Investor Delight: Andrews Sykes Group’s 43% Three-Year Return Highlights Solid Performance

Did you know that Andrews Sykes Group has delivered a 43% return over the past three years? That’s not something we see every day in today’s uncertain market. While many companies struggled, Andrews Sykes stayed strong and steady. It’s a name not often in the spotlight, but its quiet success has caught the attention of smart investors.

Let’s find out how this company achieved such impressive growth. We’ll look at what makes it tick, what drives its profits, and what it offers to long-term investors like us.

Let’s break it down and see why Andrews Sykes is becoming a hidden gem in the investment world.

Company Overview

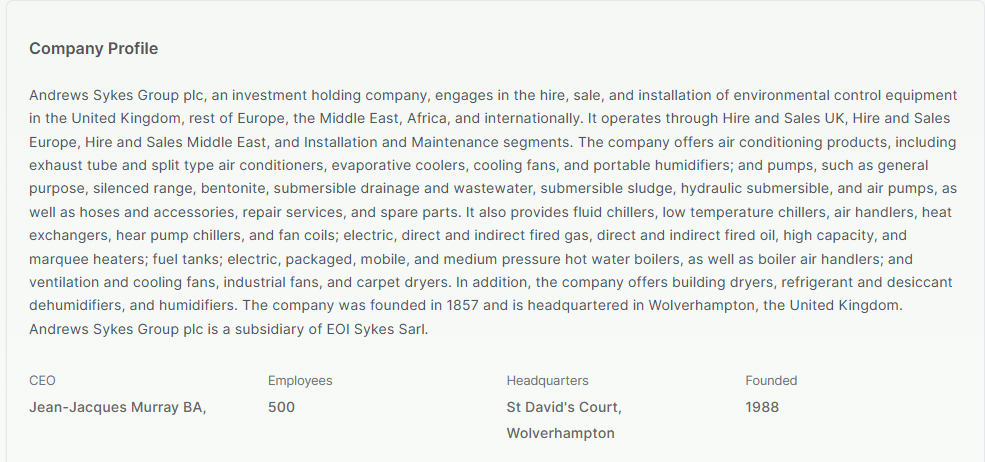

We see Andrews Sykes Group as a specialist hire company. It started in 1857 and began as a pump specialist along the River Thames in the 19th century in the UK. Today, it serves the UK, Europe, the Middle East, and Africa. Its fleet includes climate‑control gear like air conditioners, chillers, heaters, dehumidifiers, plus pumping equipment. The company is split into Hire & Sales (UK, Europe, Middle East) and a UK installation arm. We like its wide reach and focus on essential services.

The 43% Return: Breaking Down the Numbers

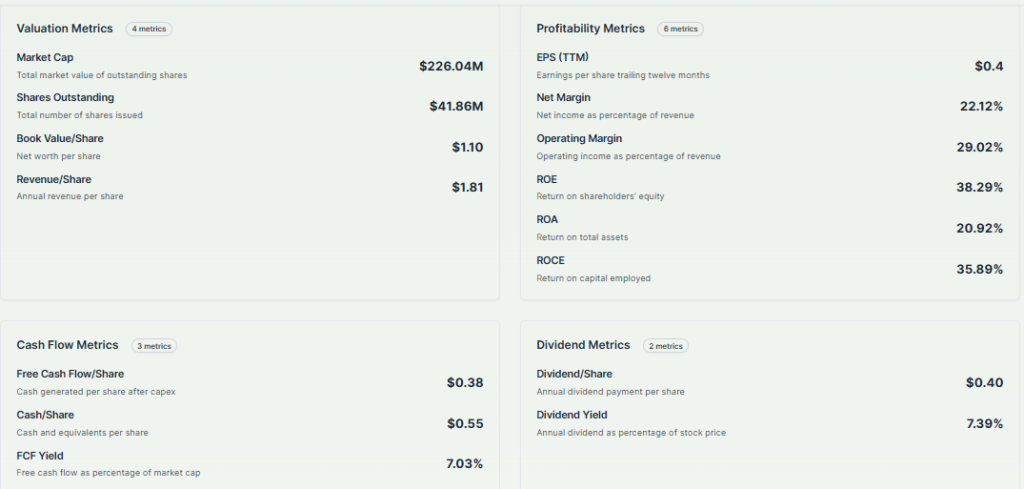

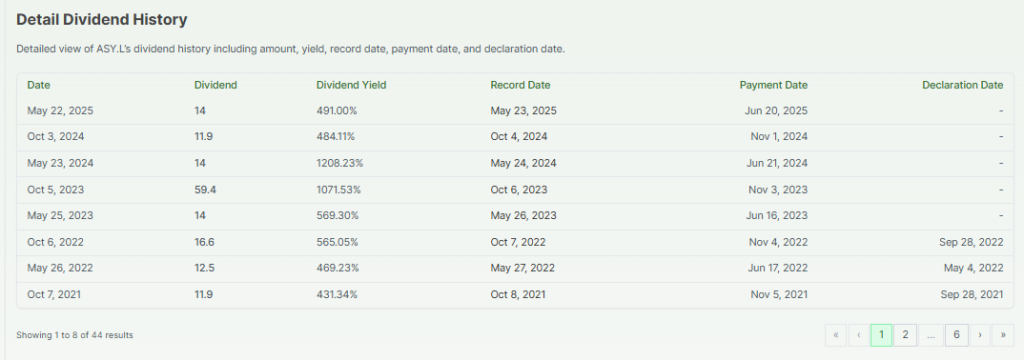

Andrews Sykes has delivered a strong 43% total return across the last three years. That includes gains in stock price and dividends. Its final 2024 dividend was £0.14 per share, adding about a 4.8% yield.

Earnings per share for full‑year 2024 came in at roughly £0.40, down slightly from £0.42 in 2023. Even with mixed operating numbers, investors saw a solid rise in value.

What’s Driving the Performance?

Operational efficiency. Costs are under control. In 2024, operating profit hit a record £23.2 m, up 2% year-on-year. Management is right-sizing the fleet and cutting leases strategically.

Steady demand. Construction, data centers, and events keep gear running. Although 2024 had a cooler summer, the core UK business still posted strong profits (£15.4 m operating). In Europe, milder weather hit revenue but didn’t fully erode margins.

Recovery in the Middle East. Revenue jumped from £5.6 m to £7.7 m in 2024. Operating profit nearly tripled to £1.1 m. This shows growth in emerging markets under new local leadership.

Resilience in volatility. Despite some revenue dips, overall group profit stayed firm. Net income moved from £17.8 m down slightly to £16.8 m. We see it as a sign of solid cost discipline.

Investor Sentiment and Market Perception

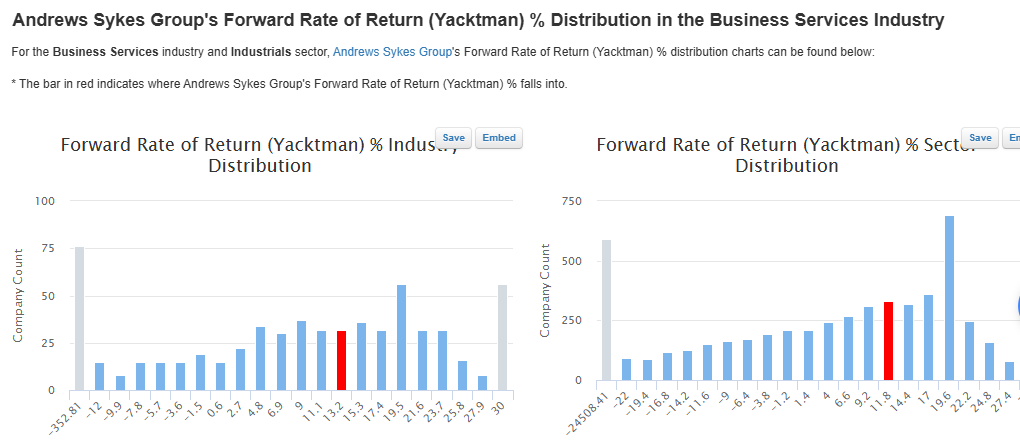

Analysts give limited coverage, but investors rate this stock for steady dividends and resilience. The forward rate of return (Yacktman method) stands at about 12.9% slightly above the industry norm.

This means cash flow and growth may offer a strong future payoff. Institutional players like HSBC and CBH hold small stakes, showing moderate backing. We feel the market trusts its consistent, value‑added model.

Risks and Challenges

The weather is a factor. Cool summers reduce AC rental demand, as seen in 2024. Fuel and power costs could squeeze margins. Europe saw a 3.6% revenue dip in 2024, partly due to pulling out of unprofitable French operations.

Currency shifts, like a strong pound, also affected international earnings. Competitors in hiring and leasing can add pressure. Rules on emissions and energy use may bring extra compliance expenses.

Outlook and Future Potential

Management expects momentum to carry on into 2025. They are focusing on Middle East growth, plus cost control, and fleet optimisation. The next full‐year dividend remains at £0.14, offering a stable yield.

With a strong forward return and record profitability in 2024, the company seems well‑positioned to grow. If demand rises with weather swings or new infrastructure, we could see more upside.

Bottom Line

We see Andrews Sykes as a quiet winner. It blends steady income, strong margins, and a wide service footprint. The 43% gain over three years is not luck; it’s a result of efficiency, balanced exposure, and careful expansion. For investors who value steady results and income, this firm offers real value. We’ll keep a close eye, as its core model checks a lot of long‑term boxes.

Frequently Asked Questions (FAQs)

Andrews Sykes is mainly owned by a Murray family trust through EOI Sykes SARL, holding about 87% of shares. Jacques “Tony” Murray led it until his passing in 2023.

The Andrews Sykes Group reported annual revenue of £75.9 million for the year ended December 31, 2024, marking a 3.6% decline from the previous year.

Disclaimer:

This content is for informational purposes only and not financial advice. Always conduct your research.

What brings you to Meyka?

Pick what interests you most and we will get you started.

I'm here to read news

Find more articles like this one

I'm here to research stocks

Ask our AI about any stock

I'm here to track my Portfolio

Get daily updates and alerts (coming March 2026)