Federal Bank Shares Drop 5% After Q1 Profit Decline: What Do Analysts Recommend?

Federal Bank’s shares took a sharp hit, falling nearly 5% in a single day. This drop came right after the bank posted its Q1 earnings, which showed a 15% fall in net profit compared to the same time last year. It caught many investors off guard.

So, what happened? Why did profits drop? And more importantly, should we stay invested, sell, or buy more?

Advertisement

Let’s look at what went wrong this quarter, how the market reacted, and what top analysts think about the future of Federal Bank.

Key Financial Highlights from Q1

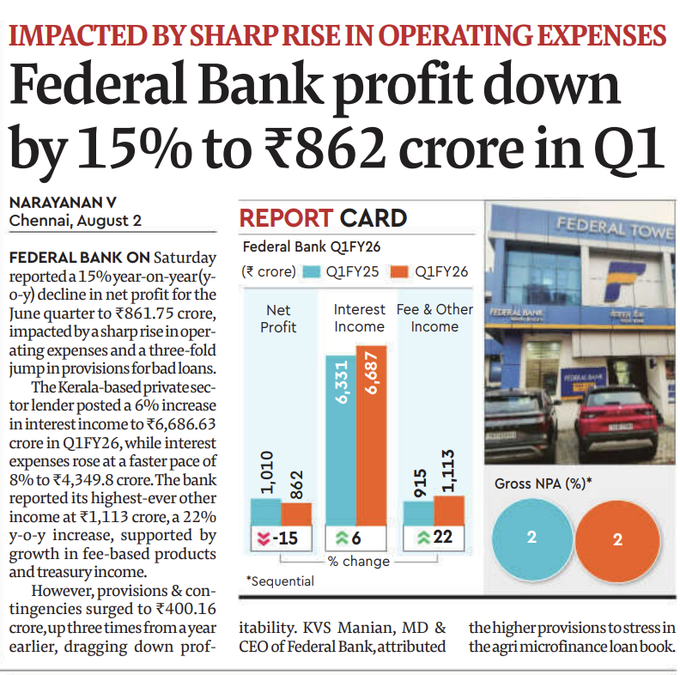

In the June quarter, Federal Bank’s net profit dropped to ₹861.75 crore. This was a 14.6% fall from ₹1,009 crore in the same time last year. However, the bank’s main income stayed stable. Its net interest income (NII) went up 2% from last year, reaching ₹2,336.83 crore. The bank also earned its highest-ever other income of ₹1,113 crore, showing strong growth of 21.6%.

Deposits grew steadily, rising 8% year-on-year to ₹2.87 lakh crore. Loans, or advances, also increased by nearly 9%, reaching ₹2.41 lakh crore. The CASA ratio improved to about 30%. Fee income touched a new high of ₹786 crore during the quarter, showing healthy earnings from non-interest sources.

Reasons Behind the Profit Decline

We saw two main pressures on the numbers. First, provisions jumped significantly. They rose over 170% YoY, hitting around ₹400 crore. This was driven by slippages in microfinance (MFI) and agriculture loans.

Second, credit costs rose sharply, reaching about 65-67 basis points, up from 24 bps a year ago and 27 bps in the previous quarter. Slippages climbed too. MFI slippages peaked in May and began to ease in June and July.

While these were big negatives, there were positives. Asset quality improved. Gross NPA ratio slipped down from 2.11% to 1.91%, and net NPA eased to 0.48%.

Market Reaction & Technical Outlook

The market reacted fast. Shares dove about 5-6% on Q1 results day to ₹185, the lowest level in over three months. Later, the price bounced a bit, trading near ₹195 by midday.

Technical indicators showed a bearish setup. A recent MACD crossover and a break below the ₹200 support zone suggest room for more downside in the near term.

Analyst’s Recommendations

Avendus

Avendus has given Federal Bank an “Add” rating. They lowered the target price to ₹209 from ₹216. The firm thinks the return on assets (RoA) may stay around 1% because profit margins are under pressure. They also cut their credit growth forecast for FY26 to 10%. According to them, the bank is worth 1.2 times its expected book value for FY27.

Motilal Oswal

They stuck with a “Buy” rating but cut the target to ₹235. They expect Q1 slippages to ease over H2 and forecast credit costs of around 55 bps for the year. RoA is seen improving to 1.18% and RoE to 13% by FY27.

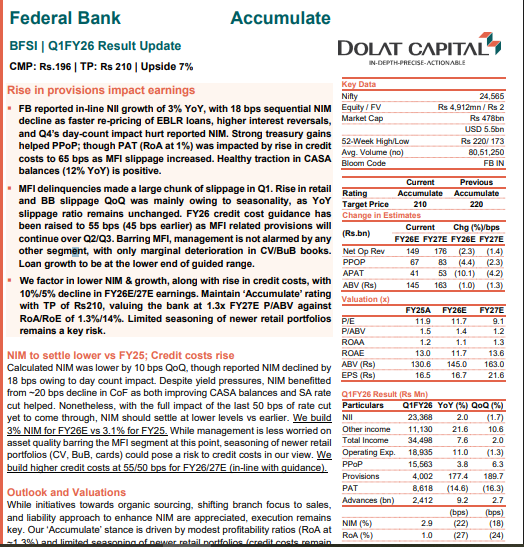

Dolat Capital

Maintained an “Accumulate” stance with a new target of ₹210. Their view draws attention to modest RoA, limited seasoning of new retail assets, and expected credit costs rising to 55 bps this year. They note CASA traction is a positive sign.

Others

Nuvama and CLSA also maintained Buy / Outperform ratings. They cited improving asset quality and a strong fee‑income base as reasons for optimism. Morgan Stanley, however, stayed cautious. It flagged continued high provisions and set a lower target of ₹165, considering credit risk to remain elevated over H1 FY26.

Summary Table: Analyst Views

| Broker | View | Target Price | Key Points |

| Avendus | Add | ₹209 | RoA to bottom at ~1%, credit growth cautious |

| Motilal Oswal | Buy | ₹235 | Slippages to ease, margins to recover |

| Dolat Capital | Accumulate | ₹210 | Elevated credit cost, still improving CASA |

| Nuvama / CLSA | Buy / Outperform | ~₹230 | Fee income strength, improving asset mix |

| Morgan Stanley | Underweight | ₹165 | Cautious view on MFI stress and cost load |

What Investors Should Consider?

We think several points should guide decision‑making now:

We see potential upside. Most targets fall between ₹210-235, which is about 10-25% above today’s levels. This may offer room to gain if slippages ease and margins recover.

That said, risks remain real. High provisions, MFI defaults, and NIM pressures could knock earnings further in the near term. Return metrics like RoA (~1%) and RoE (~10%) are still subdued despite improvements.

Federal Bank has strength too. Digital transactions account for over 90% of activity. Its focus on commercial banking, gold loans, and credit cards shows diversification. Fee income and CASA ratio are trending positively.

So if you are a long-term investor, staying near ₹200-210 may fit someone looking for value. But cautious investors may prefer to wait for clearer signs of credit normalization.

Bottom Line

Federal Bank’s Q1 showed weak profit due to rising slippages in the MFI and agriculture portfolios. NII growth was modest, and margins compressed. These triggered a 5-6% share price fall.

Still, the bank earned its highest-ever non-interest income. It also kept good growth in deposits and loans. Even though asset quality was under pressure, early signs of improvement were seen.

Most analysts remain constructive, giving Buy/Add ratings with targets mostly in the ₹210-235 range. A few are defensive, waiting for better clarity. This may be a good time for long-term investors to hold conviction, while risk‑averse traders might want to stay on the sidelines until the credit picture improves.

Advertisement

Frequently Asked Questions (FAQs)

Analysts expect a 12‑month target of around ₹227-235 based on current data. Some set a low of ₹165 due to caution. Average target is ₹227.6.

As of July 2025, shares are falling because Q1 net profit dropped about 14.6% due to high loan provisions for microfinance and agriculture. Investors also worry about margin decline.

Most analysts rate it “Buy” or “Add” with targets around ₹209-235. But some are cautious, giving “Underweight” or “Neutral” views around ₹165-195.

Yes. Deposits rose nearly 8% and loans grew about 9%. Fee income hit a record high. Profit growth is moderate, but credit cost pressure is present.

Disclaimer:

This is for information only, not financial advice. Always do your research.

Advertisement

What brings you to Meyka?

Pick what interests you most and we will get you started.

I'm here to read news

Find more articles like this one

I'm here to research stocks

Ask Meyka Analyst about any stock

I'm here to track my Portfolio

Get daily updates and alerts (coming March 2026)