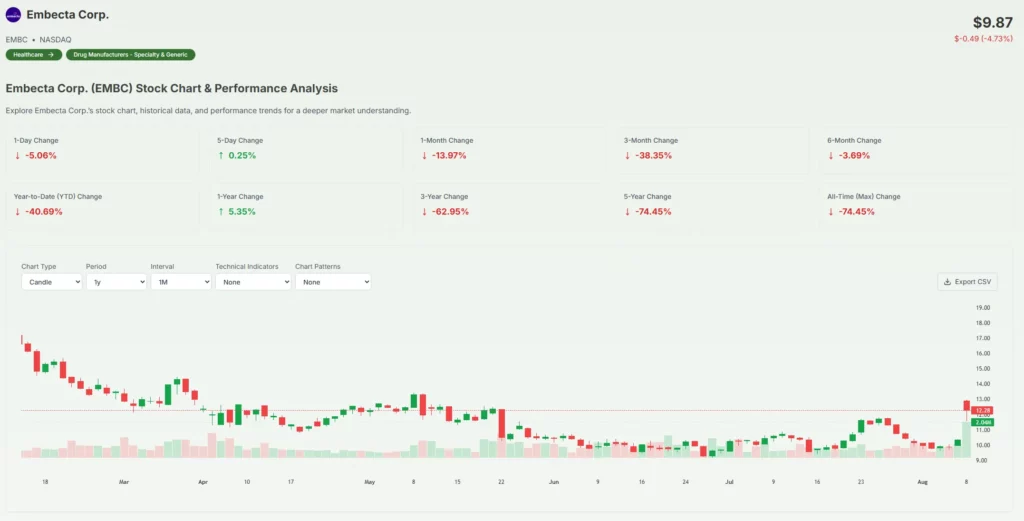

Embecta Corp Q3 2025 Outperformance: A Key Opportunity for Strategic Re-Rating Amid Margin Stability

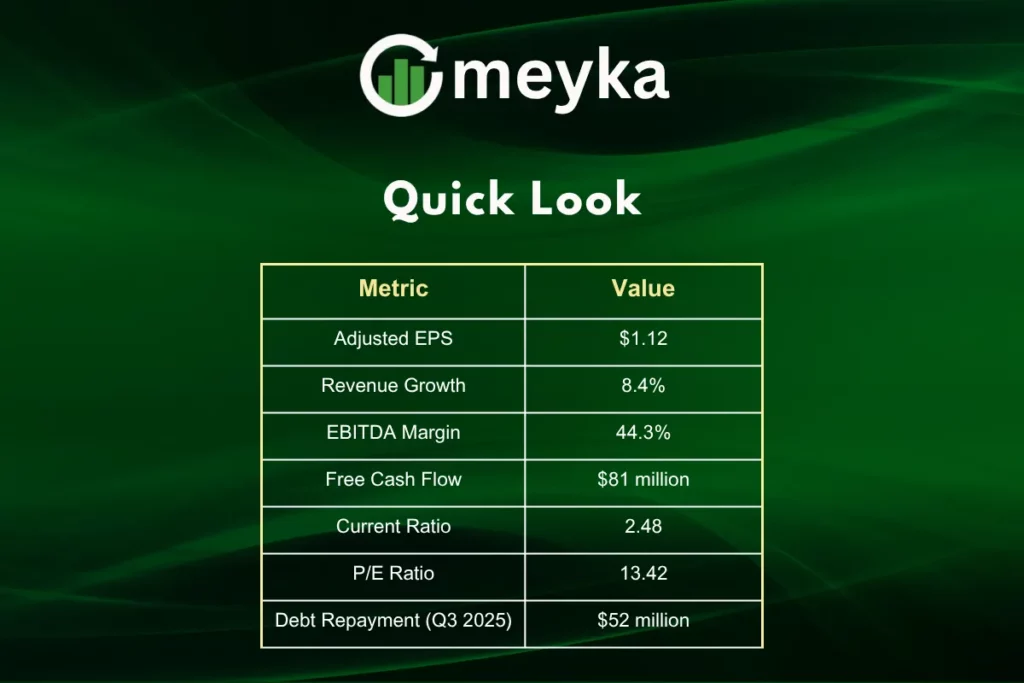

We witnessed Embecta Corp deliver a standout performance in Q3 2025, surpassing market expectations with robust financials. The company reported an adjusted EPS of $1.12, beating the consensus estimate of $0.77, fueled by an impressive 44.3% EBITDA margin and 8.4% revenue growth. This success positions Embecta Corp as a compelling opportunity for investors seeking long-term value and margin stability.

The strong results reflect disciplined financial management, including a $52 million term loan B repayment toward a $110 million 2025 debt reduction goal. With $81 million in free cash flow and a 2.48 current ratio, Embecta Corp showcases financial flexibility, making it a prime candidate for a strategic re-rating in the market.

Why Embecta Corp’s Q3 2025 Results Matter

Embecta Corp’s Q3 2025 performance highlights its ability to exceed expectations in a competitive sector. The adjusted EPS of $1.12 reflects operational efficiency, while 8.4% revenue growth signals strong demand for its diabetes care solutions. This growth aligns with the company’s focus on innovation and market expansion.

The 44.3% EBITDA margin underscores Embecta Corp ability to maintain profitability despite market challenges. We see this as a sign of sustainable operations, critical for long-term investors. The company’s focus on margin stability ensures it remains competitive.

Financial Discipline Drives Stability

Embecta Corp reduced its debt by $52 million in Q3 2025, part of a $110 million annual target. This repayment strengthens its balance sheet, reducing financial risk. The 2.48 current ratio indicates strong liquidity, supporting future growth initiatives.

The company generated $81 million in free cash flow, providing flexibility for reinvestment or further debt reduction. We view this as a testament to Embecta Corp’s disciplined capital allocation. Such financial health attracts investors seeking stability and growth potential.

Valuation and Market Opportunity for Embecta Corp

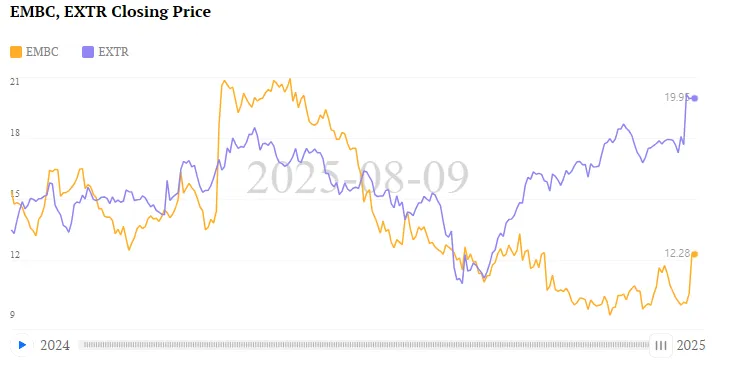

Embecta Corp’s 13.42 P/E ratio sits 20% below the sector average, suggesting undervaluation. Analysts project a 53% upside potential, with price targets ranging from $12 to $25. This gap presents a clear opportunity for a strategic re-rating.

The 16.99% pre-market stock surge post-earnings reflects market confidence in Embecta Corp’s trajectory. We believe the stock’s valuation, combined with strong fundamentals, positions it as a strategic buy for investors with a 3–5 year horizon. The company’s focus on value creation enhances its appeal.

Full-Year Guidance Signals Confidence

Embecta Corp projects full-year revenue between $1.078 billion and $1.085 billion, reflecting steady growth. The anticipated adjusted EPS of $2.90–$2.95 reinforces confidence in sustained profitability. These projections align with the company’s long-term strategy.

The company aims to maintain a 63.25%–63.5% adjusted gross margin, showcasing operational consistency. We see this guidance as a signal of Embecta Corp’s ability to navigate market dynamics. Investors can expect reliable performance in the coming quarters.

Strategic Positioning for Long-Term Growth

Embecta Corp’s focus on diabetes care solutions positions it in a high-demand market. Its innovative product pipeline supports sustained revenue growth. We view this as a key driver for future success.

The company’s disciplined capital allocation prioritizes both income and growth. By balancing debt reduction with reinvestment, Embecta Corp ensures long-term value creation. This strategy appeals to investors seeking stability and upside potential.

Key Financial Metrics at a Glance

Competitive Edge in the Diabetes Care Sector

Embecta Corp’s leadership in insulin delivery systems sets it apart from competitors. Its 8.4% revenue growth reflects strong market demand. We attribute this to the company’s focus on quality and innovation.

The 44.3% EBITDA margin highlights operational efficiency, a critical factor in maintaining a competitive edge. Embecta Corp’s ability to deliver consistent results strengthens its market position. This performance supports a strategic re-rating in the near term.

Final Thoughts

Embecta Corp’s Q3 2025 results highlight its potential for a strategic re-rating amid strong financial performance. The company’s 8.4% revenue growth, 44.3% EBITDA margin, and disciplined capital allocation signal a bright future. We see Embecta Corp as a compelling opportunity for investors seeking value and stability.

The projected 53% upside potential and undervalued P/E ratio make it a standout in the healthcare sector. With a focus on innovation and financial discipline, Embecta Corp is well-positioned for sustained growth. This article does not provide financial advice.

Disclaimer:

This is for informational purposes only and does not constitute financial advice. Always do your research.

What brings you to Meyka?

Pick what interests you most and we will get you started.

I'm here to read news

Find more articles like this one

I'm here to research stocks

Ask our AI about any stock

I'm here to track my Portfolio

Get daily updates and alerts (coming March 2026)