India’s banking sector just had a busy quarter. Two of its biggest private banks, HDFC Bank and ICICI Bank, have posted their results for Q1 FY26. These numbers provide a detailed view of how the top banks, HDFC vs ICICI Bank, are performing in a rapidly changing economy.

HDFC and ICICI are not just names. They handle crores of customer accounts, loans, and investments every day. Even common citizens can feel the impact of how well these banks do.

Advertisement

Now that the merger of HDFC Ltd. and HDFC Bank is behind us, all eyes are on how the bank will manage growth, profits, and costs. On the other hand, ICICI Bank has stayed strong with stable margins and better asset quality this quarter.

Let’s not just compare numbers. We’ll break down what these Q1 results mean for investors, depositors, and anyone watching India’s financial growth.

Macro Market Angles

Both HDFC and ICICI beat expectations in Q1 FY26, and investors took notice. On July 21, the stocks for both banks jumped after earnings surprises. ICICI surged ~3%, while HDFC rose nearly 3%, bouncing off technical support and gaining over 20% year to date. The broader market followed, with the Nifty and Sensex rising modestly thanks to banking gains. Meanwhile, trade talk optimism ahead of a U.S.-India deadline on August 1 compensated for global uncertainty.

Financial Highlights: HDFC vs ICICI Bank

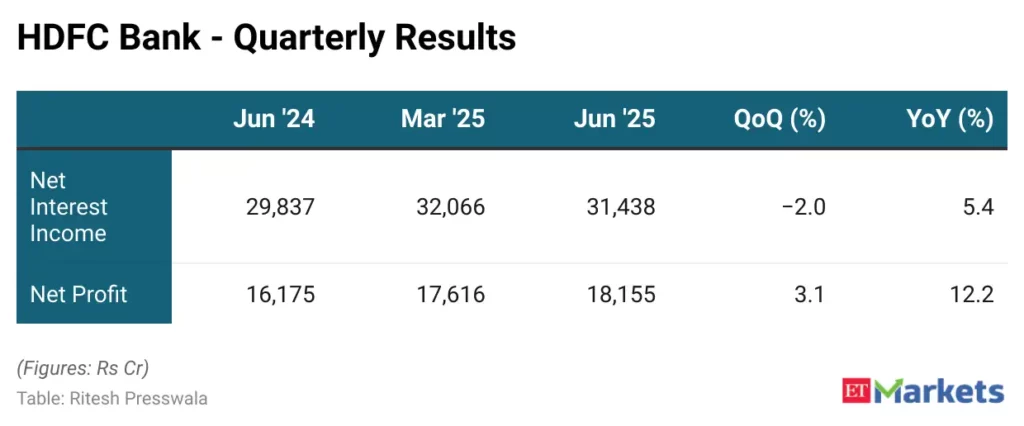

HDFC Bank

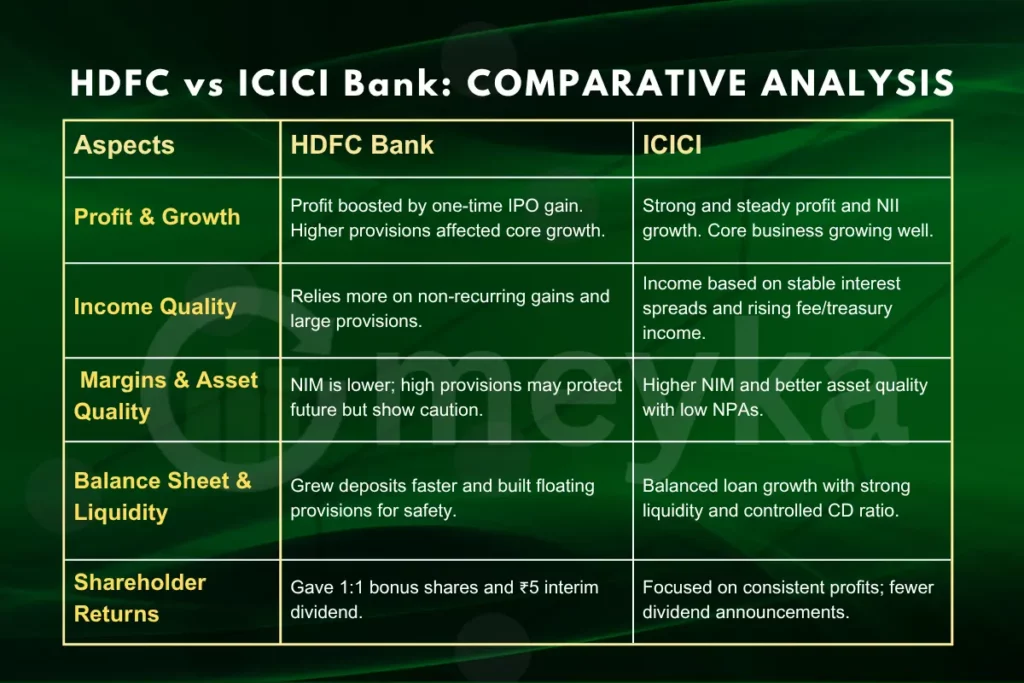

HDFC Bank’s standalone net profit rose 12.2% YoY, reaching ₹18,155 crore. It managed to report strong interest income while maintaining healthy loan quality. Net interest income (NII) grew 5.4% YoY, to ₹31,439 crore. Operating costs climbed only ~5%, showing tight cost control.

Big headline items included ₹9,128 crore gain from the HDB Financial Services IPO and a large ₹14,442 crore provision stack, mostly floating buffers for future risks. These moves suggest the bank is staying cautious while capturing one-off gains.

On top of earnings, HDFC declared a 1:1 bonus issue and ₹5 per share interim dividend, making it an attractive option for retail investors. The bank’s deposits rose ~16% YoY, thanks largely to growth in term deposits and a CASA ratio of ~34-35%.

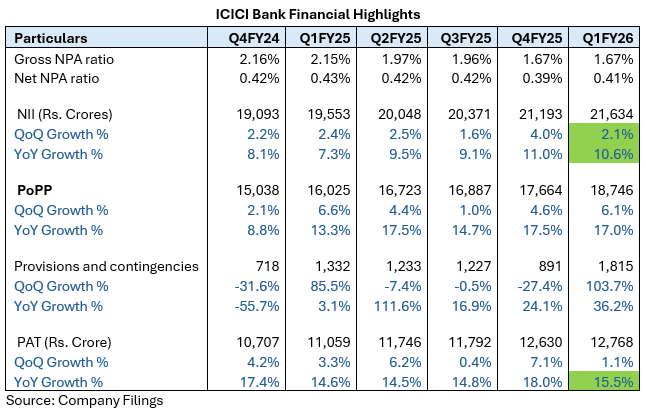

ICICI Bank

ICICI Bank recorded 15-16% YoY net profit growth of ₹12,768 crore on a standalone basis and ₹13,558 crore consolidated. Its Net Interest Income increased ~8-11% YoY to ₹21,634-21,635 crore.

The bank’s loan book expanded ~12% YoY to ₹13.3 trillion, while deposits grew ~11-13% on average. Importantly, ICICI maintained strong asset quality; gross NPA dropped from 2.15% to 1.67%, net NPA held at ~0.41%, and coverage ratio stood at ~75%. Capital levels remained solid with CET1 at ~16.3% and CAR at ~17%.

Non-interest income (excluding treasury) also grew ~14% YoY, reflecting diversified revenue streams. The bank also approved buying out ICICI Prudential Pension Fund, moving to strengthen fee income.

HDFC vs ICICI Bank: Comparative Analysis

Market Reaction & Analyst Views

HDFC is a “top pick” among brokers, driven by optimism over bonus issue, merger impact, and credit growth. But analysts caution that near-term margins may compress until charts break key resistance.

Meanwhile, short-term traders prefer ICICI. Its performance and lighter CD ratio give it an edge in liquidity and momentum. Short-term investors are betting on clean growth and stable spreads at ICICI.

Risks & Watch-outs

- HDFC: Margin pressure, high CD ratio, reliance on one-time gains, and heavy provisioning.

- ICICI: Slower loan growth in some segments, possible treasury volatility, and acquisitions integration.

- Macroeconomic: RBI policy decisions, global trade dynamics before August 1 U.S.-India deadline, could shift trends.

Valuation & Investor Implications

ICICI offers momentum and margin-led growth. Its lower payout but steady returns make it suited for those seeking earnings expansion. HDFC appeals to long-term investors due to strong shareholder returns, bonus shares, and potential gain from merged synergies.

Bottom Line

We can say both banks delivered strong Q1 FY26 results, but reasons differ. ICICI shows consistent, organic growth with clean margins. HDFC delivers big shareholder rewards but relies more on one-offs and high provisioning. If you want fast, recurring earnings and stable asset quality, ICICI fits well. If you seek high yield and long-term merger benefits, HDFC offers a compelling play.

Advertisement

Frequently Asked Questions (FAQs)

Both banks are strong. ICICI has better profit growth and cleaner income this quarter. HDFC offers high returns and long-term value. It depends on your goal.

ICICI Bank made ₹12,768 crore profit in Q1 FY26. Its loan book and deposits grew well. It also kept good asset quality with low bad loans.

HDFC Bank reported ₹18,155 crore profit in Q1 FY26. It grew slower than ICICI but gave bonus shares and a ₹5 special dividend to investors.

HDFC is good for long-term holding. It gives steady returns and strong dividends. But short-term growth may be slower than other banks right now.

Disclaimer:

This content is for informational purposes only and not financial advice. Always conduct your research

Advertisement

What brings you to Meyka?

Pick what interests you most and we will get you started.

I'm here to read news

Find more articles like this one

I'm here to research stocks

Ask Meyka Analyst about any stock

I'm here to track my Portfolio

Get daily updates and alerts (coming March 2026)