Do you know some companies show profits even when they are losing money? That’s possible with a metric called EBITDA.

EBITDA stands for Earnings Before Interest, Taxes, Depreciation, and Amortization. It’s not as scary as it sounds. In fact, it’s one of the most common ways investors and business owners look at profit.

Advertisement

We use EBITDA to see how much a business earns from its main work. It ignores taxes, loans, and even some business costs. This can make the company look stronger than it really is.

That’s why people love it and also why some don’t trust it.

Let’s look at what EBITDA really means, how to calculate it, and where it came from. We’ll also talk about why some big names in finance question it.

What is EBITDA?

EBITDA stands for Earnings Before Interest, Taxes, Depreciation, and Amortization. It’s a financial metric that shows how much money a company makes from its main business activities, without considering certain expenses.

Think of it this way: EBITDA focuses on the core operations of a business. It doesn’t include costs like loan interest, taxes, or the reduction in value of assets over time (depreciation and amortization).

Comparing EBITDA to Other Metrics:

- Net Income: This is the profit after all expenses, including interest, taxes, and depreciation. It’s the “bottom line” of a company’s income statement.

- Operating Income: Also known as EBIT (Earnings Before Interest and Taxes), this measures profit from regular business operations, excluding interest and taxes but including depreciation and amortization.

EBITDA helps compare companies in the same industry. It removes factors like taxes and financing that differ from company to company. Startups and companies in buyouts use it to focus on operations.

EBITDA Formula

a. Basic Formula:

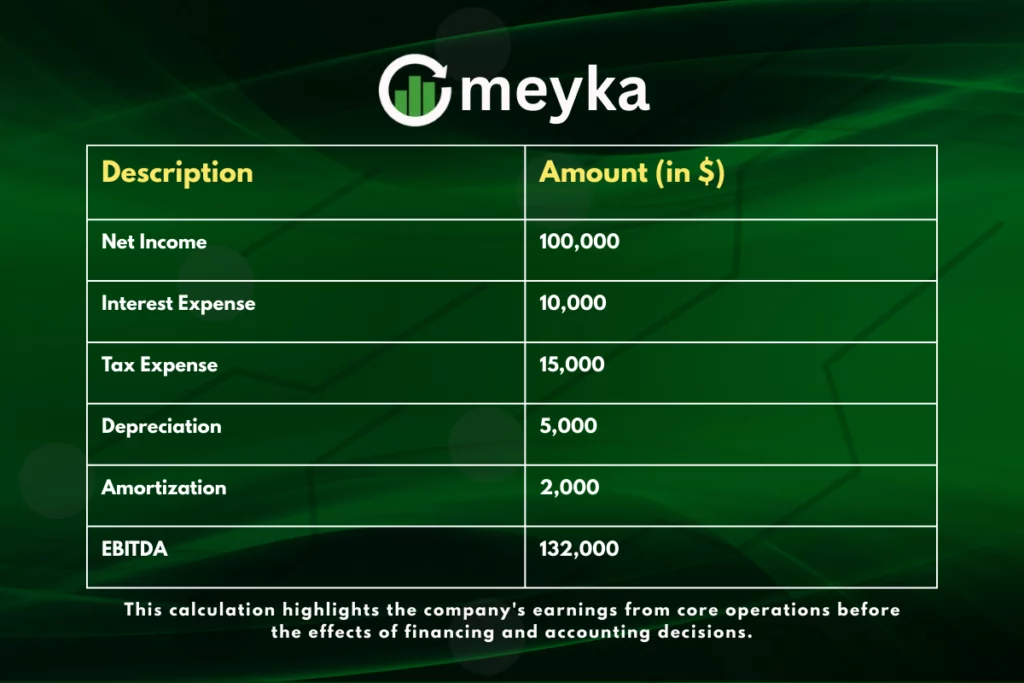

EBITDA = Net Income + Interest + Taxes + Depreciation + Amortization

Let’s break down each component:

- Net Income: The company’s total profit after all expenses.

- Interest: Costs paid on borrowed money.

- Taxes: Government levies on earnings.

- Depreciation: Reduction in value of tangible assets over time.

- Amortization: Similar to depreciation but for intangible assets like patents.

b. Alternate Formula (from Operating Income):

EBITDA = Operating Profit + Depreciation + Amortization

This version is handy when detailed financial statements aren’t available, but you have access to the operating profit.

c. Example Calculation:

History of EBITDA

EBITDA became popular in the 1980s during leveraged buyouts (LBOs). Investors needed a fast way to see if a company could generate cash to pay debt. EBITDA showed operational profit clearly, without financial or accounting distractions.

It later became a common metric for analyzing companies with high debt or in industries needing heavy investment. Its simplicity made it easy for analysts and investors to use.

Why Do Companies Use EBITDA?

EBITDA focuses on earnings from core business activities, excluding non-operational expenses. This shows how well a company performs in its main operations.

EBITDA makes it easier to compare companies, no matter their capital or tax structures by removing factors like taxes and interest. Though not a cash flow measure, EBITDA gives an idea of a company’s ability to generate cash for paying debt or reinvesting.

In deals, EBITDA helps value companies. The EV/EBITDA ratio helps decide if a company is over or undervalued compared to others.

Criticism and Limitations

EBITDA isn’t part of Generally Accepted Accounting Principles (GAAP). This gives companies flexibility in how they calculate it, which can lead to inconsistencies.

EBITDA excludes depreciation and amortization, and ignores asset wear and the need for reinvestment. It also leaves out interest and tax costs. Because it skips important expenses, EBITDA can make a company’s financial health look better than it really is.

Some companies use EBITDA to distract from losses or weak cash flow, which might mislead investors.

Warren Buffett famously said, “Does management think the tooth fairy pays for capital expenditures?” He warned against ignoring key costs like asset upkeep.

EBITDA vs. Other Metrics

a. EBIT

EBIT (Earnings Before Interest and Taxes) includes depreciation and amortization. This provides a more comprehensive view of operational profitability, especially for asset-heavy businesses.

b. Net Income

This is the bottom-line profit after all expenses. It’s a comprehensive measure but can be influenced by non-operational factors.

c. Operating Cash Flow

This metric shows the actual cash generated from operations, offering a clear picture of liquidity and financial health.

Real-World Examples

Startups often show strong EBITDA figures to highlight operational potential, even if they’re not yet profitable on the net income line.

These industries have significant depreciation costs due to assets like stores or aircraft. EBITDA can make them appear more profitable than they are.

Companies in this sector use EBITDA to smooth out earnings volatility caused by fluctuating commodity prices, but it may mask underlying financial issues.

Should Investors Trust EBITDA?

EBITDA is a useful tool, but it shouldn’t be the sole metric for investment decisions. It’s essential to consider it alongside other financial indicators like net income and cash flow. Consistency in calculation and transparency in reporting are also crucial.

Wrap Up

EBITDA offers a snapshot of a company’s operational performance, stripping away certain expenses to focus on core profitability. It’s valuable for comparisons and valuations, it’s not without flaws. Investors should use EBITDA as one of several tools in their financial analysis toolkit. It ensures a comprehensive understanding of a company’s financial health.

Advertisement

Frequently Asked Questions (FAQs)

EBITDA started in the 1980s during leveraged buyouts. Investors needed a quick way to see a company’s cash flow before interest, taxes, depreciation, and amortization. It made analyzing companies faster and easier.

EBITDA excludes key expenses like interest and taxes, potentially overstating profitability. Critics argue it can mislead investors about a company’s true financial health.

John Malone is credited with popularizing EBITDA. He emphasized cash flow over net income in cable TV, coining the term to highlight operational earnings.

Charlie Munger criticized EBITDA, calling it “bull**** earnings.” He believed it concealed financial realities by ignoring important costs like interest and taxes.

Disclaimer:

This content is for informational purposes only and not financial advice. Always conduct your research.

Advertisement

What brings you to Meyka?

Pick what interests you most and we will get you started.

I'm here to read news

Find more articles like this one

I'm here to research stocks

Ask Meyka Analyst about any stock

I'm here to track my Portfolio

Get daily updates and alerts (coming March 2026)