer:

The content shared by Meyka AI PTY LTD is solely for research and informational purposes. Meyka is not a financial advisory service, and the information provided should not be considered investment or trading advice.

What brings you to Meyka?

Pick what interests you most and we will get you started.

I'm here to read news

Find more articles like this one

I'm here to research stocks

Ask our AI about any stock

I'm here to track my Portfolio

Get daily updates and alerts (coming March 2026)