Eternal Share Price Analysis: What Q1 2025 Results Mean for Zomato’s Parent Company

Eternal, the parent company of Zomato, just released its Q1 results for FY2025. The numbers of Eternal share price analysis got everyone talking: investors, market watchers, and even everyday food delivery users like us. Why? Because this isn’t just about one quarter. It’s about what comes next for a company shaping how millions of Indians eat, shop, and order online.

Zomato’s journey from a food discovery app to a full-stack tech platform has been bold. But now, Eternal handles much more Blinkit (quick commerce), Hyperpure (B2B supplies), and logistics. So, when earnings drop, we’re not just checking profits. We’re tracking future trends.

Let’s break down what the Q1 FY2025 results mean for Eternal’s share price. We’ll look at how its different businesses performed, why the stock moved the way it did, and what it means for people thinking about investing.

Eternal: Company Overview

Eternal began life as Zomato, a food‑discovery app in 2010. Over time, it grew fast. Now, it covers food delivery, quick commerce (Blinkit), B2B supplies (Hyperpure), and event ticketing (District). Its model links technology with everyday needs. It makes money when people order meals, groceries, or party tickets through its app. Today, Eternal is more than a food app. It is a full‑stack tech firm serving millions in India.

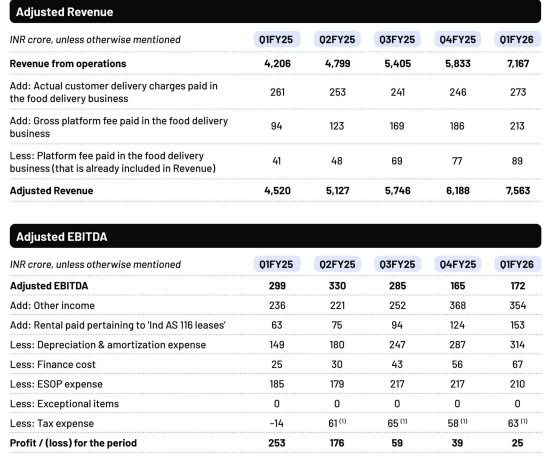

Q1 FY2026 Financial Snapshot

In Q1 FY26, Eternal posted ₹7,167 crore in revenue. That’s 70 percent more than a year ago. But net profit fell 90 percent to just ₹25 crore. Adjusted EBITDA slipped 42 percent to ₹172 crore, even though food delivery margins improved slightly to 5 percent. Blinkit revenue jumped 155 percent to ₹2,400 crore. Hyperpure grew by 89 percent, making ₹2,295 crore. Food delivery revenue reached ₹2,261 crore, up 16 percent.

Market Reaction & Share Price Movement

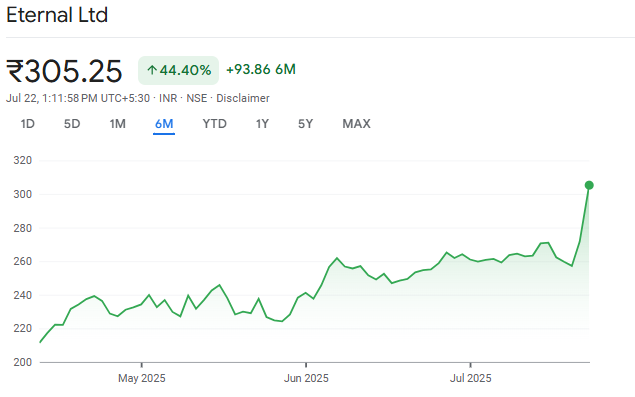

The day results came out, Eternal shares rallied. They jumped about 7-15 percent, settling between ₹277 and ₹312 levels not seen in five months.

Investors cheered the strong revenue and quick commerce dominance. Even with profit dipping, market sentiment stayed upbeat. By the next day, Eternal was the top gainer on Nifty 50.

Key Growth Drivers & Strategic Moves

Blinkit stole the show. It became the largest part of B2C business. For the first time, Blinkit’s net order value beat that of food delivery 127 percent growth year-on-year. Blinkit added 243 new dark stores to reach 1,544 by June-end.

Hyperpure also grew strongly and helped restaurants buy produce. The company even moved to own inventory in quick commerce. The CFO said this sets the stage for better margins later. Food delivery also improved, thanks to leaner operations.

Eternal Share Price Analysis: Risks & Challenges

Rapid expansion comes at a cost. Blinkit had an EBITDA loss of ₹162 crore this quarter. That makes it harder to boost overall profits. Plus, competition is intense. Swiggy, BigBasket, Amazon, and Flipkart are investing heavily.

Hyperpure may slow soon. The company warned it may see de-growth in B2B in the coming quarters. Also, rising wages and fuel prices threaten delivery costs.

Analyst Views & Projections

Brokerages like Motilal Oswal and Elara raised their target prices to ₹330-340, citing Blinkit’s momentum. UBS, Citi, and Bernstein praised quick commerce strength. But Macquarie flagged cost challenges and valuation risks.

Analysts say Eternal aims to grow food delivery by 30 percent yearly. They see Blinkit pushing margins in the next 12-18 months.

What Does It Mean for Investors?

We see a mixed picture. For investors focused on revenue and future market share, this quarter is encouraging. Blinkit is climbing fast. For those who want profits now, margins are still under strain.

If you’re a growth investor, Eternal looks promising. For value investors, it’s risky until margins improve. But strong cash reserves (₹18,857 crore) provide a cushion.

Wrap Up

Eternal’s Q1 report shows its transformation into a diversified tech firm. Revenue is up 70 percent. Blinkit now leads B2C. But profit dropped sharply due to heavy spending on expansion. The market cheered the growth story, not the profit line.

We believe the coming quarters will test whether Blinkit’s scale can turn costs into profits. For now, Eternal offers a ride with high speed and some bumps. Investors should track Eternal share price analysis margins closely and keep an eye on how quickly quick commerce can stabilize its returns.

Frequently Asked Questions (FAQs)

As of July 22, 2025, Eternal (parent of Zomato) shares trade around ₹311.60 on BSE. They hit an all-time high after Q1 results came out.

Eternal Limited is itself the parent company. It owns Zomato, Blinkit, Hyperpure, and District.

Shares fell earlier due to faster hiring and expansion costs, rising expenses in Blinkit, and foreign fund limits. These hurt profits and sentiment.

In Q1 FY26, Eternal’s revenue rose 70% to ₹7,167 cr, but net profit dropped 90% to ₹25 cr. EBITDA fell by over 40%.

Disclaimer:

This content is for informational purposes only and not financial advice. Always conduct your research.

What brings you to Meyka?

Pick what interests you most and we will get you started.

I'm here to read news

Find more articles like this one

I'm here to research stocks

Ask our AI about any stock

I'm here to track my Portfolio

Get daily updates and alerts (coming March 2026)