The Lloyds share has shown a strong 40% rally in 2025, catching the attention of investors and analysts. The surge came after the release of the H1 2025 results, which revealed a mix of resilience and strategic clarity. But many are now asking, Can this growth continue into 2026?

Let’s get deeper into the numbers, performance, market expectations, and what investors are thinking.

Advertisement

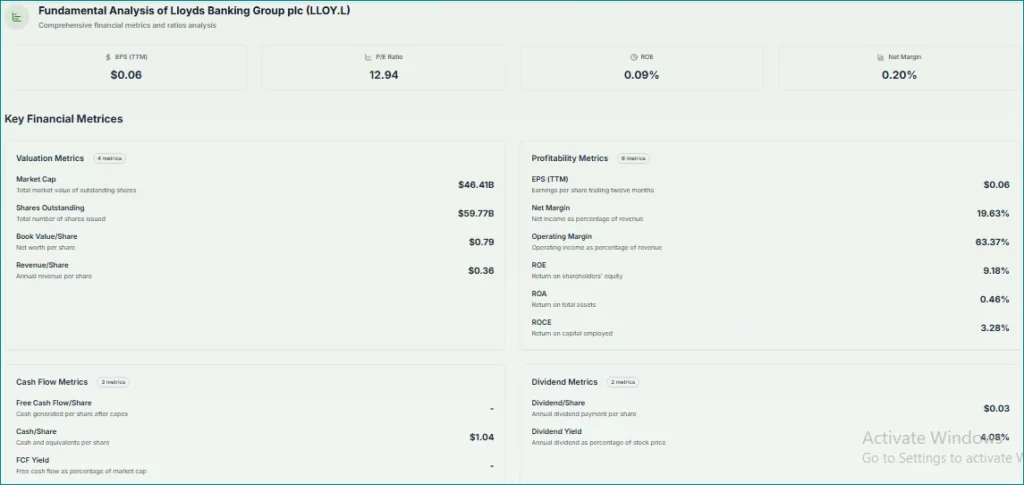

What Did Lloyds Report in H1 2025?

Lloyds Banking Group announced its H1 2025 results, revealing a 4% increase in profit and a 15% dividend hike. The bank’s net income rose to £9.3 billion, supported by higher interest margins and stable loan books. It also maintained a strong CET1 capital ratio, suggesting solid financial health.

As per Investing.com, Lloyds’ performance beat analysts’ expectations, especially with its rising profitability and return on tangible equity (RoTE) at 13.6%.

Lloyds’ earnings data shows a steady uptrend in core income, as reflected in their latest H1 2025 report.

Why Is the Lloyds Share Rallying So Strongly?

There are a few reasons behind this upward trend:

- Dividend boost: The 15% dividend increase made Lloyds more attractive to income-focused investors.

- Strong earnings: The bank continues to benefit from high interest rates in the UK, which have increased its net interest income.

- Digital shift: Lloyds has been investing in digital banking and AI, which is helping improve efficiency and cut operational costs.

But the real question is…

Will the Lloyds Share Keep Rising?

While the 40% rally in 2025 is impressive, many investors are cautious about whether it can continue.

In an article by Yahoo Finance UK, analysts noted that while Lloyds shows strength, economic uncertainty, inflation pressures, and potential rate cuts in 2026 could slow future gains.

The following chart clearly illustrates the 2025 rally in Lloyds share price, highlighting its key performance spikes

Still, the bank’s clear 2025 blueprint focusing on sustainable growth, improved digital services, and increased customer engagement shows potential for further upside.

What Are Experts and Investors Saying?

Social media has been buzzing after the H1 results. Let’s take a look at what experts are tweeting:

@PositiveMoneyUK commented, “UK banks continue to profit off higher interest rates, but are they giving back enough to customers? Lloyds results spark debate.”

@wallstengine tweeted, “Lloyds shares up 40% in 2025! Solid performance in H1, but macro headwinds could test this rally in H2.”

@entrustTMF noted, “With rising dividends and strong capital ratios, Lloyds looks well-positioned. One of the most stable UK banking stocks right now.”

How Is Lloyds Performing Compared to Other UK Banks?

Lloyds is doing better than some of its peers, like Barclays and NatWest, in 2025, especially in shareholder returns. Its RoTE of 13.6% is among the highest in the sector. The bank’s cost-to-income ratio has also improved, showcasing its efficiency.

Compared to HSBC, Lloyds still lags in global diversification, but its UK-focused strategy has worked well this year due to the stable domestic economy.

Are There Risks Ahead for Lloyds Share?

Yes, there are always risks. Some possible challenges include:

- A slowdown in the UK housing market could affect mortgage growth.

- Potential interest rate cuts in late 2025 or early 2026, may shrink the bank’s profit margins.

- Regulatory changes and political uncertainty could also impact operations.

These risks mean investors should stay informed and not expect the same 40% rise to repeat in H2.

Is Lloyds Undervalued or Positioned for Growth?

From a valuation perspective, Lloyds appears attractively priced compared to both its historical averages and key peers like Barclays. Analysts point to its low price-to-earnings (P/E) ratio, solid return on equity (ROE), and consistent dividend payouts as signs of strong underlying fundamentals.

Investors looking for value stocks with stable earnings and strong capital positions are viewing Lloyds as a potential growth pick, especially if the UK economy avoids a slowdown. While it might not offer explosive gains in H2 2025, the long-term upside remains promising.

What Should Investors Do Now?

If you’re already holding Lloyds shares, analysts suggest it’s worth holding for the long term, especially due to high dividends and stable performance. For new investors, entering after such a big rally might be risky unless the price dips or guidance for H2 improves.

According to The Motley Fool UK, Lloyds remains a “value stock with growth potential” as long as the UK economy avoids recession.

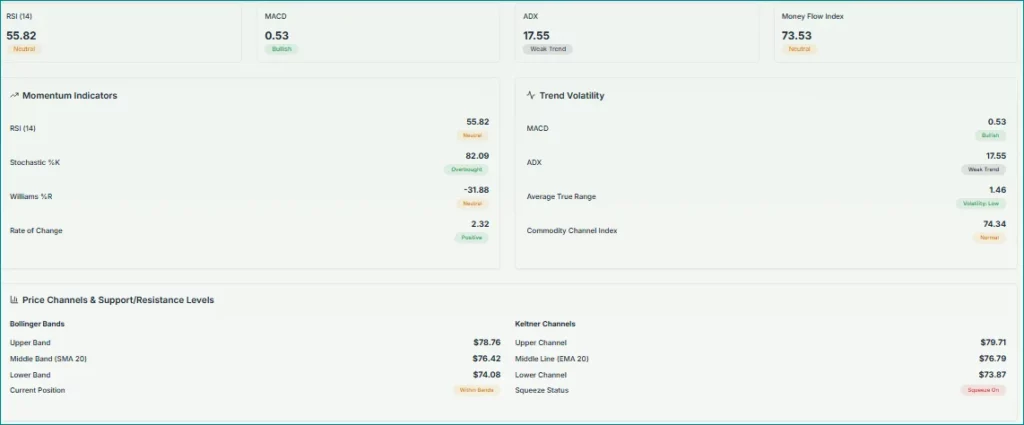

According to recent technical indicators, Lloyds share may still have upside potential. Here’s the technical breakdown.

Conclusion: Can the Rally Continue Beyond 2025?

Lloyds has delivered an excellent first half in 2025. The 40% gain in its share price is backed by solid financial results, increased dividends, and long-term digital transformation plans. However, macroeconomic conditions, interest rate decisions, and competition could influence future growth.

So, while the rally may not continue at the same pace, Lloyds is still a strong player in the UK banking space. Investors must watch the upcoming Q3 results, interest rate trends, and consumer sentiment to make smart decisions.

For now, Lloyds is winning the confidence of the market, but only time will tell if it can hold its ground in 2026.

Advertisement

FAQ’S

Analysts expect Lloyds to maintain or slightly raise its dividend in 2025, potentially offering a yield over 5%. The increase will depend on earnings and capital position.

Some analysts forecast moderate growth in 2025 driven by interest rates and digital banking gains. However, economic uncertainty could limit upside.

For income investors, Lloyds is appealing due to its strong dividend yield. But share price appreciation may be slower than growth stocks.

Many analysts consider Lloyds undervalued based on its price-to-book and strong capital ratios. However, value traps are a risk if growth stagnates.

Lloyds is more stable and UK-focused, ideal for conservative investors. Barclays has global exposure and higher risk-reward potential.

Recent declines are due to lower net interest margins and weak UK growth outlook. Market volatility and investor caution are also factors.

Disclaimer

This content is for informational purposes only and not financial advice. Always conduct your research.

Advertisement

What brings you to Meyka?

Pick what interests you most and we will get you started.

I'm here to read news

Find more articles like this one

I'm here to research stocks

Ask our AI about any stock

I'm here to track my Portfolio

Get daily updates and alerts (coming March 2026)