HDFC Bank Profit Falls to Rs 16,258 Crore Despite HDB IPO Gain; Provisions Surge to Rs 14,442 Crore

India’s largest private bank, HDFC Bank, just reported its earnings for the latest quarter. The numbers surprised many. Even though the bank made gains from the much-awaited HDB Financial Services IPO, its net profit fell to ₹16,258 crore.

That’s not what we expected from a giant like HDFC. Especially when there’s good news like an IPO boost. So, what happened? The short answer provisions. They jumped to ₹14,442 crore, eating up a big part of the bank’s earnings.

Advertisement

Let’s talk about the HDB IPO, the reasons behind the sudden rise in provisions, and how the recent HDFC, HDFC Ltd. merger is still impacting the numbers.

It’s a mix of good news and caution signs. So let’s dig deeper into what’s going on with HDFC Bank and what it means for the future.

Key Highlights of the Q1 Financial Results

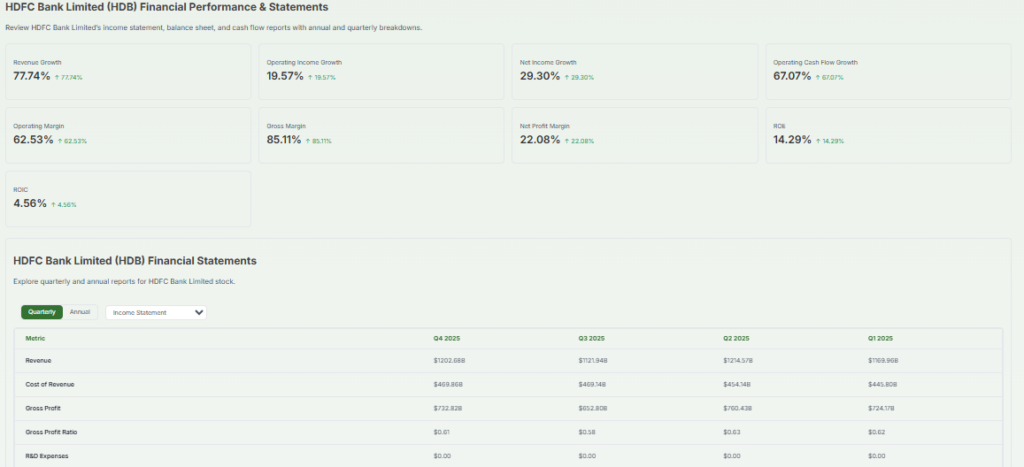

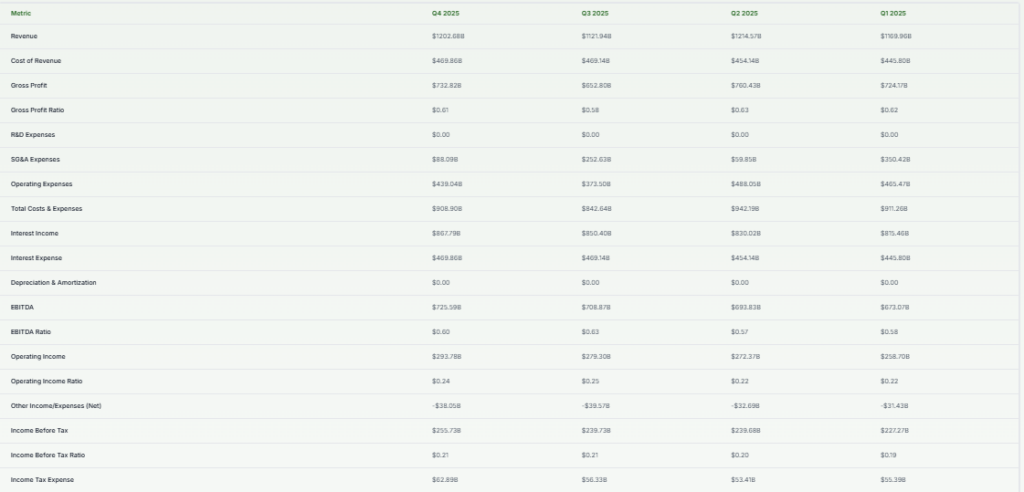

HDFC Bank’s consolidated net profit for April-June 2025 dipped 1.3% to ₹16,258 crore, down from ₹16,475 crore a year ago. Yet, its standalone net profit (core operations) climbed 12.2% YoY to ₹18,155 crore, driven by strong income growth.

Net Interest Income (NII) rose by 5.4% to ₹31,438 crore, while other income more than doubled, reaching ₹21,730 crore, thanks to treasury gains and the HDB IPO.

Despite this, provisions skyrocketed from about ₹2,600 crore to ₹14,442 crore, weighing on the bottom line.

The Role of Provisions

The main culprit behind the profit dip was a massive rise in provisions. HDFC Bank set aside ₹14,442 crore, which included:

- ₹9,000 crore in floating provisions

- ₹1,700 crore in contingent buffers

These were taken as precautionary steps, not due to actual bad loans.

Management explained that most provisions were meant to strengthen the balance sheet against possible future stress, not in response to rising defaults.

Additionally, fresh slippages rose to ₹9,000 crore, attributed partly to seasonal challenges in agriculture. Both Gross NPA (1.40%) and Net NPA (0.47%) inched up from the previous quarter.

HDB Financial Services IPO and One-Time Gains

HDFC Bank earned a pre-tax gain of ₹9,128 crore from the IPO of its subsidiary, HDB Financial Services.

This lifted other income significantly, even as the bank reduced its stake from 94.3% to 74.2%.

However, since these gains were one-time, they didn’t help offset the huge increase in provisions. Long term, HDB’s listing opens doors for monetization and sharper focus on the NBFC business.

Impact of HDFC, HDFC Ltd. Merger

The merger of HDFC Ltd and HDFC Bank in July 2023 brought in a large mortgage book.

While the expanded loan base supports growth, it also requires higher provisioning and has put pressure on net interest margins.

New loans from merged portfolios need diligent monitoring. So, while expected, the integration is still affecting how aggressively the bank provisions its loan book.

Asset Quality and Balance Sheet Analysis

- Gross advances grew 6.7% YoY to ₹26.53 lakh crore.

- Deposits surged ~16%, crossing ₹27.6 lakh crore, but the CASA ratio declined to ~34% from 38%.

- NII growth of 5.4% shows solid core earnings, though the NIM narrowed to 3.35% due to faster deposit repricing.

- Capital Adequacy Ratio remains strong at ~19.9%, providing a buffer for capital risks.

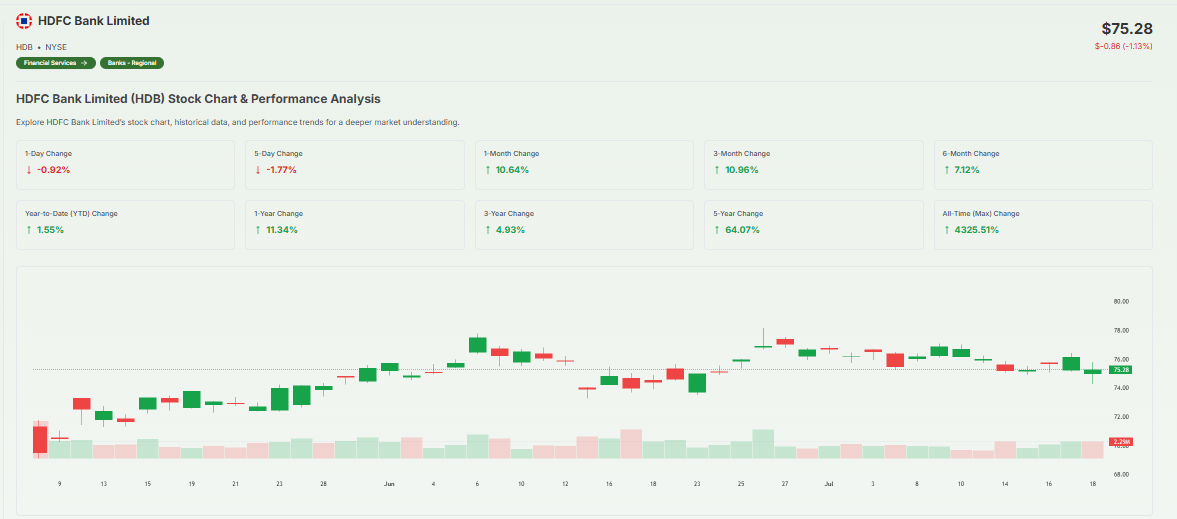

Market and Investor Reaction

After the results, HDFC Bank’s stock fell ~1.6%, reflecting investor caution. Analysts praised the strong interest and fee income. They also noted that provisions were strategic, not panic-driven.

Shareholder-friendly moves, like a 1:1 bonus share and a ₹5/share interim dividend, underline management confidence.

Future Outlook and Strategy

We expect HDFC Bank to:

- Let rate cuts feed into loan yields gradually, which should help margins.

- Manage floating provisions carefully to avoid a hit to profits.

- Keep a conservative watch on agri and unsecured loans, where slippages rose.

- Leverage HDB Financial’s success to build stronger fee income streams.

Wrap Up

Q1 was a mixed bag for HDFC Bank. Core operations look strong. But heavy provisioning to build buffers hit reported profit. Going ahead, the bank’s focus will be on balancing income growth, careful risk provisioning, and monetizing HDB.

We think this cautious approach strengthens resilience, but investors should watch how provisions evolve in the coming quarters.

Advertisement

Frequently Asked Questions (FAQs)

The HDB IPO brought a one-time gain of ₹9,128 crore to HDFC Bank. It cut the bank’s stake in HDB from about 94% to 74%, boosting other income.

No. For Q1 FY25, HDFC Bank’s net profit fell 1.3% to ₹16,258 crore, not ₹16,175 crore. The latter figure was for a prior year period.

HDFC Bank’s standalone return on assets (ROA) hovered around 0.48% in Q1 FY26, indicating its profit per ₹100 of assets held.

Yes. HDB Financial launched a ₹12,500 crore IPO ₹2,500 crore in fresh capital and ₹10,000 crore offered by HDFC Bank. This cut the bank’s stake to about 74%.

Disclaimer:

This content is for informational purposes only and not financial advice. Always conduct your research.

Advertisement

What brings you to Meyka?

Pick what interests you most and we will get you started.

I'm here to read news

Find more articles like this one

I'm here to research stocks

Ask Meyka Analyst about any stock

I'm here to track my Portfolio

Get daily updates and alerts (coming March 2026)