Do you know that more Gen X fear going broke than dying?

It sounds shocking, but it’s true.

We’re talking about people born between 1965 and 1980. That’s Generation X. Right now, they are in their 40s and 50s. For many of them, retirement is getting close. But savings? Not enough.

A report by the National Institute on Retirement Security says that most Gen X households have saved less than $50,000 for retirement. That’s not even enough to cover a few years of bills.

We grew up watching our parents retire with pensions. Now, most of us have to figure it out on our own. That means 401(k)s, IRAs, and savings. But life got expensive. Many of us are still paying off debts, raising kids, or caring for older parents.

Retirement used to mean rest. For Gen X, it feels more like a race against time.

Let’s talk about why Gen X is so worried, how we got here, and what we can still do to change the story.

Who is Generation X?

Generation X includes people born between 1965 and 1980. Today, we’re in our mid-40s to late 50s. We’ve lived through some tough times: the dot-com crash, the 2008 financial crisis, and now rising inflation.

We’re often called the “sandwich generation” because many of us are caring for both our children and our aging parents. That means more expenses and less time to save.

We don’t have pensions unlike our parents. We rely on 401(k)s and IRAs, which means we have to manage our own retirement savings.

The Fear Factor: Why Gen X Dreads Retirement

A recent Allianz survey found that 70% of Gen Xers fear running out of money more than death. That’s a big deal.

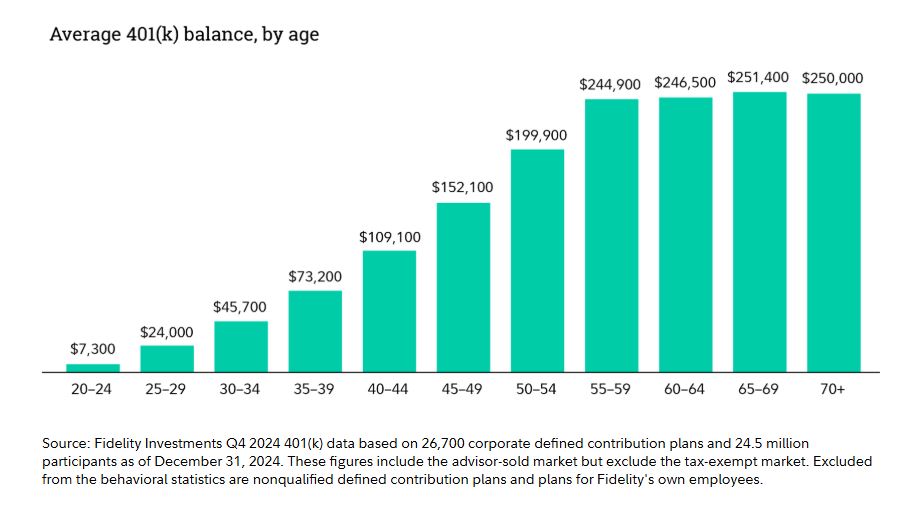

Why are we so worried? Because many of us haven’t saved enough. The average 401(k) balance for Gen X is $192,300, and the average IRA balance is $103,952.

But experts say we need about $1 million to retire comfortably. That means we’re way behind. Plus, we’re dealing with high living costs, healthcare expenses, and debt. It’s no wonder we’re anxious.

Missed Opportunities and Systemic Failures

Many of us didn’t learn about personal finance in school. We weren’t taught how to budget, save, or invest.

We’ve also faced economic challenges. The 2008 recession hit us hard, and many of us lost jobs or homes. Now, inflation is making everything more expensive.

Wages haven’t kept up with the cost of living. And without pensions, we’re left to handle retirement planning on our own.

The Retirement Savings Gap

According to Fidelity, the average retirement account balance for Gen X clients is $178,500. That’s far below the $1 million many experts recommend.

Why the gap? Because we started saving late, faced economic downturns, and had to deal with life’s expenses.

Many of us are still paying off student loans, mortgages, and credit card debt. That leaves less money for retirement savings.

Some of us hope Social Security will help, but there’s uncertainty about its future. We can’t rely on it alone.

Emotional and Mental Impact

The stress of financial insecurity takes a toll on our mental health. We worry about the future, feel upset, and sometimes even ashamed.

This anxiety affects our relationships and overall well-being. We may avoid thinking about retirement because it feels too daunting.

But ignoring the problem won’t make it go away. We need to face it head-on.

What Can Be Done? Solutions and Advice

- We can take on flexible jobs that keep us active and bring in some income. This reduces pressure on our savings.

- We don’t need to become experts. But understanding basic investments like index funds can help grow our savings. Avoid risky, get-rich-quick schemes.

- Many free resources, like AARP’s retirement tools, can guide us. We just need to take the first step.

- If we have access to employer retirement plans or matching contributions, we should always take full advantage of them.

- We’re not alone. Sharing worries with friends or support groups can lead to advice and peace of mind.

Taking small, steady steps today can make a big difference tomorrow.

Hope on the Horizon

The good news? We still have time.

Even if we’re behind, starting now matters. Many Gen Xers are already taking action. In fact, a 2024 study by Vanguard shows that Gen X participation in retirement savings plans has increased to 77%, a major jump from a decade ago.

There’s also more help out there. Online tools, robo-advisors, and apps like Fidelity, Mint, and Empower make saving and budgeting easier than ever.

We’re also seeing a shift in mindset. More of us are becoming aware of the problem. That awareness leads to action. And action leads to change.

We may not have pensions. But we have resilience, experience, and the drive to take control.

Final Thoughts

Retirement doesn’t have to be scary. Yes, Gen X faces big challenges. But we’re also tough.

We’ve faced recessions, job losses, and rising costs, and we’re still standing. We don’t need to fear the future. What we need is a plan, a goal, and the courage to take the first step.

Let’s not wait any longer. The sooner we act, the better our retirement years can be. We owe that to ourselves, and to the next generation watching us.

Because we’re not just Generation X. We’re Generation Strong.

Frequently Asked Questions (FAQs)

Many Gen Xers plan to retire later than expected, with 47% anticipating delayed retirement due to insufficient savings and economic pressures.

Financially, Gen X faces challenges: 35% have less than $10,000 saved for retirement, and 46% doubt they’ll have enough to retire comfortably.

Gen X is facing many problems. Prices keep going up. Healthcare is expensive. Many help both their kids and parents. This makes it hard to save money for retirement.

Gen X is concerned about outliving savings, rising healthcare expenses, and the reliability of Social Security benefits in retirement.

Disclaimer:

This content is for informational purposes only and not financial advice. Always conduct your research.

What brings you to Meyka?

Pick what interests you most and we will get you started.

I'm here to read news

Find more articles like this one

I'm here to research stocks

Ask our AI about any stock

I'm here to track my Portfolio

Get daily updates and alerts (coming March 2026)